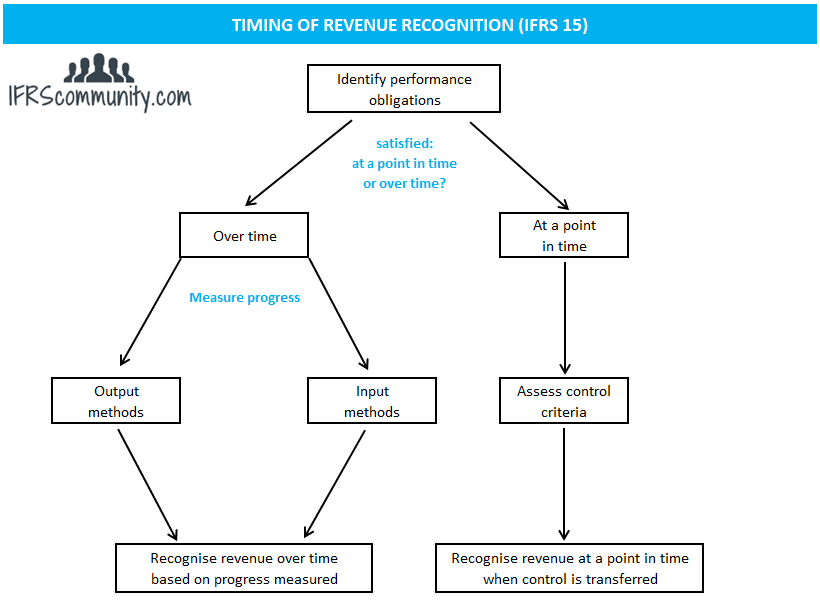

Revenue is recognised when performance obligations are satisfied in the amount of transaction price allocated to the satisfied obligations. Performance obligations are satisfied when a promised good or service is transferred to a customer. This transfer implies that the customer has obtained control of the asset or service in question. Performance obligations can be satisfied, and thereby revenue can be recognised, either at a point in time or over time:

Too many IFRS updates? I know the feeling! That's why I created Reporting Period. It's a concise monthly summary of IFRS developments and Big 4 insights for accounting professionals. It's completely free, with zero spam, and you can unsubscribe anytime with one click. Interested? Leave your email below:

Performance obligation

A performance obligation refers to a commitment to deliver a distinct good or service (or a bundle of goods or services) to a customer (IFRS 15.22). At the inception of a contract, entities must identify the goods or services promised within it. This acts as the initial step in identifying performance obligations. Apart from goods or services explicitly mentioned in the contract, all implied promises (for instance, stemming from past business practices or publicly stated policies) that give the customer a valid expectation of receiving a distinct good or service are also viewed as individual performance obligations. This holds true even if such promises aren’t legally enforceable (IFRS 15.24, BC87).

However, activities that do not involve a transfer of goods or services to a customer, even though they might be necessary for fulfilling a contract, are not considered performance obligations (IFRS 15.25). For example, this could include setting up a manufacturing process or connecting a customer to a telecommunications network.

Distinct goods or services

Definition of distinct goods or services

A good or service is considered distinct if it meets the following two conditions (IFRS 15.27):

- The customer can derive benefit from the good or service either independently or in conjunction with other resources that the customer can readily access. In other words, the good or service is capable of being distinct.

- The entity’s promise to deliver the good or service to the customer is separately identifiable from other commitments in the contract. In other words, the promise to deliver the good or service is distinct within the context of the contract.

A two-step approach is typically most effective. Firstly, entities consider whether the good or service is capable of being distinct. If it is not, then it isn’t considered distinct. If it is, the entity then assesses whether this good or service is distinct within the context of the contract. If it is, the good or service is distinct. If it isn’t, the good or service isn’t distinct. IFRS 15.26 provides examples of distinct goods or services.

If a promised good or service is not distinct, it should be combined with other promised goods or services until they collectively form a distinct bundle. Such a bundle is then viewed as a single performance obligation (IFRS 15.30).

