Interest-free loans, or loans at below-market interest rate, are widespread among entities under common control. They can also act as a form of government grant, intended to stimulate economic growth and development.

According to IFRS 9.B5.1.1, long-term loans or receivables that do not carry interest should be recognised at their fair value. This is measured as the present value of all future cash flows, discounted using the prevailing market interest rates for a comparable instrument (same currency, term, etc.), with a similar credit rating. Usually, the debtor’s incremental borrowing rate is a good starting point for calculating the discount rate. Any amount loaned or borrowed exceeding the fair value of the loan should be accounted for according to its substance under other applicable IFRS.

Let’s dive in.

Example: Loan at below-market interest rate subsidised by government

Entity A obtains a loan of $900,000 from a bank on 25 September 20X1. The bank’s quoted interest rate for this loan is 5%, but the government will subsidise the loan, and Entity A will only be charged 2% p.a. The loan will be repaid after two years, with interest paid annually. All calculations presented in this example are available for download in an Excel file.

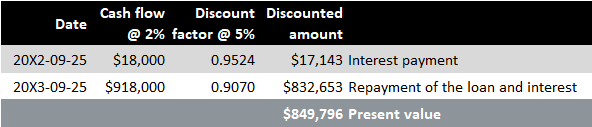

Entity A prepares a schedule of expected cash flows for the loan, where interest is calculated using the subsidised rate of 2% p.a. Meanwhile, the discount rate applied to determine the loan’s fair value is based on the market interest rate of 5% p.a.

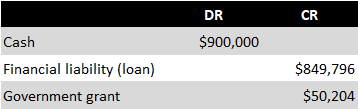

The difference between the fair value of the loan liability ($849,796) and the cash received from the bank ($900,000) is recognised as a government grant (IAS 20.10A).

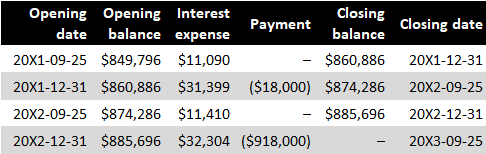

The loan is then measured at amortised cost as follows:

--

Too many IFRS updates? I know the feeling! That's why I created Reporting Period. It's a concise monthly summary of IFRS developments and Big 4 insights for accounting professionals. It's completely free, with zero spam, and you can unsubscribe anytime with one click. Interested? Leave your email below:

As mentioned previously, interest-free loans are frequent among entities under common control. The difference between the fair value of such a loan and the cash proceeds is usually recognised as:

- Increase in the parent’s investment in the subsidiary in the parent’s separate financial statements, and

- Equity contribution in the subsidiary’s separate financial statements.

However, these loans may trigger additional tax charges due to potential violations of transfer pricing laws in certain countries.

Interest-free intra-group loans often lack a specified repayment date, which can make it challenging to predict cash flows and determine fair value. Two potential accounting approaches are:

- Treating the loan as short-term and repayable on demand, therefore considering its fair value equal to the proceeds received, or

- Treating it as an in-substance equity contribution from the parent.

The exact treatment depends on the specific facts and circumstances surrounding the loan, although the first approach is generally more common. For a more comprehensive discussion on this topic, refer to BDO’s publication ‘Applying IFRS 9 to Related Company Loans‘.

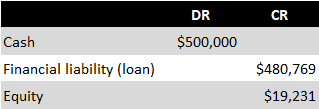

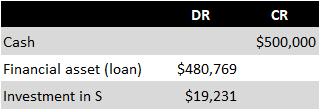

On 20 April 20X1, subsidiary ‘S’ receives an interest-free loan of $500,000 from parent ‘P’, repayable after one year. The bank’s quoted interest rate for such a loan is 4%. Initially, S discounts the loan repayment using the market rate (i.e. 4%), resulting in a fair value of the liability amounting to $480,769. Calculations from this example can be downloaded in an Excel file.

S recognises the loan as follows:

The entries made by P are as follows:

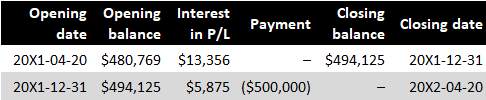

As seen here, the difference between the cash received and the loan’s fair value at initial recognition is recognised as an additional equity contribution by P. The loan is then accounted for using the amortised cost method:

See also how to account for other types of intra-group transactions in separate financial statements.