For many businesses, tracking the movement of identical inventory items on a unit-by-unit basis would be impossible. As a result, IAS 2 permits the use of either the first-in, first-out (FIFO) method or a weighted average cost formula to represent movements of interchangeable inventories.

Let’s dive in.

Interchangeable inventories

The cost of interchangeable inventories, which aren’t allocated for a specific project, should be determined using either the FIFO or weighted average cost formula. The chosen formula should be consistently applied to all inventories of a similar nature and use to the entity (IAS 2.25-26).

--Too many IFRS updates? I know the feeling! That's why I created Reporting Period. It's a concise monthly summary of IFRS developments and Big 4 insights for accounting professionals. It's completely free, with zero spam, and you can unsubscribe anytime with one click. Interested? Leave your email below:

FIFO method

Under the FIFO method, the earliest purchased or produced inventories are assumed to be sold first. As a result, items still held in inventory at the reporting date are those most recently acquired or produced (IAS 2.27).

Example: FIFO method

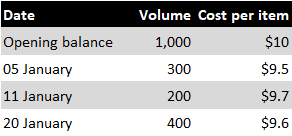

On 1 January 20X1, Entity A has 1,000 units of product X, each costing $10. During the month, it makes the following purchases:

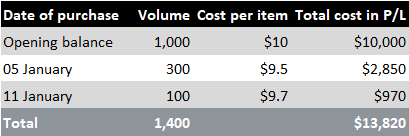

By the end of January 20X1, Entity A has sold 1,400 units of product X, leaving 500 units in inventory. Using the FIFO method, those 500 units comprise 400 items purchased on 20 January at $9.6 each and 100 items purchased on 11 January at $9.7 each. The cost of goods sold is $13,820, calculated as follows:

Weighted average cost

The weighted average cost method calculates the cost of each inventory item from the weighted average cost of similar items at the start and throughout a period. It can be determined periodically or upon each delivery (IAS 2.27).

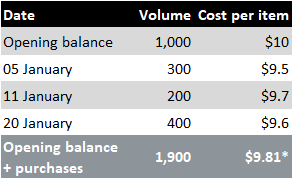

On 1 January 20X1, Entity A holds 1,000 units of product X, each with an average cost of $10. During the month, it makes the following purchases and calculates the average cost per item as follows:

* Refer to the downloadable Excel file.

By the end of January, 1,500 units of product X have been sold, leaving 400 units in inventory. These 400 units are valued at $3,924 (400 x $9.81), and the cost of the 1,500 units sold is $14,715 (1,500 x $9.81).

LIFO method

The LIFO method (last-in, first-out) is not permitted under IFRS, as explained in IAS 2.BC9-BC21.

Inventories that are not interchangeable

Inventories that aren’t typically interchangeable should have their costs specifically identified. This approach also applies to items designated for a particular project (IAS 2.23-24).

Consignment arrangements

Inventories delivered to another party (like a dealer or distributor) under a consignment arrangement remain on the delivering party’s statement of financial position until the criteria for revenue recognition are satisfied.

Recognition in P/L

When inventories are sold, their carrying amount is recognised as an expense in the same period as the related revenue. If inventories are used to create other assets, they form part of the cost of those assets.

Another situation in which the cost of inventories is recognised in P/L is when they are written down to net realisable value, together with any subsequent reversal of that write-down (IAS 2.34-35).

More about IAS 2

See other pages relating to IAS 2:

IAS 2: Scope, Definitions and Disclosure

IAS 2: Cost of Inventories

IAS 2: Cost Formulas (FIFO, LIFO and Weighted Average Cost)

IAS 2: Net Realisable Value (NRV)