Accounting policies encompass specific principles, bases, conventions, rules and practices applied by an entity when preparing and presenting its financial statements. If an IFRS specifically addresses a particular transaction or event, the entity’s accounting policy should be in accordance with that standard (IAS 8.7). Nevertheless, not all transactions or events are covered by IFRS. In such instances, entities must develop their own accounting policies using the hierarchy prescribed by IAS 8.

Accounting policies should be applied consistently to similar items throughout all reporting periods. That being said, entities may, and do, change their accounting policies in specific circumstances.

Let’s dive in.

--Too many IFRS updates? I know the feeling! That's why I created Reporting Period. It's a concise monthly summary of IFRS developments and Big 4 insights for accounting professionals. It's completely free, with zero spam, and you can unsubscribe anytime with one click. Interested? Leave your email below:

Absence of applicable IFRS

If a specific transaction or event isn’t governed by an existing IFRS, entities must develop an accounting policy that addresses the economic decision-making needs of financial statement users. The financial statements produced should (IAS 8.10):

- Faithfully represent the entity’s financial position, performance, and cash flows (CF.2.12-19).

- Reflect the economic substance of transactions, events, and conditions, rather than just their legal form.

- Remain neutral and prudent (CF.2.15-16).

- Be complete in all material respects.

When developing an accounting policy, entities should first determine whether any IFRS addresses similar issues and apply this IFRS to the fullest extent possible (IAS 8.11). If there’s no IFRS addressing similar matters, the next step is to consider the definitions, recognition criteria and measurement concepts from the Conceptual Framework for Financial Reporting, or simply the Conceptual Framework (CF). It is important to acknowledge, though, that the Conceptual Framework itself is not an IFRS Standard, and nothing within it has the authority to supersede any requirement of an IFRS Standard (CF.SP1.2).

Complex transactions may consist of several accounting issues. For some of those issues, entities may be able to identify similarities to matters addressed in other IFRSs. However, others might not have a clear analogy. The IASB’s Guide to Selecting and Applying Accounting Policies suggests that entities might refer to the requirements in an IFRS Standard for certain issues while turning to the Conceptual Framework for others. This approach is exemplified in the IFRS Interpretations Committee’s agenda decision regarding deposits relating to taxes other than income tax.

Entities can also refer to pronouncements from other standard-setting bodies with similar conceptual frameworks, such as US GAAP, or even other accounting literature and widely accepted industry practices. However, these sources must not contradict IFRSs dealing with similar issues or the Conceptual Framework (IAS 8.12). It’s worth noting that certain local jurisdictions may mandate the application of local GAAP for transactions not covered by IFRS.

Even if there’s no specific IFRS for a transaction or event, which likely means no explicit disclosure obligations, the general disclosure requirements under IFRS 18 still apply. These include:

- Introducing additional line items in the primary financial statements.

- Disclosing significant income or expense items separately.

- Providing additional information relevant to understanding the financial statements.

- Disclosing material accounting policy information.

- Disclosing assumptions and other major sources of estimation uncertainty.

Consistency in application

Entities must apply accounting policies consistently for similar transactions or events (IAS 8.13). This principle also applies to policies developed in the absence of applicable IFRS. Additionally, consolidated financial statements of a group should be prepared using consistent accounting policies for all group entities (IFRS 10.19, B86-B87).

However, some IFRSs permit the categorisation of items to which different accounting policies are applied. For instance, IAS 27.10 allows different measurement methods for various investment categories. Similarly, IAS 2.25 allows different cost formulas for inventories.

Changes in accounting policies

Changes in accounting policies can arise due to:

- The adoption of a new, revised, or amended IFRS; or

- A voluntary change by the entity.

Adoption of a new, revised, or amended IFRS

Whenever an entity adopts a new, revised or amended IFRS, it must follow the transitional provisions within that standard. Such transitional provisions override the general requirements of IAS 8 (IAS 8.19(a)). For instance, the transitional provisions might offer an exemption from fully retrospective application of new accounting policies, or might require specific disclosures explaining the impact of adopting the new standard.