The business model of an entity should not affect whether a good or service is treated as a separate performance obligation. For instance, a telecommunications company may prefer to categorise a ‘free’ mobile phone given to a customer as a marketing cost, because its main business is to provide telecommunication services rather than to sell phones. However, this kind of approach is not permissible under IFRS 15 (IFRS 15.BC88-BC90).

A good or service is capable of being distinct

In some cases, it’s clear that a customer can benefit from a good or service independently, like a piece of furniture. Other times, a good or service may only provide benefits when used in conjunction with other readily available resources, for instance, a mobile phone that requires a telecommunications service provider. According to IFRS 15.28, a readily available resource is a good or service sold separately (either by the reporting entity or a third party) or a resource that the customer has already acquired from the entity. This includes products or services that the entity will transfer to the customer under the contract before the good or service in question is transferred, or from other transactions or events. This is explained further in Example 11 Cases A/E, Example 12 and Example 56 Case A accompanying IFRS 15.

As noted in paragraph IFRS 15.BC100, the assessment of whether a customer can benefit from the goods or services independently should be based on the characteristics of the goods or services themselves, not the way the customer may use them. Thus, any contractual limitations that might prevent the customer from obtaining readily available resources from a source other than the entity are disregarded. This is illustrated in Example 11 Case D accompanying IFRS 15.

A good or service is distinct within the context of the contract

When a product or service promised to a customer is intrinsically linked to other promises in the contract, it’s not distinct. In such cases, the customer has, in substance, contracted for a combined product or service, and what appear to be distinct products or services are actually inputs into a combined item. For instance, when a customer orders 10,000 copies of a book to be printed, the paper used is not distinct, even though the customer could technically take the paper elsewhere to print the book. Similarly, construction companies don’t recognise revenue when they deliver building materials to a construction site if the customer has contracted them to construct a building. This is illustrated in the following examples accompanying IFRS 15: Example 10 Case A, Example 11 Cases B/E, Example 55 and Example 56 Case B.

Paragraph IFRS 15.29 details the three most common situations where two or more promises to transfer goods or services to a customer are not separately identifiable (a non-exhaustive list):

- The entity provides a significant service of integrating the goods or services with other goods or services promised in the contract into a bundle that represents the combined output for which the customer has contracted. In other words, the entity is using the goods or services as inputs to create or deliver the combined output specified by the customer. A combined output could include more than one phase, element or unit, such as construction contracts.

- One or more of the goods or services significantly modifies or customises, or is significantly modified or customised by, one or more of the other goods or services promised in the contract, such as the sale of software with significant customisation.

- Each of the goods or services is significantly affected by one or more of the other goods or services in the contract (they are highly interdependent or highly interrelated).

Non-refundable upfront fees

The accounting treatment of non-refundable upfront fees must be evaluated in line with the criteria for identifying a performance obligation. Typically, these initial fees do not lead to the transfer of a distinct good or service to the customer and, hence, are not considered as separate performance obligations. Rather, they are allocated to other identified performance obligations within the contract, in accordance with IFRS 15.B48-B50. If these upfront fees are identified as compensation for the setup costs borne by the entity, such costs can be recognised as costs incurred to fulfil a contract (assets) under IFRS 15.B51. Refer to Example 53 accompanying IFRS 15 for more detail.

Examples of distinct goods or services

- A car manufacturer selling cars to a dealer with a contractual promise to offer free maintenance to the end customer (the dealer’s customer) for three years post-purchase. This commitment to free maintenance constitutes a distinct service and a separate performance obligation for the car manufacturer.

- A telecommunications company offers a free smartphone to each customer who signs up for a premium telecommunications service and also charges a one-time connection fee. The free smartphone represents a distinct good and a separate performance obligation for the company, while the connection fee is not seen as a distinct service or a separate performance obligation as it does not result in any goods or services being transferred to the customer.

- A sporting equipment manufacturer contracts with a customer to produce 100,000 pieces of equipment. The manufacturer charges upfront setup costs of $0.5 million and $100 for each manufactured item. The setup of the production line is not a distinct service and does not constitute a separate performance obligation, as it does not result in the transfer of goods or services to the customer.

