IFRS 13 is applicable to all fair value measurements that are either required or permitted by other IFRSs. However, there are specific exceptions detailed in IFRS 13.6-7.

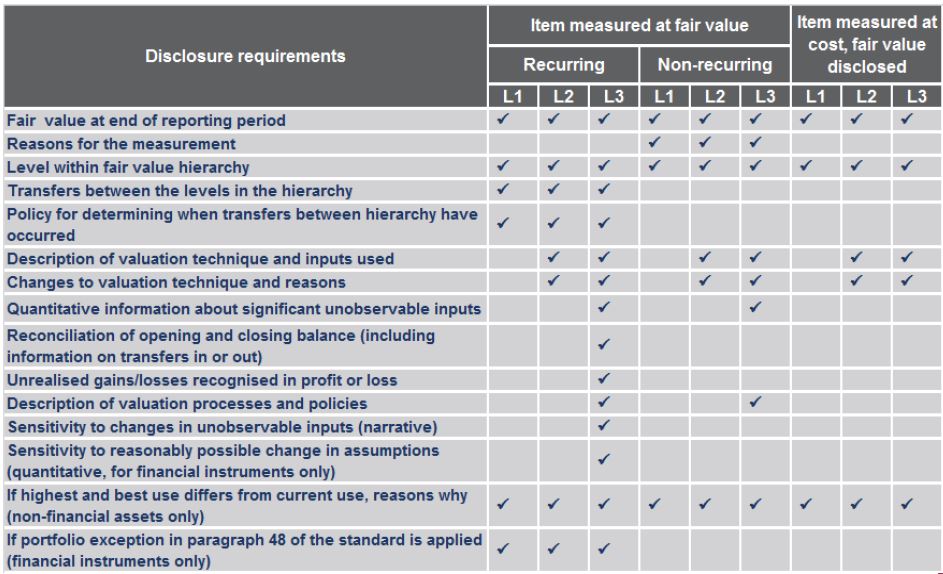

The disclosure requirements under IFRS 13, detailed in IFRS 13.91-99, are summarised below:

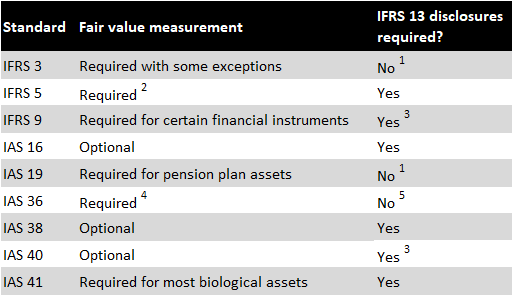

It should be noted that the disclosure requirements of IFRS 13 do not apply to the fair value measurement at the initial recognition of an asset or liability (IFRS 13.BC184). Other IFRS Standards, such as IFRS 7, mandate the disclosure of fair value for assets and liabilities that are not measured at fair value in the statement of financial position. Certain disclosure requirements of IFRS 13 are also relevant to these disclosures (IFRS 13.97), which is summarised in the table below:

- These IFRSs have specific disclosure requirements for assets and liabilities that they mandate to be measured at fair value.

- Disclosure is required when the fair value less costs to sell is lower than the carrying amount.

- IFRS 13 disclosures are mandatory even when the measurement basis is amortised cost (as per IFRS 9) or cost (as per IAS 40).

- Disclosure is necessary if the fair value less costs of disposal is lower than the carrying amount and higher than the value in use.

- IAS 36 outlines its own disclosure requirements for recoverable amounts measured as fair value less costs of disposal.

The disclosure requirements of IFRS 13 are exemplified in Examples 15-19 accompanying this Standard.

See the following pages relating to fair value measurement: