Under IAS 2, inventories are measured at the lower of cost and net realisable value (IAS 2.9). The cost of inventories includes all costs of purchase, conversion, and other costs incurred in bringing the inventories to their present location and condition.

Let’s dive in.

Purchase costs

The purchase costs of inventories include the purchase price, import duties, and other taxes (excluding those subsequently recoverable by the entity from the tax authorities), alongside transport and handling fees. Other costs directly attributable to the acquisition of finished goods or materials are also included. Trade discounts, rebates, and similar items are deducted in establishing the purchase costs (IAS 2.11).

Discounts and rebates

Contractual rebates and discounts are anticipated if it is probable that they have been earned or will take effect. Discretionary (i.e. not contractual) rebates and discounts are not anticipated. This is not covered explicitly in IAS 2 but can be applied by analogy from IAS 34 (IAS 34.B23). Consider the example below.

Example: Accrued contractual volume rebates

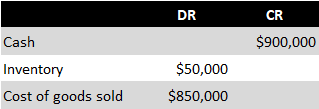

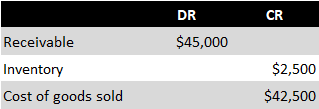

On 1 January 20X1, Entity A, a retailer, signs a 2-year contract with a supplier of product X. According to the agreement, Entity A acquires product X for $100 per item. The agreement stipulates that Entity A will receive a $5 rebate for each item purchased (applied retrospectively to all purchases) if it procures at least 10,000 products over the 2-year contract term. During 20X1, Entity A bought 9,000 products, with 8,500 of these already sold to customers. As of 31 December 20X1, Entity A determines it is probable it will earn the rebate, as product X sales increased during the second half of 20X1. The rebate is contractual, therefore Entity A accrues it in its financial statements for 20X1.

Entries made by Entity A are as follows:

Entity A bought 9,000 products for $100 per item, of which 8,500 were sold:

Entity A accrues the contractual rebate of $5 per product:

--

Too many IFRS updates? I know the feeling! That's why I created Reporting Period. It's a concise monthly summary of IFRS developments and Big 4 insights for accounting professionals. It's completely free, with zero spam, and you can unsubscribe anytime with one click. Interested? Leave your email below:

Example: Discretionary volume rebates

On 1 January 20X1, Entity A, a retailer, enters into a 3-year contract with a supplier of product Q. According to the agreement, Entity A buys product Q for $60 per item. The supplier of product Q typically grants volume rebates to entities that make high-volume purchases. However, these rebates are discretionary and entirely subject to the judgement of the supplier. During 20X1, Entity A purchased 14,000 products. As of 31 December 20X1, Entity A assesses that it is probable that it will receive a rebate after the 3-year contract period. However, since the rebate is non-contractual, Entity A does not accrue it in its financial statements for 20X1. If the amount is material, Entity A discloses it as a contingent asset.

Conversion costs

Conversion costs of internally produced inventories incorporate three main components under IAS 2.12:

- Costs directly linked to units of production, such as direct materials used.

- Systematic allocation of variable production overheads.

- Systematic allocation of fixed production overheads.

Variable production overheads

Variable production overheads refer to indirect production costs that fluctuate with the volume of production. These overheads may include indirect materials or labour (IAS 2.12). Such costs are allocated to each unit of production based on the actual use of production facilities (IAS 2.13). However, any abnormal quantities of wasted materials or other inefficiencies are charged to profit or loss as they are incurred (IAS 2.16(a)).

Fixed production overheads

Fixed production overheads are indirect production costs that remain relatively constant, irrespective of production volume. Examples include depreciation and maintenance of factory buildings and equipment used in the production process, as well as factory management and administrative costs. These overheads are allocated to each unit of production based on the normal capacity of the production facilities.

In practice, the actual level of production is often used as normal capacity. However, adjustments must be made for idle periods (for example, due to a lack of purchase orders) or unforeseen repairs. These adjustments result in the immediate recognition of the relevant fixed production overheads in P/L, rather than in the cost of inventories (IAS 2.13).

Note that IAS 2 requires production overheads to be allocated (entities can’t choose to exclude them from the cost of inventory).

Joint products and by-products

IAS 2.14 addresses the determination of conversion costs when the production process results in more than one product. This is relevant where joint products are produced, or where there is a main product and a by-product. If the costs of converting each product are not separately identifiable, they should be allocated between the products on a rational and consistent basis.