- Entity X manufactures specialised equipment which is installed on the customer’s premises. Only Entity X can perform the installation. The entity charges $5 million for the equipment and $0.5 million for its installation. The equipment and installation are considered a single performance obligation since the customer would not benefit from either the equipment or installation service independently.

A series of distinct goods or services that are substantially the same

An additional crucial type of performance obligation is a series of distinct goods or services that are substantially the same and share the same pattern of transfer to the customer (IFRS 15.22(b)). In practical terms, this often relates to repetitive services such as cleaning services or transaction processing (IFRS 15.BC114).

A series of distinct goods or services is treated as a single performance obligation when both of the following conditions are met, as per IFRS 15.23:

- Each distinct good or service in the series would satisfy the criteria for a performance obligation satisfied over time.

- The same method would be used to measure the entity’s progress towards the complete satisfaction of the performance obligation for each distinct good or service in the series.

Refer to Examples 7, 13, 25 accompanying IFRS 15 and the examples below.

Example: A series of distinct goods or services that are substantially the same

Entity A, a car parts manufacturer, contracts with a car producer to manufacture 1 million car seats over the forthcoming three years. Each car seat is a distinct good, yet Entity A considers the entire contract as a single performance obligation under paragraph IFRS 15.22(b). This is because it concludes that the conditions under paragraph IFRS 15.35(c) are met. It is irrelevant whether the production is distributed evenly over time or not.

Performance obligations satisfied over time

Criteria for performance obligations to be satisfied over time

A performance obligation is considered satisfied over time if any one of the criteria detailed in IFRS 15.35 is met:

- The customer simultaneously receives and consumes the benefits provided by the entity’s performance.

- The entity’s performance creates or enhances an asset that the customer controls as it is being created or enhanced.

- The entity’s performance doesn’t create an asset with an alternative use to the entity, and the entity has an enforceable right to payment for performance completed to date.

Simultaneous receipt and utilisation of benefits by the customer

This criterion applies typically in routine or recurring services, like flat-fee internet access or cleaning services, but it can also be relevant in more complex contracts. When it’s not clear whether this criterion is met, it’s crucial to assess whether another entity would need to significantly reperform the work completed by the original entity to fulfil the remaining performance obligation. In evaluating this, an entity should (IFRS 15.B4):

- Disregard potential contractual restrictions or practical limitations that might otherwise impede the transfer of the remaining performance obligation to another entity.

- Assume that another entity fulfilling the remaining performance obligation would not have access to any asset currently controlled by the original entity and would continue to be controlled by them if the performance obligation were transferred.

The IASB clarified that this criterion for a performance obligation satisfied over time is not intended for situations where an asset (e.g., work-in-progress) is created but not immediately consumed by the customer (IFRS 15.BC128). For more information, see Examples 13, 18, and 25 accompanying IFRS 15 and the example below.

Example: Satisfaction of performance obligation in a transportation service

Entity A agrees to transport a package from Madrid to London. At the end of the reporting period, the package has been transported to Paris. Entity A should recognise revenue for the portion of the transportation completed (i.e., from Madrid to Paris) since another entity would not need to significantly reperform the work completed by Entity A if it were to fulfil the remaining performance obligation, which is to transport the package from Paris to London (IFRS 15.B4).

Entity’s performance creates or enhances an asset controlled by the customer

This criterion, when satisfied, also indicates that a performance obligation is satisfied over time. It is most commonly applicable in the construction industry when an asset is created or enhanced on the customer’s land. See the following discussion for more information on control of an asset by a customer.

Asset without an alternative use to the entity and enforceable right to payment

Overview of the conditions to be met

A performance obligation is considered as satisfied over time under this criterion when both the following conditions are met:

- The entity’s performance does not create an asset with an alternative use due to legal or practical restrictions; and

- The entity possesses a contractual or legally enforceable right to receive reasonable compensation for the performance completed to date if the contract were to be terminated before completion, except for the entity’s failure to perform as promised.

