As businesses process large volumes of transactions, accounting errors may result from data-entry mistakes, mathematical inaccuracies, misunderstandings of applicable IFRS requirements, oversights or misinterpretations of facts. They may also arise from bugs in accounting software or miscommunication within finance teams. Most errors are unintentional and result from human error or process inefficiencies, although some may result from fraud.

Definition of errors

Under IAS 8.5, prior period errors are omissions from, or misstatements in, an entity’s financial statements for one or more prior periods. These errors result from a failure to use, or the misuse of, reliable information that:

- was available when the financial statements were authorised for issue; and

- could reasonably be expected to have been obtained and taken into account in preparing those statements.

Errors may relate not only to the recognition and measurement of assets or liabilities, but also to the presentation or disclosure of elements of the financial statements (IAS 8.41).

It’s worth noting that the IASB has clarified that an entity doesn’t have an error simply because its application of IFRS was inconsistent with an IFRIC agenda decision.

--Too many IFRS updates? I know the feeling! That's why I created Reporting Period. It's a concise monthly summary of IFRS developments and Big 4 insights for accounting professionals. It's completely free, with zero spam, and you can unsubscribe anytime with one click. Interested? Leave your email below:

Distinguishing between error corrections and changes in accounting estimates or policies

Corrections of errors are distinct from changes in accounting estimates or accounting policies. By definition, accounting estimates are monetary amounts in financial statements that are subject to measurement uncertainty. For example, releasing a provision through P/L because the actual outcome of a contingency differs from the provision previously recognised is not a correction of an error. Instead, it is a change in an accounting estimate (IAS 8.48).

However, what appears to be a change in an accounting policy or estimate may, in substance, be a correction of an error. Examples include:

- Revising an estimate, such as a fair value measurement, because of a previous oversight or misinterpretation.

- Changing an accounting policy because the previous policy didn’t comply with IFRS requirements.

- Reclassifying amounts in the primary financial statements because the previous classification wasn’t consistent with IFRS.

In each case, it’s important to determine whether the previous accounting treatment was affected by an omission or misinterpretation of facts or circumstances that could reasonably have been expected to be considered. If relevant information was available in the prior period but wasn’t used, the change is a correction of an error.

Similarly, when an entity changes an accounting policy or reclassifies amounts, it should consider whether the previous policy or presentation complied with IFRS. If it didn’t, the change is also a correction of an error.

Example: Gross vs net revenue presentation

Game World operates an online platform for gaming enthusiasts. The platform includes a marketplace through which games from various third-party sellers are sold to gamers. Game World processes payments between sellers and buyers and earns a fee from each sale. Historically, Game World recognised the full amount of the sales proceeds as revenue and the payments made to sellers as costs.

However, a newly appointed chief accounting officer believes that Game World should recognise only the commission it earns from each sale as revenue because the company acts as an agent between buyers and sellers. Consequently, the full amount spent by customers on games shouldn’t be recognised as Game World’s revenue. This change won’t affect operating profit.

Although management initiated the change voluntarily, it represents the correction of a prior period error because the previous accounting policy didn’t comply with IFRS 15.

Material errors

Material prior period errors must be corrected retrospectively in the first set of financial statements authorised for issue after the error is discovered (IAS 8.42). The correction involves:

- Restating the comparative amounts for the prior periods presented in which the error occurred; or

- If the error occurred before the earliest prior period presented, restating the opening balances of assets, liabilities and equity for that period.

- Presenting a third statement of financial position in certain circumstances.

This treatment ensures that the correction doesn’t affect P/L for the period in which the error is identified. Information presented for earlier periods, including historical summaries of financial data, should be restated as far back as practicable (IAS 8.46).

Entities aren’t required under IFRS to reissue their financial statements for prior years. However, local laws or regulations may require them to do so. For example, SEC registrants in the US must undertake a ‘Big R restatement’ if an error is material to the financial statements of a prior period. A Big R restatement requires the entity to restate and reissue its previously issued financial statements to correct the error.

The implementation guidance accompanying IAS 8 suggests labelling the relevant columns of comparative information as ‘restated’. Although IAS 8 doesn’t explicitly require this labelling, it is considered best practice and is frequently required by auditors.

Immaterial errors

IAS 8 doesn’t provide explicit instructions on the correction of immaterial errors. In practice, these errors are generally corrected in the current year without restating comparative amounts or opening balances.