One such basis might be the relative sales value of each product. If the value of the by-product is immaterial, it may be measured at net realisable value, with that amount deducted from the cost of the main product.

Other costs

Under IAS 2, costs beyond those of purchase or conversion that are incurred in bringing the inventories to their present location and condition can be included in their carrying amount (IAS 2.15). These may encompass non-production overheads or costs of design for specific customers. However, IAS 2.16 requires specific costs to be excluded from the cost of inventories:

- Abnormal amounts of wasted materials, labour or other production costs.

- Storage costs, unless necessary for the production process prior to another production stage.

- Administrative overheads that do not contribute to bringing inventories to their present location and condition.

- Selling costs.

Storage costs

Storage costs are generally excluded from the cost of inventories, except when necessary for the production process before a further production stage. Thus, storing finished goods in a warehouse or materials and work-in-progress due to timing mismatches (such as storing bricks before their transfer to a construction site) does not increase their cost. An exception to this rule includes inventory items such as maturing alcoholic beverages (like wine) or certain types of food products (such as cheese), where storage is a necessary part of the production process.

Transportation costs

Transportation costs may be allocated to the cost of inventory if they are incurred ‘in bringing the inventories to their present location and condition’. However, they must not be classified as selling costs as these are specifically excluded from inventory costs (IAS 2.16(d)). The distinction can be challenging to make and different treatments may apply where they can be justified. For instance, the cost of transporting materials and work-in-progress to a production facility can be incorporated into the cost of finished goods.

Likewise, the cost of transporting finished goods from the production facility or central warehouses to retail outlets can also be added to inventory costs as these expenses are necessary ‘in bringing the inventories to their current location’ to facilitate the sale. Conversely, relocating inventory between retail outlets to meet local demand, or transporting items from retail outlets to customer premises, is more likely to be categorised as selling activities and should therefore be expensed in P/L as incurred.

Non-production overheads

According to IAS 2.15, it’s appropriate to incorporate non-production overheads into the cost of inventories, provided those costs are ‘incurred in bringing the inventories to their present location and condition’. In practice, this allows a broad range of non-production overheads to be allocated to inventory. Consequently, each entity must establish its own policy based on rational criteria and materiality. Nevertheless, general administrative and corporate overheads can never be included in the cost of inventories.

Financing component

When inventories are purchased on credit terms that significantly deviate from normal credit terms (e.g. where the credit period is much longer than the industry average), inventory costs are recognised based on the purchase price under standard credit terms. The difference between the standard credit terms and the actual amounts paid is recognised as interest expense over the financing period (IAS 2.18).

Under IAS 23, inventories can be qualifying assets if they meet the relevant criteria. However, entities can use the scope exemption for inventories manufactured or produced in large quantities on a repetitive basis.

Measurement techniques

IAS 2 permits the use of approximations when determining the cost of inventories, including the standard cost method and the retail method (IAS 2.21-22).

The standard cost method takes account of typical levels of materials, labour, efficiency and capacity utilisation.

The retail method, as the name suggests, is commonly used in the retail sector to measure the cost of inventories with high turnover and similar margins. Under this method, inventory cost is determined by converting selling prices to cost by adjusting for a normal margin.

Initial recognition

IAS 2 does not provide specific guidance on the precise timing for the recognition of purchased inventories. Consequently, entities typically refer to the principles of revenue recognition to determine when inventory should be recognised. According to this approach, inventory is recognised at the point when an entity gains control over it.

A key factor in determining when control of inventory is transferred to the entity is the shipping terms agreed upon in the transaction. These terms usually specify the moment at which the entity acquires legal title and the associated risks and rewards of ownership, along with an immediate obligation to pay.

For example, under free on board (FOB) terms, control is typically considered to pass to the buyer when the goods are loaded onto the shipping vessel. This is evidenced by the receipt of the bill of lading and the assumption of the risk of loss or damage from that point. Therefore, goods purchased under FOB terms that are still in transit at the reporting date should nevertheless be included in inventory.

More about IAS 2

See other pages relating to IAS 2:

IAS 2: Scope, Definitions and Disclosure

IAS 2: Cost of Inventories

IAS 2: Cost Formulas (FIFO, LIFO and Weighted Average Cost)

IAS 2: Net Realisable Value (NRV)