No alternative use

An asset created by an entity’s performance does not have an alternative use if the entity is either:

- Contractually restricted from repurposing the asset during its creation or enhancement, or

- Practically limited from repurposing the completed asset for another use.

A contractual restriction is considered substantive when a customer can enforce rights if the entity attempts to repurpose the asset. Conversely, a restriction is not substantive if the asset is interchangeable and can be transferred to another customer without breaching the contract or incurring significant additional costs. Additionally, practical limitations exist if redirecting the asset for another use would cause significant economic losses to the entity, either due to substantial rework costs or the necessity to sell the asset at a considerable loss. This often applies to assets with unique design specifications for a specific customer or those located in remote areas (IFRS 15.B6-B8 and BC134-BC141).

The assessment of whether an asset has an alternative use is made at the inception of the contract (IFRS 15.36).

Enforceable right to payment

The obligation of the customer to pay for the work completed to date is a key indicator that the customer controls the asset and the performance obligation is satisfied over time. It doesn’t mean that the entity must have an unconditional right to payment at the reporting date. Instead, it should have a legally enforceable right to demand payment for performance completed to date if the customer were to terminate the contract prematurely. Further discussion on this criterion can be found in IFRS 15.37; B9-B13; BC142-BC147. Examples 16 and 17 accompanying IFRS 15 also provide further guidance.

Stand-ready obligation

In some cases, the essence of performance obligations lies in being ready to serve the customer, rather than delivering the actual goods or services. Such obligations are typically considered as satisfied over time, with revenue recognised linearly. For instance, a gym membership represents an obligation to be ready to provide the customer access to the gym and its facilities. It wouldn’t provide meaningful results if the gym tried to calculate the number of hours the customer will use throughout the contract and recognise revenue based on actual/total ratio. Instead, revenue is recognised proportionately to the elapsed time.

Measuring progress towards complete satisfaction of a performance obligation over time

Methods for measuring progress

When a performance obligation is satisfied over time, revenue is recognised in accordance with the progress made towards complete satisfaction of the performance obligation. The measurement of this progress can be either output-based or input-based. However, only one method should be applied to measure progress for a specific performance obligation, and also for performance obligations with similar characteristics (IFRS 15.BC161). This can be notably challenging for performance obligations composed of several non-distinct goods or services.

Output methods

As outlined in IFRS 15.B15-B17, output methods rely on the direct measurement of the value to the customer of the goods or services transferred to date, compared to the remaining goods or services promised under the contract. Methods of measurement can include surveys, milestones reached, elapsed time or units delivered. The chosen measurement method must consider all goods and services promised in the contract. The benefit of output methods is their direct measurement of the value of the goods or services delivered to the customer.

Right-to-invoice practical expedient

IFRS 15.B16 (see also BC167) provides a practical expedient, permitting the recognition of revenue at the sum to which an entity has a right to invoice, provided this corresponds directly with the value to the customer of the entity’s completed performance to date. This expedient can be highly beneficial, as it essentially allows entities to sidestep the need to determine the transaction price and allocate it to performance obligations.

Input methods

When the outputs used to measure progress are not directly observable or when acquiring the necessary information for their application incurs undue costs, entities are permitted to use input methods for measuring progress. As detailed in IFRS 15.B18-B19, these input methods can include measures based on direct labour hours, elapsed time, or the consumption of resources.

IFRS 15 also states that it’s possible to recognise revenue on a straight-line basis if the entity’s efforts or inputs are distributed evenly throughout the performance period. For additional insight, see Example 8 accompanying IFRS 15. The Basis for Conclusions to IFRS 15 and Example 19 include specific discussions on uninstalled materials (IFRS 15.BC170-BC175) and inefficiencies and wasted materials (IFRS 15.BC176-BC178).

Inability to measure the progress reliably

When an entity is unable to reliably measure progress, revenue is recognised only to the extent of costs incurred, as long as the entity expects to recover these costs. Such costs cannot be deferred and recognised as assets unless they meet the criteria for recognising costs incurred to fulfil a contract. Once reliable measurement of progress becomes feasible, the entity applies either output or input methods, as detailed above (IFRS 15.44-45).