It is commonly accepted that the correction should be recognised in the same financial statement line in which the error originally occurred. For example, if revenue was overstated in prior years, current-year revenue would be reduced so that cumulative revenue remains correct. If recognising the correction in the current year could influence the decisions of users of the financial statements, this may indicate that the error is material and should instead be corrected retrospectively.

Some accountants take the view that immaterial errors may be corrected directly through equity as a current-year movement. However, this conflicts with the requirement that all changes in equity during a period, other than those arising from transactions with owners in their capacity as owners, must be included in total comprehensive income (IFRS 18.112 / IAS 1.109).

Disclosure

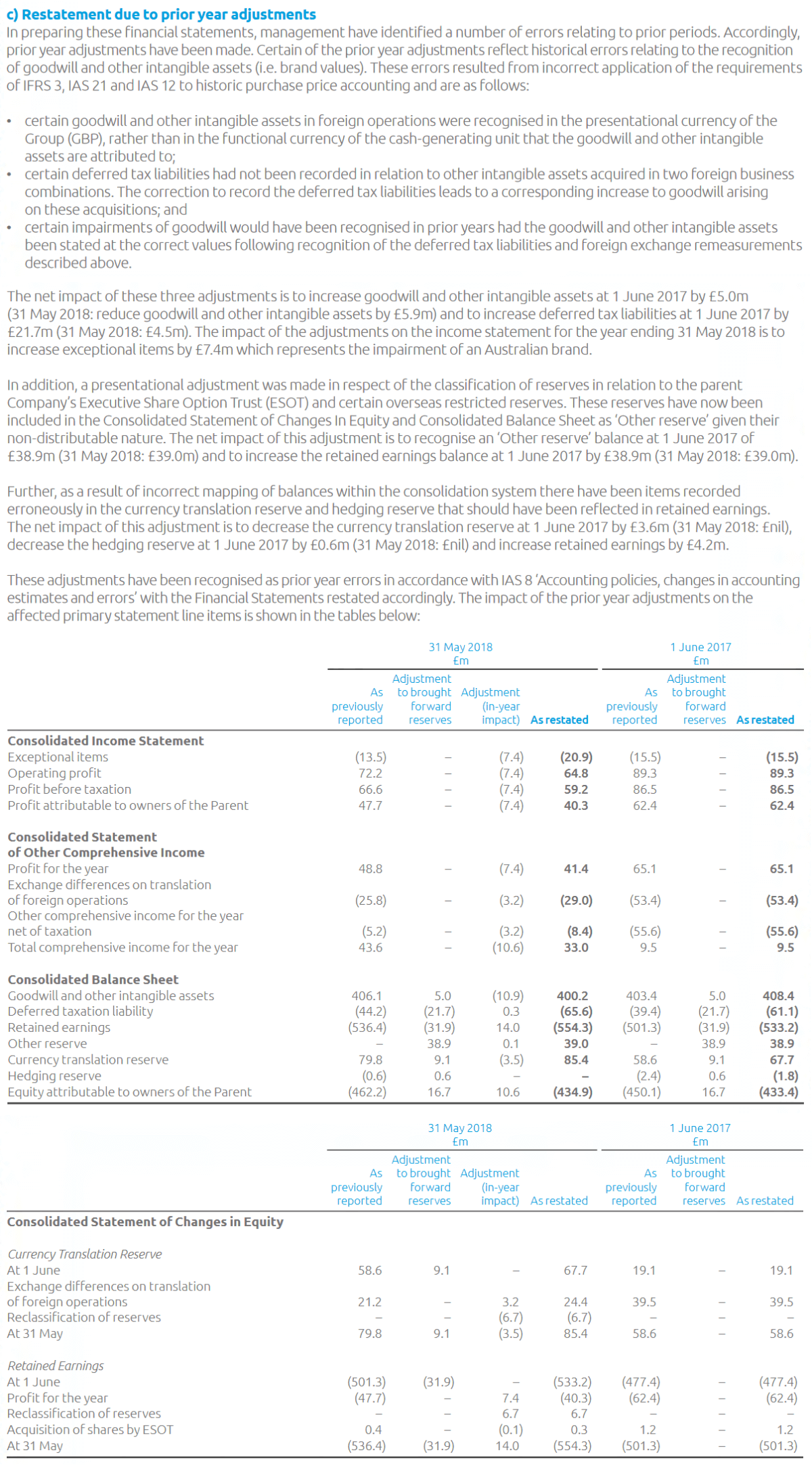

Entities that correct a material prior period error should provide the disclosures required by IAS 8.49. The extract below illustrates the application of these requirements: