IFRS 5 establishes specific requirements for the presentation and disclosure of discontinued operations to help financial statement users assess an entity’s ability to generate profit and cash. A discontinued operation is defined by IFRS 5.32 as a component of an entity that has either been sold or is classified as held for sale and:

- Represents a distinct major business line or operational region,

- Is part of a coordinated plan to sell a distinct major business line or operational region, or

- Is a subsidiary acquired solely for resale.

Let’s explore these in more detail.

Component of an entity

A component of an entity refers to operations and cash flows which can be clearly distinguished, both in terms of operations and financial reporting, from the rest of the entity (IFRS 5 Appendix A). IFRS 5.31 elaborates that such a component would have been identified as a CGU when in use or as a separate subsidiary (IFRS 5.36A).

Abandoned operations

Operations are classified as discontinued only when they are actually abandoned, not when the management merely decides to do so.

Presentation and disclosure

Post-tax profit or loss of discontinued operations is consolidated into a single amount in the P/L and OCI statements. This total also reflects any effects from remeasuring to fair value less costs to sell, or from the sale of assets or groups of assets linked to the discontinued operation (IFRS 5.33(a)). Detailed breakdowns of this figure are typically given in the notes, as mentioned in IFRS 5.33(b), (d), and the EPS provisions of IAS 33.68. Additionally, disclosures should also cover net cash flows related to the operating, investing and financing activities of the discontinued operations (IFRS 5.33(c)).

Any adjustments made during the current period to previously presented amounts in discontinued operations, which relate to a discontinued operation sold in an earlier period, should still be classified under discontinued operations. Examples of such adjustments can be found in IFRS 5.35.

