Materiality is a fundamental concept in financial reporting under IFRS. Information is considered material if its omission, misstatement or obscuring could reasonably be expected to influence decisions made by primary users of financial statements (IFRS 18.B1 / IAS 1.7). Materiality is relevant to decisions relating to the selection and application of accounting policies, as well as presentation and disclosure in financial statements.

IAS 8.8 provides entities with relief from applying IFRS requirements when the effect of applying them is immaterial. Furthermore, IFRS 18.19 (IAS 1.31) states that entities don’t have to provide a specific disclosure required by IFRS if the information resulting from that disclosure is immaterial. This holds true even if the IFRS sets out specific requirements or labels them as minimum requirements.

The notion of materiality is specific to individual entities, and IFRSs don’t provide any quantitative benchmarks (Conceptual Framework 2.11). However, the IASB has released the non-binding IFRS Practice Statement 2 Making Materiality Judgements, which provides additional guidance.

--Too many IFRS updates? I know the feeling! That's why I created Reporting Period. It's a concise monthly summary of IFRS developments and Big 4 insights for accounting professionals. It's completely free, with zero spam, and you can unsubscribe anytime with one click. Interested? Leave your email below:

Quantitative considerations

To determine materiality, entities and auditors often adopt the approach of applying a percentage to a selected benchmark. Typical bases for such calculations include 5% of profit before tax or 2-3% of operating income or EBITDA. However, these benchmarks will differ between sectors. For example, materiality levels used by financial institutions can be based on total assets or equity.

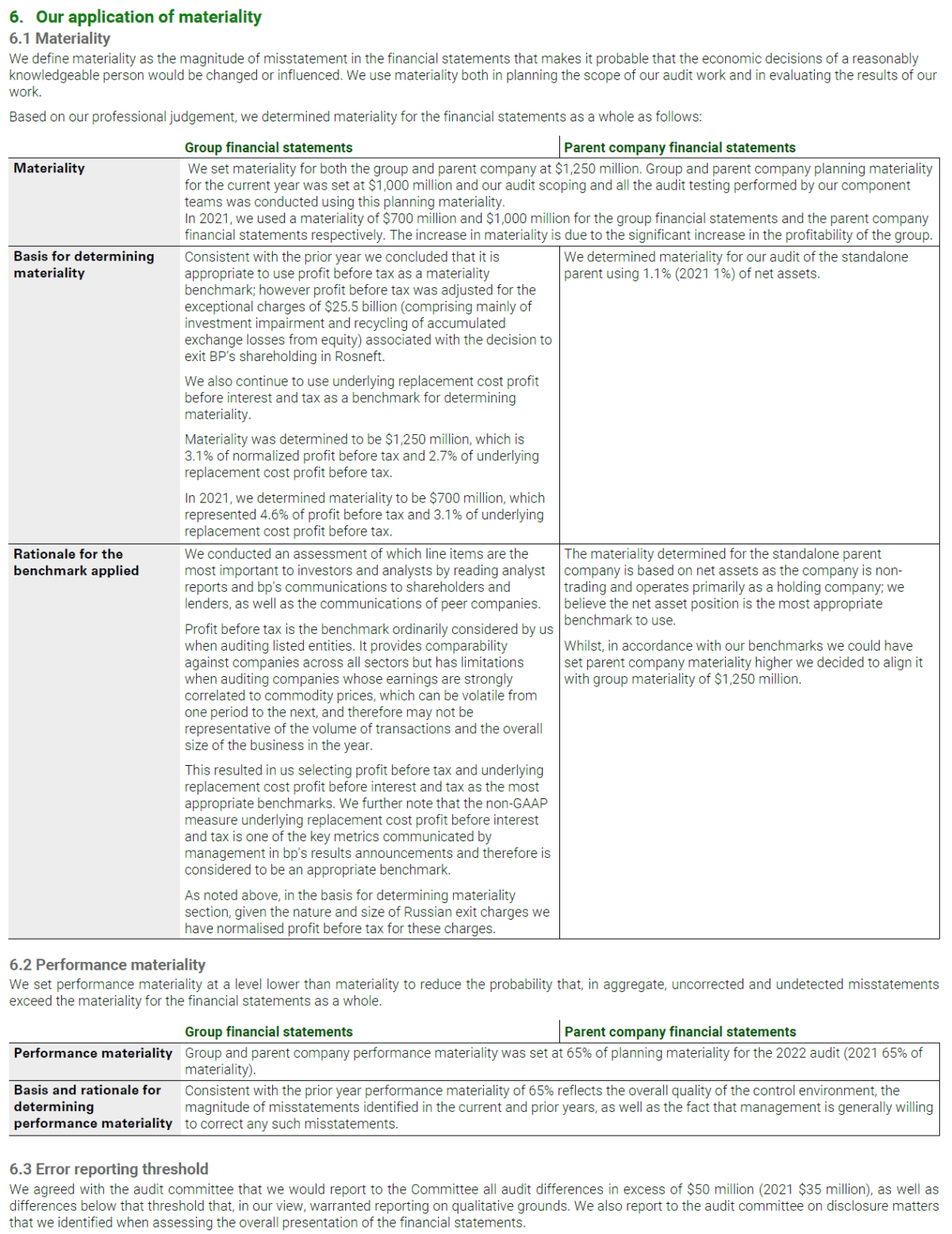

The UK International Standard on Auditing 701 mandates auditors to disclose overall materiality and performance materiality (refer to ISA 320.10-11 for definitions) in their audit reports, together with a rationale for the significant judgements made in the process (ISA UK 701.16-1). Such disclosures offer insights into auditors’ materiality assessments, as shown in this extract from BP’s audit report:

