When a contract provides a customer with the option to obtain additional goods or services, such an option is viewed as a separate performance obligation if it confers a ‘material right’ to the customer. Simply put, it needs to be more than just a typical marketing or promotional offer. If this is the case, the customer has effectively made an advance payment for goods or services to be delivered in the future. A material right, as defined in IFRS 15.B39-B41, is a right that:

- The customer would not receive unless they enter into that specific contract; and

- Offers the customer an option to acquire an additional good or service at a price less than the stand-alone selling price (SSP).

To allocate a portion of the transaction price to this option – since it is considered a distinct performance obligation – it is key to estimate the SSP of the option. Such estimation should incorporate factors such as (IFRS 15.B42):

- Discount provided by this option,

- Discount the customer could get without the analysed option, and

- Probability of the option being exercised.

Revenue associated with the option is recognised either when future goods or services are transferred, or when the option expires, as per IFRS 15.B40. Examples 49, 50, 51, and 52 accompanying IFRS 15 and the examples below further illustrate this.

Example: An option for an additional product

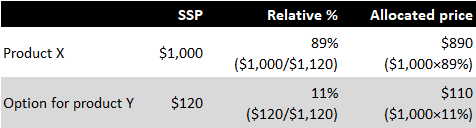

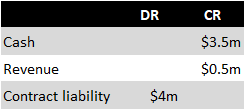

Let’s assume Entity A sells its customer product X for $1,000 and provides an option to purchase product Y for $500. Independently, Entity A sells product Y for $700. Entity A determines that the option to buy product Y for $500 constitutes a material right for the customer. Accordingly, Entity A must establish the SSP of this option and estimates it to be $120, calculated as follows:

[Discount provided by this option ($200) – discount offered to other returning customers ($50)] x 80% probability of the customer exercising this option = $120

The transaction price of $1,000 is therefore allocated between product X and the option for product Y as follows:

Upon delivering product X to the customer, Entity A recognises $890 of revenue (with the cost of product X being recognised as a revenue expense in P/L). The residual $110 is presented as a contract liability.

When the customer exercises the option and purchases product Y for $500, Entity A recognises a revenue of $610. This comprises the stated price of $500 and the utilisation of the contract liability of $110. Naturally, the cost of product Y is concurrently recognised as a revenue expense.

--

Too many IFRS updates? I know the feeling! That's why I created Reporting Period. It's a concise monthly summary of IFRS developments and Big 4 insights for accounting professionals. It's completely free, with zero spam, and you can unsubscribe anytime with one click. Interested? Leave your email below:

Example: Customer loyalty programme (points redeemable by the entity itself)

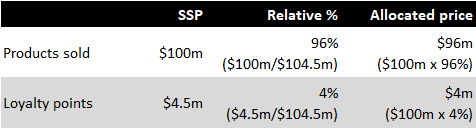

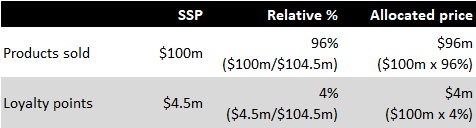

Entity A operates a customer loyalty programme. Customers receive 5 loyalty points for every $100 worth of purchases. Each point equates to $1 worth of purchases from Entity A. Entity A predicts that 90% of the points will be redeemed by customers, with the remaining 10% set to expire. Therefore, the stand-alone selling price of one point is $0.9 ($1 x 90% probability of redemption). Points can be redeemed until the end of the year following their issuance.

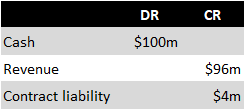

During the year 20X1, Entity A sells products totalling $100 million, leading to the awarding of 5 million points to customers. The overall transaction price of $100 million is allocated between the products sold and the points awarded as follows:

Entity A records the following entries:

In year 20X2, customers redeem 3.5 million points for product purchases. Entity A revises its assessment, now believing that 95% of points will be redeemed and only 5% will expire. Consequently, $3 million of contract liability is released as revenue (3.5 million points / 4.75 million points expected to be redeemed x $4 million of the allocated transaction price). The remaining $1 million is still recognised as contract liability and will be recognised in year 20X3 when the remaining points are redeemed or expire. The cost of products given to customers in exchange for loyalty points is naturally recognised as a revenue expense in P/L.

Example: Loyalty programme operated by a third party

Entity A participates in a customer loyalty programme operated by a large electronics retailer (Entity X). Customers earn 5 loyalty points for every $100 worth of purchases. These points can only be spent on purchases from Entity X, and each point equates to $1 worth of purchases. Entity A estimates the stand-alone selling price of one point to be $0.9. For each point transferred to a customer, Entity A pays Entity X $0.7.

During the year 20X1, Entity A sells products amounting to $100 million. Consequently, 5 million points are awarded to customers. The total transaction price of $100 million is allocated between the products sold and the points awarded as follows:

In addition, Entity A determines that it is acting as an agent for Entity X. As a result, Entity A recognises revenue immediately when points are awarded to customers, as its performance obligation as an agent is fulfilled upon providing customers with Entity X’s loyalty points. Entity A recognises revenue relating to loyalty points on a net basis (as a commission), which is the allocated price of $4 million minus $3.5 million paid to Entity X.

Entity A makes the following entries:

In Step 1, products are sold and points awarded:

In Step 2, revenue relating to loyalty points is recognised as a commission and payment to Entity X is made:

See other pages relating to IFRS 15:

Identifying a Contract

Performance Obligations and Timing of Revenue Recognition

Contract Modifications

Transaction Price

Principal vs Agent, or Reporting Revenue Gross vs Net

Revenue from Licensing of Intellectual Property

Revenue from Customers’ Unexercised Rights (Breakage)

Customer Loyalty Programmes and Other Options for Additional Goods or Services

Warranties

Contract Assets and Contract Liabilities

Contract Costs

Disclosure