If no specific transitional provisions exist, the new, revised or amended IFRS should be applied retrospectively (IAS 8.19(b)).

Voluntary change

Voluntary changes in accounting policy are permitted only if they ensure that the financial statements provide more relevant and reliable information (IAS 8.14). Such changes can be attributed to:

- Agenda decisions issued by the IFRS Interpretations Committee.

- Pronouncements from other standard-setting authorities used in developing an accounting policy in the absence of applicable IFRS (IAS 8.21).

- An entity’s internal assessments.

It’s important to note that:

- Choosing to apply an IFRS earlier than required is not considered a voluntary change in policy (IAS 8.20).

- Using a new accounting policy for events or transactions that either didn’t occur before or were immaterial isn’t a change in accounting policy (IAS 8.16(b)).

- The initial application of a policy to revalue assets in line with IAS 16 or IAS 38 should be accounted for as a revaluation and not under IAS 8 (IAS 8.17-18).

Retrospective application

Any voluntary policy change must be applied retrospectively (IAS 8.19(b)). This means adjusting the opening balance of each affected component of equity for the earliest period presented, and the other comparative amounts, as though the new policy had always been in place (IAS 8.22).

IAS 8.23-27 acknowledges that, at times, it might be impracticable to determine either the period-specific effects of the change or its cumulative effect. In such scenarios, the entity should apply the new accounting policy to the carrying amounts of assets and liabilities as at the beginning of the earliest period for which retrospective application is practicable. This period could even be the current one. Related adjustments should be applied to the opening balance of retained earnings or other relevant components of equity for that period.

When it’s impracticable to determine the cumulative effect across all previous periods, the entity should prospectively apply the policy from the earliest feasible period, disregarding the cumulative adjustment to assets, liabilities and equity that arose before this date.

Immaterial impact of change in accounting policy

The effect of a change in accounting policy might be immaterial. IAS 8.8 provides entities with relief from applying IFRS requirements when the outcome of following them is immaterial. So, it can be argued that if the application of a new policy doesn’t have a material effect, there’s no need to apply it retrospectively. However, when this new policy affects the recognition or measurement of assets or liabilities, entities must decide how to treat assets or liabilities previously measured under the old policy at the start of the current year. There are two potential approaches:

Approach 1: Assets and liabilities in the opening balance are adjusted to match the new accounting policy.

With this approach, any resultant impact is recognised in the current period’s P/L. This approach builds on the notion that a change in the accounting policy remains immaterial as long as the cumulative effect on the current period’s P/L is also immaterial. Notably, US GAAP SAB Topic 5.F Accounting Changes Not Retroactively Applied Due to Immateriality (ASC 250-10-S99-3) officially supports this approach.

Approach 2: The opening balance of assets and liabilities isn’t adjusted in accordance with the new policy.

This means no one-time P/L impact is recognised. The downside here is that the new policy won’t be entirely implemented until assets and liabilities recognised before the change have been derecognised. Here, the materiality of the change is determined by considering the potential consequences of adjusting all assets and liabilities under the new policy. Essentially, it asks: what’s the significance of what’s left out? This approach is similar to the impracticable restatement approach where, as per IAS 8.27, the cumulative adjustment to assets, liabilities and equity up to a specific date is ignored.

Disclosure

Accounting policy information

IAS 8.27A-27I (or IAS 1.117 before the adoption of IFRS 18) requires entities to disclose their material accounting policy information. IAS 8.27C lists situations in which an accounting policy is likely to be considered material, such as:

- A current-period change in accounting policy with a material impact.

- Available options permitted by IFRSs, such as the option to measure investment property at historical cost or fair value under IAS 40.

- The absence of an applicable IFRS, for instance, regarding business combinations under common control.