Performance obligations satisfied at a point in time

The default option: performance obligations satisfied at a point in time

The default assumption is that a performance obligation is satisfied at a point in time. That is, if a performance obligation doesn’t meet the criteria to be considered as satisfied over time, it is considered to be satisfied at a particular point in time. The challenge lies in determining the exact moment an obligation is satisfied, which is when a customer obtains control of a promised good or service (‘an asset’), as detailed in IFRS 15.38.

Control of an asset

Control refers to the ability to direct the use of, and obtain substantially all of the remaining benefits from, an asset. The benefits of an asset are the potential cash flows that can be obtained directly or indirectly in many ways, such as by producing goods or providing services, enhancing the value of other assets or reducing expenses. Control also includes the capability to prevent other entities from accessing those benefits (IFRS 15.31-34).

The concept of control as can be divided into the following segments, further explained by the IASB in IFRS 15.BC120:

- Ability – the present right to:

- direct the use of an asset (this also entails restricting another entity from using the asset), and

- obtain substantially all of the remaining benefits from an asset.

The judgement of when control has been transferred to a customer should be made from the customer’s viewpoint (IFRS 15.BC121). Paragraph IFRS 15.38 offers additional indicators of control transfer, discussed further below.

Present right to payment for the asset

When the execution of a contract reaches a stage where the entity has a right to payment, it indicates that the control of the asset has been transferred to the customer.

Transfer of legal title to a customer

The transfer of a legal title to a customer under a contract signifies that control of the asset has been handed over. However, control can be transferred even without the legal title transfer, for instance, when the entity retains the legal title until all customer payments are settled.

Transfer of physical possession

The transfer of physical possession is another sign of control transfer, with a few notable exceptions:

- Repurchase agreements (including call and put options) detailed in IFRS 15.B64-B76 and Example 62 accompanying IFRS 15.

- Consignment arrangements (for example, with a dealer or distributor) explained in IFRS 15.B77-B78.

- Bill-and-hold arrangements outlined in IFRS 15.B79-B82 and Example 63 accompanying IFRS 15.

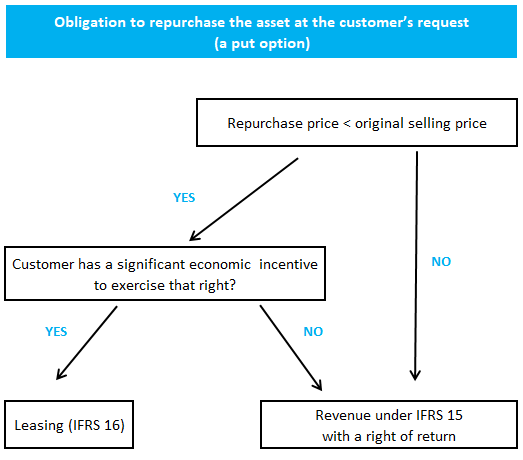

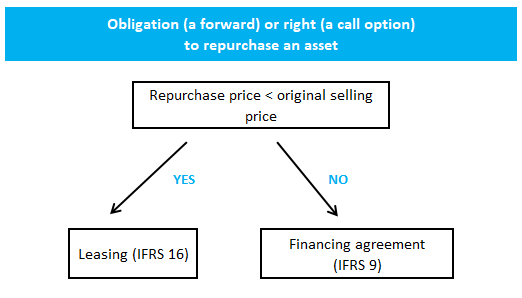

Repurchase agreements

A repurchase agreement is a contract where an entity sells an asset and simultaneously commits to, or reserves the right to, reacquire the asset. This repurchase can involve either the original asset, a substantially similar asset, or a different asset that incorporates the originally sold asset. Commonly, repurchase agreements take one of three forms:

- The entity’s commitment to buy back the asset (a forward);

- The entity’s option to reacquire the asset (a call option);

- The entity’s obligation to repurchase the asset upon the customer’s request (a put option).