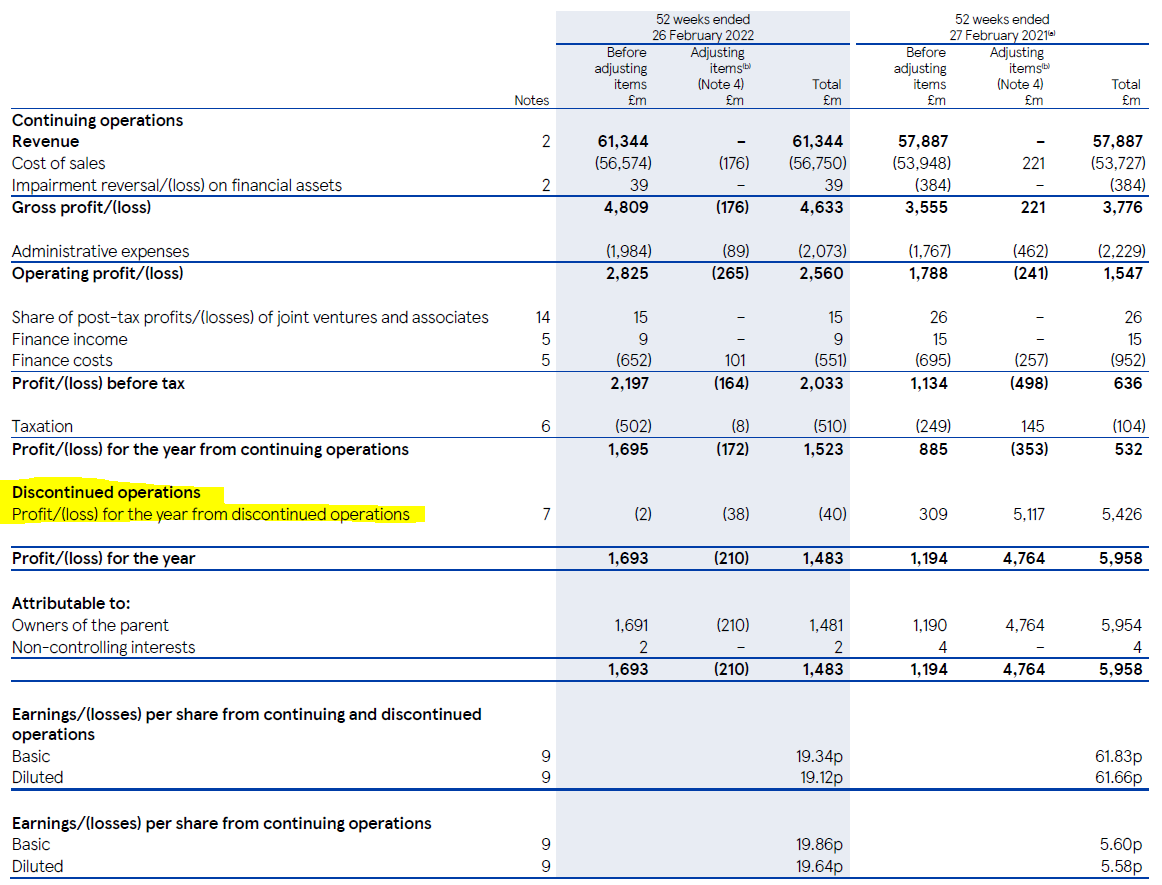

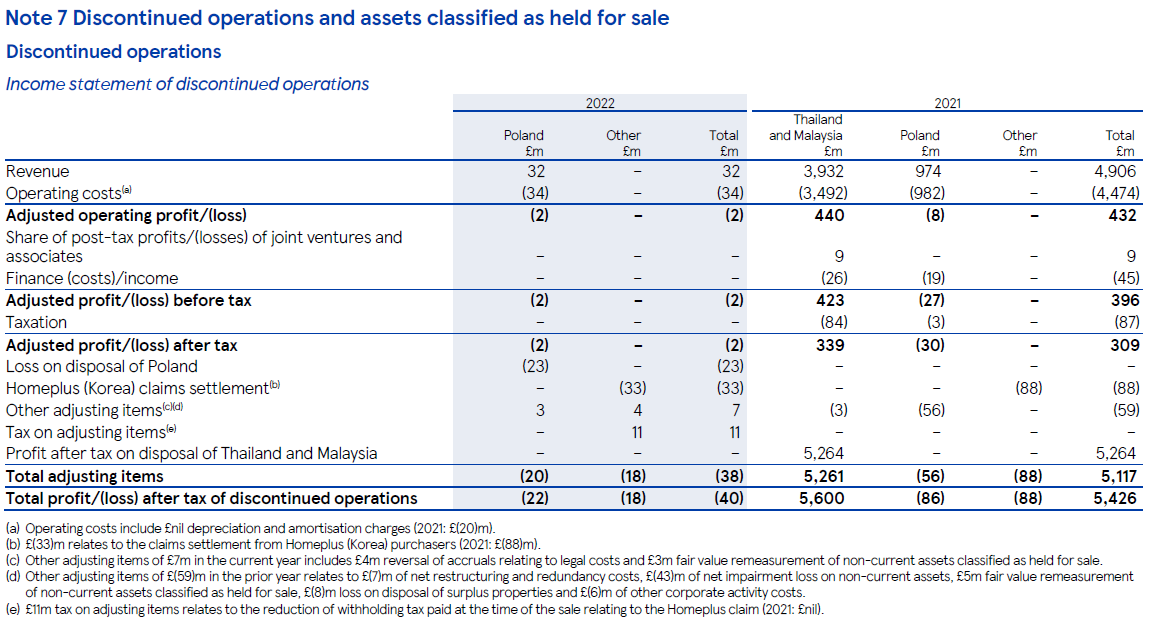

Below are examples that demonstrate how to present discontinued operations in the income statement, with associated disclosures in the notes.

Too many IFRS updates? I know the feeling! That's why I created Reporting Period. It's a concise monthly summary of IFRS developments and Big 4 insights for accounting professionals. It's completely free, with zero spam, and you can unsubscribe anytime with one click. Interested? Leave your email below:

Comparative information

Income statements from previous periods must be restated so that any operations classified as discontinued by the end of the current reporting period align with IFRS 5 presentation requirements (IFRS 5.34). However, no adjustments should be made to comparative data regarding assets and liabilities in the statement of financial position.

Intragroup transactions

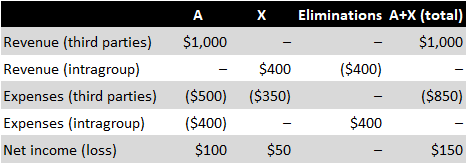

Let’s take a closer look at the treatment of intragroup transactions with discontinued operations using the following example:

Example: Intragroup transactions involving discontinued operations

Imagine Group A has a subsidiary named X that is an integral contributor to Group A’s operations. X earns revenue exclusively from intragroup activities but incurs expenses when dealing with external suppliers.

Over time, X is classified as a discontinued operation under IFRS 5. Below are tables presenting the revenue and expenses of both A and X. The ‘A+X’ column in the first table shows the consolidated results of Group A without treating X as a discontinued operation:

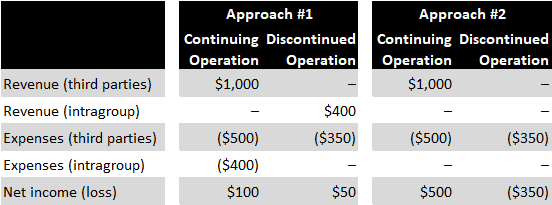

Let’s now examine two approaches to presenting the consolidated income statement when subsidiary X is classified as a discontinued operation:

Approach #1 incorporates all of X’s activities, including both external and intragroup transactions, marking them under one umbrella as a discontinued operation. As a result, the line showcasing discontinued operations now includes the intragroup revenue generated by X. Consequently, Group A’s continuing operations now comprise the intragroup expenses associated with X. This method’s merit lies in its accurate representation of both entities’ performance. However, a notable flaw is that intragroup expenses incurred by A will be presented as continuing operations in consolidated financial statements.

Approach #2 emphasises the complete cancellation of intragroup transactions. Hence, only X’s dealings with external entities are presented as a discontinued operation. This method’s drawback is its potential misrepresentation: it might suggest that X is a subsidiary operating at a loss, which isn’t accurate. Simultaneously, Group A’s profitability could be inaccurately inflated, given that X’s revenue contributions are overlooked.

The IFRS Interpretations Committee discussed the presentation of intragroup transactions between continuing and discontinued operations. They pointed out that neither IFRS 5 nor IAS 1 have stipulations concerning the presentation of discontinued operations that override the consolidation requirements of IFRS 10 which mandates the elimination of income and expenses resulting from intragroup transactions. However, the Committee did not specify how this elimination should be allocated between continuing and discontinued operations. As a result, entities can adopt both approaches illustrated above and clarify their method in the accompanying notes.

Changes in classification

Should an entity cease to classify a component as held for sale, the results of said component, which were previously presented as discontinued operations, should be reclassified and incorporated into continuing operations across all presented periods (IFRS 5.36). Moreover, effects of the remeasurement of assets and liabilities (like additional ‘catch-up’ depreciation) are incorporated into the present year’s results from continuing operations (IFRS 5.28).