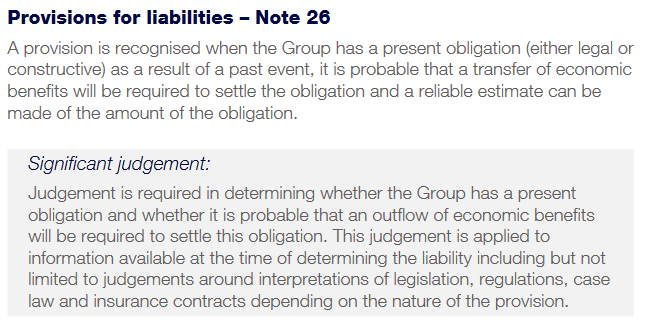

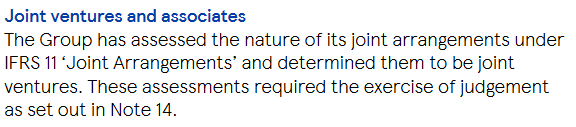

- Significant judgements or assumptions made in applying an accounting policy, such as determining control over a structured entity under IFRS 10.

- Complex accounting scenarios in which multiple IFRSs apply to a single transaction.

IAS 8.27D emphasises the greater usefulness of entity-specific accounting policy information over generic information, or details that merely copy or summarise IFRS requirements. For further insights on making materiality judgements concerning disclosures of accounting policy information, refer to paragraphs 88A-88G of IFRS Practice Statement 2: Making Materiality Judgements.

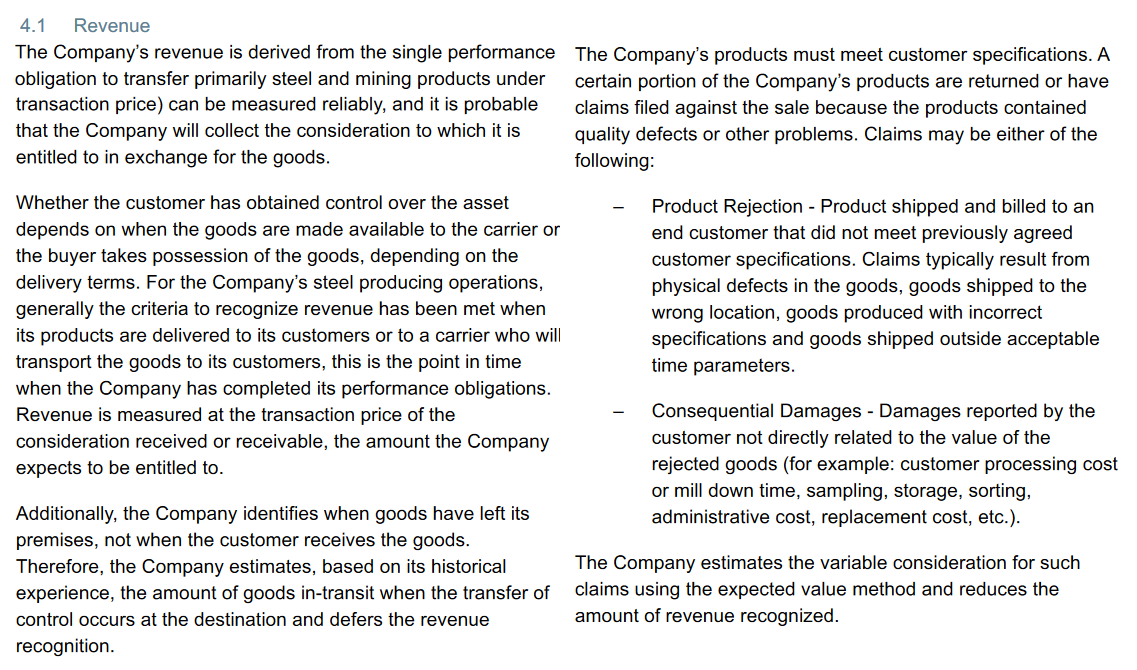

Below is an excerpt from ArcelorMittal’s annual report with entity-specific accounting policies related to revenue:

Judgements

Applying accounting policies involves exercising various judgements beyond estimations, and IAS 8.27G (or IAS 1.122 before the adoption of IFRS 18) mandates disclosure of significant judgements. These judgements refer to the conclusions made by management in the context of applying accounting policies to specific transactions or events. For instance, judgements are exercised by management when identifying performance obligations within a contract under IFRS 15 or determining whether certain arrangements qualify as a lease under IFRS 16. Even though some IFRSs explicitly require the disclosure of judgements in their domains, significant judgements must always be disclosed under IAS 8.27G, irrespective of whether other IFRSs include specific provisions.