The requirements related to repurchase agreements, as detailed in IFRS 15.B64-B76, are summarised below:

Consignment arrangements

When an entity supplies a product to a third party, like a dealer or distributor, for subsequent sale to end customers, it is crucial for the entity to determine if control of the product has been transferred to that third party at the time of delivery. If the third party has not gained control of the product, it may be considered as held under a consignment arrangement. As a result, the entity should not recognise revenue at the time of delivering the product.

Key indicators that an arrangement is a consignment agreement include: the entity retaining control of the product until a specified event, such as the product’s sale to an end customer, or until a certain period lapses; the entity’s right to demand the return of the product or to redirect it to another party, like a different dealer; and the dealer’s lack of an unconditional commitment to pay for the product (even if a deposit is required).

Bill-and-hold arrangements

A bill-and-hold arrangement is a contract where an entity invoices a customer for a product but retains physical possession of the product until a future date when it is transferred to the customer. For instance, a customer might request this arrangement due to lack of storage space or production schedule delays.

To determine when its performance obligation to transfer a product is satisfied, an entity must assess when the customer gains control of the product under IFRS 15.38. In some contracts, control is transferred upon the product’s delivery to the customer’s site or upon shipment, subject to the contract’s terms, including delivery and shipping conditions. However, in certain contracts, a customer may gain control of a product while it remains in the entity’s physical possession. In these cases, the customer has the ability to direct the use of, and obtain substantially all of the remaining benefits from, the product, despite opting not to take physical possession. Here, the entity no longer controls the product but provides custodial services over the customer’s asset.

Furthermore, to establish that a customer has obtained control of a product in a bill-and-hold arrangement, all the following criteria must be met:

- The rationale for the bill-and-hold arrangement should be substantive (e.g., customer-initiated).

- The product must be distinctly identified as the customer’s property.

- The product should be ready for immediate physical transfer to the customer.

- The entity must not have the option to use the product or allocate it to another customer.

When an entity recognises revenue from a product sale on a bill-and-hold basis, it should evaluate if there are remaining performance obligations, such as for custodial services.

Transfer of significant risks and rewards of ownership

The transfer of significant risks and rewards associated with owning an asset to the customer can signify the transfer of control. Nevertheless, in assessing the risks and rewards linked to the ownership of a promised asset, an entity must not consider risks that lead to an additional performance obligation beyond the obligation to transfer the asset. For instance, an entity might have transferred control of an asset to a customer without fulfilling an additional performance obligation to offer maintenance services for the transferred asset.

Acceptance of the asset by a customer

In contracts requiring customer acceptance of the product or service, the entity doesn’t consider the performance obligation satisfied until such acceptance is given. An exception applies when the entity can objectively verify that agreed-upon specifications, such as weight or size, are met (IFRS 15.B83-B85).

For agreements incorporating trial or evaluation periods, revenue isn’t recognised until the customer accepts the asset or the trial period concludes and the customer commits to paying for the asset (IFRS 15.B86).

Onerous (loss-making) contracts

IFRS 15 does not provide specific provisions for contracts resulting in losses, often referred to as onerous contracts, hence, the requirements of IAS 37 apply. In situations where multiple performance obligations are present within a contract, a provision is only recognised when the entire contract is onerous.

IAS 37 does not provide guidance on handling variable consideration, which can significantly influence whether a contract is considered onerous. Though IFRS 15 advocates caution when recognising variable consideration, this approach does not necessarily have to be adopted when determining if a contract is onerous. Variable consideration can be factored into the projected cash inflow, for instance, based on the expected value.

More about IFRS 15

See other pages relating to IFRS 15:

Identifying a Contract

Performance Obligations and Timing of Revenue Recognition

Contract Modifications

Transaction Price

Principal vs Agent, or Reporting Revenue Gross vs Net

Revenue from Licensing of Intellectual Property

Revenue from Customers’ Unexercised Rights (Breakage)

Customer Loyalty Programmes and Other Options for Additional Goods or Services

Warranties

Contract Assets and Contract Liabilities

Contract Costs

Disclosure