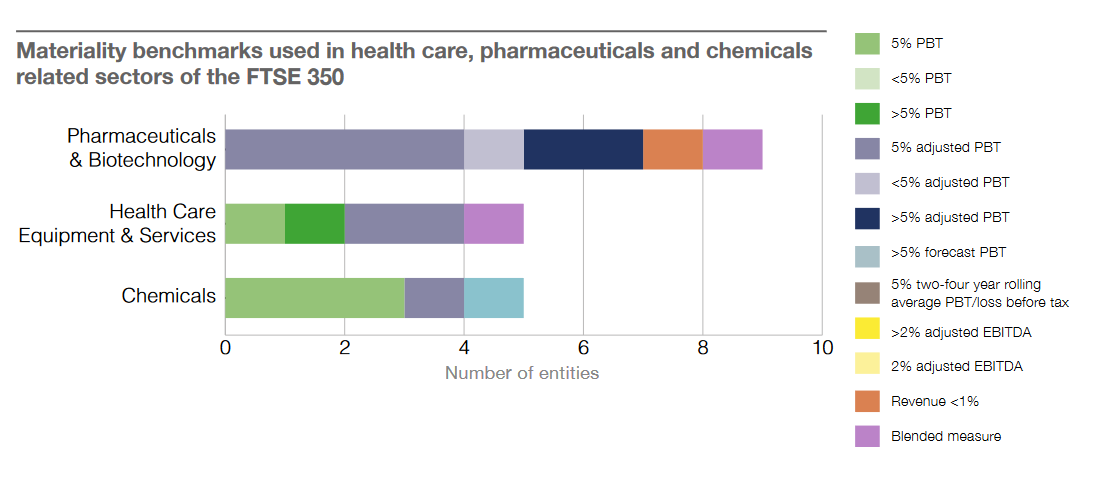

The UK Financial Reporting Council shared interesting findings from its Audit Quality Thematic Review on frequently used materiality benchmarks across various sectors. For instance, there is a summary of benchmarks used within the healthcare, pharmaceuticals and chemicals sectors in selected audit reports:

I always recommend that my clients set their own internal quantitative thresholds when assessing materiality. Ideally, this should align with the materiality assessments of their auditors. Different materiality levels are usually set for items affecting P/L, balance sheet classifications, aggregations and disclosures.

IFRSs mandate both individual and collective assessments of materiality. Thus, an immaterial item might become material when combined with other individually insignificant items. Therefore, it’s essential to keep track of all uncorrected misstatements identified during a period to determine their collective materiality. Importantly, a material misstatement cannot be balanced by another misstatement. For instance, overstated expenses don’t offset overstated revenue when assessing materiality of these misstatements.

Over time, the combined effect of previously immaterial misstatements might become material. For example, failing to recognise a yearly $1,000 liability for a decade leads to an understatement of liabilities by $10,000. Even if $1,000 might be immaterial annually, the accumulated understatement might become material over time. In such scenarios, entities can’t recognise a $10,000 liability and expense in the current period if doing so would materially distort the current year P/L. Thus, entities should correct such errors retrospectively, even if they weren’t material in any of the previous years.

Qualitative considerations

It’s important to realise that an item isn’t immaterial solely because it falls below a specified quantitative threshold. For instance, if a misstatement is deliberately made to achieve a specific presentation or outcome, it’s considered material, regardless of its monetary value (IAS 8.8/41). This shouldn’t be confused with simplifications that an entity might adopt, as these aren’t aimed at achieving a particular presentation or outcome.

When assessing materiality, qualitative factors to consider include:

- Whether misstatements allow the entity to meet financial projections, either its own or market consensus.

- Whether misstatements enable the entity to comply with regulatory requirements, debt covenants or contractual obligations.

- The ability of misstatements to turn net losses into profits or boost managerial bonuses.

- Misstatements that significantly distort segment reporting, MPMs, related party disclosures or other specific financial reporting aspects, even if they have a minor quantitative effect on the overall financial statements.

There’s also the notion of ‘obscuring’ material information, which means presenting it in a manner similar to omitting or wrongly stating that information. Examples of situations that may lead to the obscuring of material information include (IFRS 18.B3 / IAS 1.7):

- Disclosing details about a material item in unclear or ambiguous language.

- Scattering information about a material item throughout the financial statements.

- Inappropriately aggregating dissimilar items or disaggregating similar ones.

- Overloading the financial statements with immaterial information to the point where a user struggles to discern the material content.

Interim financial statements

Materiality thresholds will be lower in interim financial statements. Under IAS 34, materiality should be based on interim results, not anticipated full-year outcomes (IAS 34.IN9, 23, 25). For instance, the materiality threshold for the first quarter is only one-quarter of the threshold applied in annual financial statements.

Is it possible to maintain annual materiality levels in interim statements and still comply with IFRS? The answer is no, as IAS 34 is unambiguous on this matter. Interestingly, US GAAP is more flexible, permitting the use of annual materiality thresholds in interim financial statements, provided there is additional disclosure for items material only for the interim period (ASC 270-10-45-16 and ASC 250-10-45-27).