The subsequent extracts from CRH’s and Tesco’s annual reports serve as examples:

It’s also valuable to state that no significant judgements have been involved, if that’s the case, of course:

Initial application of an IFRS

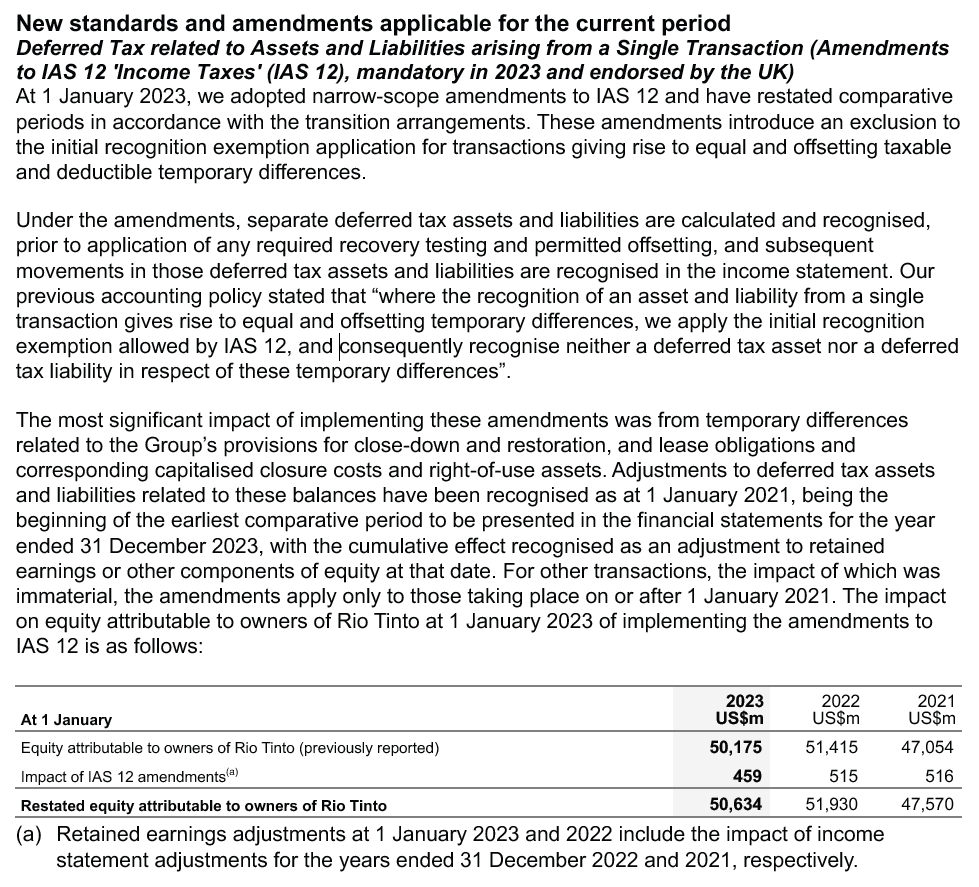

When an entity adopts a new IFRS that affects the current period, a prior period, or might affect future periods, the disclosures set out in IAS 8.28 must be provided in the year of application. This PDF file contains the disclosure made by Orange on adopting IFRS 15, and the extract below explains amendments to IAS 12:

Expected application of an IFRS

If an entity hasn’t applied an issued IFRS that isn’t yet effective, it should disclose that fact. Additionally, any available or reasonably estimable information about the possible impact of this IFRS on its financial statements should be provided (IAS 8.30-31).

