Contract asset

A contract asset is recognised when a performance obligation has been satisfied, meaning the work is complete and revenue has been recognised, but the payment is still contingent on the entity’s future performance. This typically indicates that the entity can only issue an invoice to the customer after satisfying additional performance obligations under the same contract. Contract assets also arise when a performance obligation is satisfied over time, and revenue is recognised based on progress, but the right to invoice is triggered only at specific milestones or upon full satisfaction of the related performance obligation.

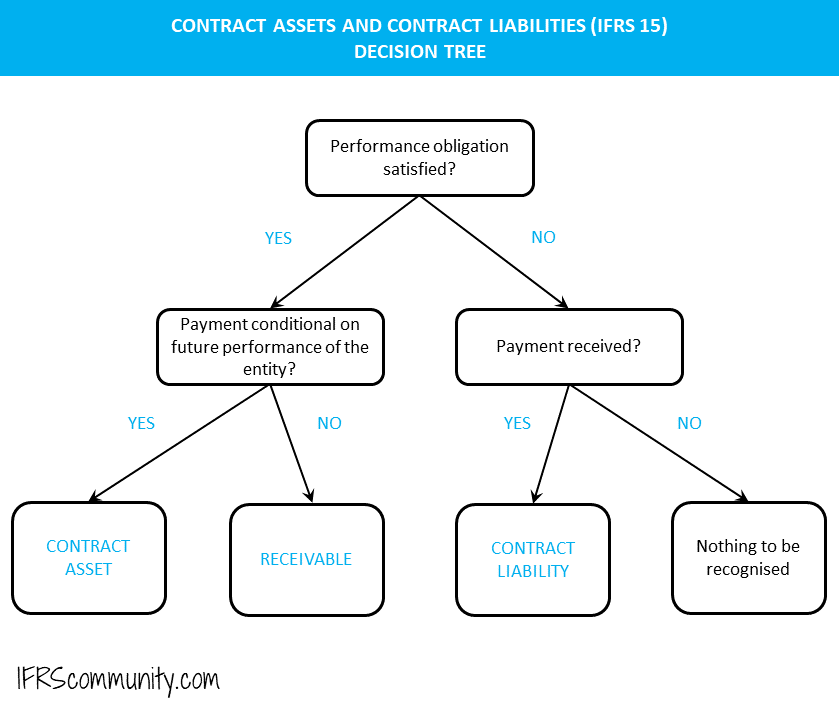

Contract assets differ from trade receivables due to the nature of the entity’s right to payment. In the case of trade receivables, the entity holds an unconditional right to receive payment, meaning only the passage of time is needed before payment is due (IFRS 15.105, 107-108). On the other hand, contract assets not only bear the credit risk but other risks as well, usually performance risk. The decision tree below illustrates this and an example follows.

Too many IFRS updates? I know the feeling! That's why I created Reporting Period. It's a concise monthly summary of IFRS developments and Big 4 insights for accounting professionals. It's completely free, with zero spam, and you can unsubscribe anytime with one click. Interested? Leave your email below:

Example: Contract asset and trade receivable in a telecommunications company

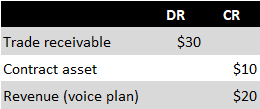

Let’s consider a telecommunications company that signs a contract with a customer. The customer purchases a smartphone for $100, payable within 30 days of contract signing, and a 24-month voice plan at $30 per month. Thus, the total transaction price in the contract is $820 ($100 + $30 x 24 months). The company regards the smartphone and voice plan as separate performance obligations. It allocates $340 to the smartphone and the remaining $480 to the voice plan. When the contract is signed and the smartphone is delivered, the company recognises these entries:

In this case, $340 of revenue is recognised when the smartphone is delivered to the customer. This amount reflects the transaction price allocated to this performance obligation, which may not match the price stated in the contract. However, only $100 is unconditionally due (to be paid within 30 days). The remaining $240 is contingent on the company’s future provision of the voice plan. If the company ceased to provide telecommunications services, the customer would not owe this amount. As such, $240 is recognised as a contract asset.

When the company issues an invoice for $30 for the first month of the voice plan, the following entries are recognised:

While the customer sees $30 on the invoice for the voice plan, from the company’s perspective, $10 is a partial repayment of the contract asset linked to the smartphone, with only $20 relating to the voice plan. This process is repeated monthly until the contract asset is fully converted to receivables and paid by the customer.

See also this real-life example from IFRS financial statements of Vodafone Group Plc:

Accrued and unbilled revenue

Is accrued or unbilled revenue considered a contract asset? Not necessarily. Just because an invoice has not yet been issued does not automatically classify the asset as a contract asset. If:

- Performance obligation has been satisfied and the related revenue recognised, and

- Payment isn’t conditional on satisfying other performance obligations in the contract, but

- Invoice hasn’t been issued by the reporting date (perhaps the precise amount isn’t yet known, or the accounts receivable accountant was late),

then the asset corresponding to the recognised revenue is classified as a receivable, not a contract asset (IFRS 15.105, BC323-326).

Impairment of contract assets

Contract assets are subject to the impairment requirements of IFRS 9. These requirements relate to the measurement, presentation, and disclosure concerning impairment (IFRS 15.107). In particular, entities are mandated to account for expected credit losses on their contract assets.

Please refer to the accompanying discussion regarding whether contract assets are considered financial assets.

Contract liability

A contract liability refers to an entity’s obligation to deliver goods or services and is recognised when a customer’s payment is due, or already received, prior to the fulfilment of a related performance obligation (IFRS 15.106). This type of liability is commonly recognised when a customer places an order and pays in advance. This is illustrated in the following example:

Example: Contract liability and trade receivable

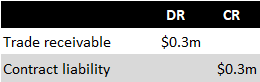

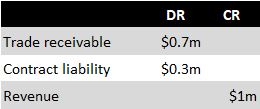

Suppose Entity A enters into a contract with a customer to manufacture and deliver 100 products for a total consideration of $1m. According to the contract, the customer is to be charged upfront for 30% of the contract’s total value, with this payment due within 30 days from the contract signing date. Entity A recognises the following entries:

An invoice for 30% of the contract’s total value is issued to the customer:

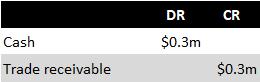

The customer settles the invoice:

The products are dispatched to the customer, an invoice for the remaining amount is issued, and revenue recognised:

Offsetting

As the rights and obligations in a contract with a customer are interdependent, contract assets and liabilities are presented on a net basis at a contract level (IFRS 15.BC317).

More about IFRS 15

See other pages relating to IFRS 15:

Identifying a Contract

Performance Obligations and Timing of Revenue Recognition

Contract Modifications

Transaction Price

Principal vs Agent, or Reporting Revenue Gross vs Net

Revenue from Licensing of Intellectual Property

Revenue from Customers’ Unexercised Rights (Breakage)

Customer Loyalty Programmes and Other Options for Additional Goods or Services

Warranties

Contract Assets and Contract Liabilities

Contract Costs

Disclosure