IAS 16 and IAS 38 present two options for measuring PP&E or intangible assets after their initial recognition: the cost model or the revaluation model (IAS 16.29; IAS 38.72).

Under the revaluation model, an asset’s carrying value is its fair value (i.e., the revalued amount), adjusted for any accumulated depreciation and impairment losses. Revaluations should be made frequently enough to ensure that the carrying amount doesn’t significantly differ from the fair value at the end of the reporting period (IAS 16.31,34; IAS 38.75). There’s no requirement for an independent valuation, but such information should be disclosed (IAS 16.77(b)). When an entity switches from the cost model to the revaluation model, it isn’t required to apply this change in accounting policy retrospectively (IAS 8.17).

The same measurement model should be applied consistently to an entire class of PP&E or intangible assets (IAS 16.29; IAS 38.72). If one asset is revalued, the whole class to which that asset belongs should also be revalued (IAS 16.36,38; IAS 38.73). A class comprises assets of a similar nature and use in the entity’s operations. For examples of classes of PP&E, see IAS 16.37.

The revaluation surplus resulting from an increase in the carrying amount of an asset is recognised in OCI, while any decrease or impairment losses affect P/L. However, increases are included in P/L up to the amount of previous decreases and impairment losses, and decreases are included in OCI up to the amount of previous increases. The revaluation surplus balance is accumulated separately in equity, labelled as ‘revaluation surplus’ (IAS 16.39-40).

The revaluation surplus can be transferred to retained earnings without impacting P/L, provided there is a higher depreciation charge due to revaluation, or the related asset is derecognised (IAS 16.41). These transfers aren’t obligatory, but are recommended, to prevent indefinite carrying forward of the revaluation surplus balance, even if the related assets are no longer in existence.

--Too many IFRS updates? I know the feeling! That's why I created Reporting Period. It's a concise monthly summary of IFRS developments and Big 4 insights for accounting professionals. It's completely free, with zero spam, and you can unsubscribe anytime with one click. Interested? Leave your email below:

Revaluation of intangible assets

The revaluation model for intangible assets prohibits the revaluation of intangible assets that have not been previously recognised as assets, or the initial recognition of intangible assets at amounts other than cost (IAS 38.76). However, IAS 38 does permit the revaluation model to be applied to intangible assets received via a government grant and recognised at a nominal amount. Assets of this nature (e.g., fishing licences, import quotas) are often the only ones satisfying the active market criterion outlined below.

IAS 38.75 stipulates that the fair value of an intangible asset should be measured by reference to an active market, i.e., Level 1 in the fair value hierarchy. IAS 38 does not allow the use of Level 2 or 3 inputs for measuring fair value. It’s rare for an active market to exist for an intangible asset, as stated in IAS 38, particularly for unique intangible assets like brands. Contracts for the sale of intangible assets are typically negotiated between individual buyers and sellers, with transactions occurring infrequently (IAS 38.78).

Entries at the revaluation date

The asset’s carrying amount should equal its fair value at the revaluation date (IAS 16.35). This can be achieved in two ways:

- by adjusting both the asset’s gross book value and its accumulated depreciation, or

- by eliminating the accumulated depreciation and adjusting the gross book value to equal the revalued amount.

Example: Entries at revaluation

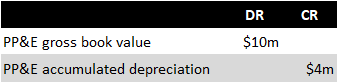

Entity A has an asset costing $10 million with a 10-year useful life and has been in use for 4 years. Thus, accumulated depreciation is $4 million (straight-line method, no residual value), resulting in a net book value of $6 million. The asset is carried at a revalued amount, and its fair value is estimated at $8 million.

The balances related to the asset before revaluation are as follows:

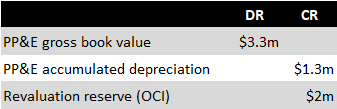

The following entries are made at the revaluation date:

Approach #1

Under this method, accumulated depreciation is eliminated and the gross book value equals the fair value. The resulting revaluation gain of $2m is recognised in OCI.

Approach #2

This method adjusts the gross book value upwards, proportional to the relative increase in the carrying amount due to revaluation, i.e., by 33%.

More about IAS 16 and 38

See other pages relating to IAS 16 and IAS 38:

IAS 16 Property, Plant and Equipment: Scope, Definitions and Disclosure

IAS 38 Intangible Assets: Scope, Definitions and Disclosure

IAS 16: Cost of Property, Plant and Equipment

IAS 38: Recognition and Cost of Intangible Assets

IAS 16 and IAS 38: Depreciation and Amortisation of Property, Plant and Equipment and Intangible Assets