Voluntary change in accounting policy

If an entity voluntarily changes its accounting policy, the nature of the change should be disclosed, together with reasons explaining why the newly adopted policy provides reliable and more relevant information. The impact of this change should also be quantified (IAS 8.29).

This example illustrates a voluntary change in accounting policy stemming from an agenda decision:

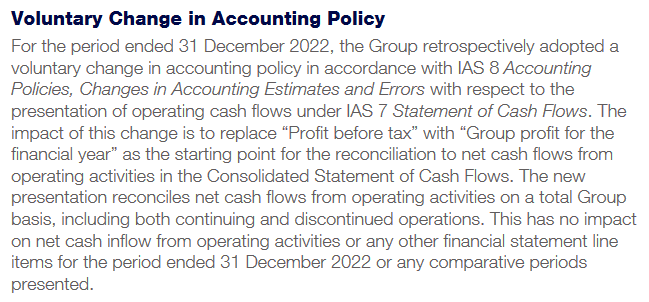

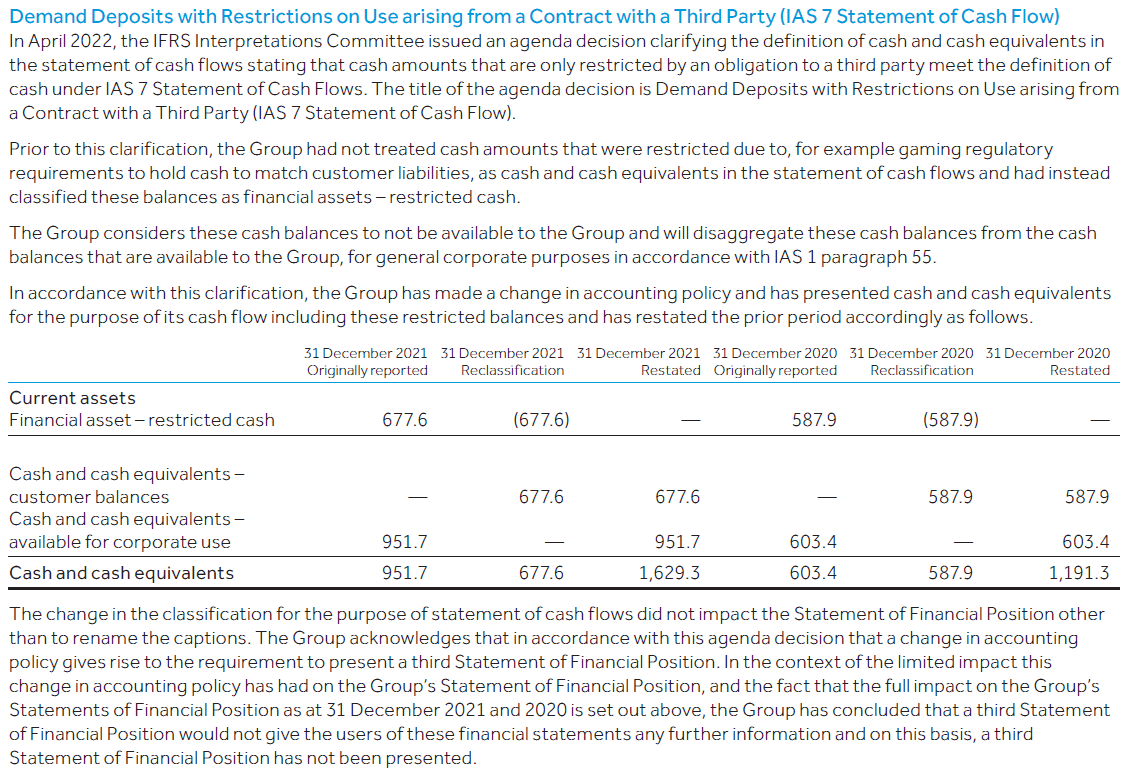

A voluntary change in accounting policy might also relate to the presentation of financial statements, without any impact on the recognition or measurement of assets, as illustrated in the extract that follows: