IFRS 8 requires entities whose securities are publicly traded, or that are taking steps to issue securities for public trading (see Scope), to provide additional information in their financial statements. This information is intended to give users a clearer understanding of the entity’s business activities and financial performance.

Let’s dive in.

Defining an operating segment

Under IFRS 8.5, an operating segment is a component of an entity that:

- engages in business activities from which it may earn revenues and incur expenses, including revenues and expenses relating to transactions with other components of the same entity;

- has operating results that are regularly reviewed by the entity’s chief operating decision maker for the purposes of allocating resources and assessing performance; and

- has discrete financial information available.

An operating segment may carry out activities that do not yet generate revenue. For example, a start-up operation may be an operating segment before it begins earning revenue.

The identification of operating segments involves determining the entity’s ‘chief operating decision maker’ (CODM). The CODM represents a function rather than a specific managerial position. That function comprises the allocation of resources to operating segments and the assessment of their performance. Depending on the entity’s governance and management structure, the CODM may be the chief executive officer, the chief operating officer, a group of executive directors or another individual or group.

Where an entity presents its business activities in different ways and the CODM uses more than one set of segment information, other factors may determine which set constitutes the entity’s operating segments. These factors include the nature of the business activities, the existence of managers responsible for the components and the information presented to the board.

An operating segment generally has a ‘segment manager’ who reports directly to the CODM and maintains regular contact with the CODM regarding the segment’s operations, financial results, forecasts and plans. Like the CODM, the segment manager is identified by reference to their function rather than a specific title. The CODM may also act as the segment manager for particular operating segments, and one segment manager may be responsible for more than one operating segment.

Where these characteristics apply to more than one set of components within an organisation, but only one set has managers who are accountable for the components, that set constitutes the operating segments. In a matrix organisation, responsibilities may overlap across product lines and geographical areas. Where the CODM regularly reviews both sets of components and discrete financial information is available for each, the entity must determine its operating segments by applying the core principle of IFRS 8. The identification of the operating segments should therefore reflect how the entity is managed and how financial information is presented for the purposes of allocating resources and assessing performance (IFRS 8.6-10).

--Too many IFRS updates? I know the feeling! That's why I created Reporting Period. It's a concise monthly summary of IFRS developments and Big 4 insights for accounting professionals. It's completely free, with zero spam, and you can unsubscribe anytime with one click. Interested? Leave your email below:

Distinguishing between operating and reportable segments

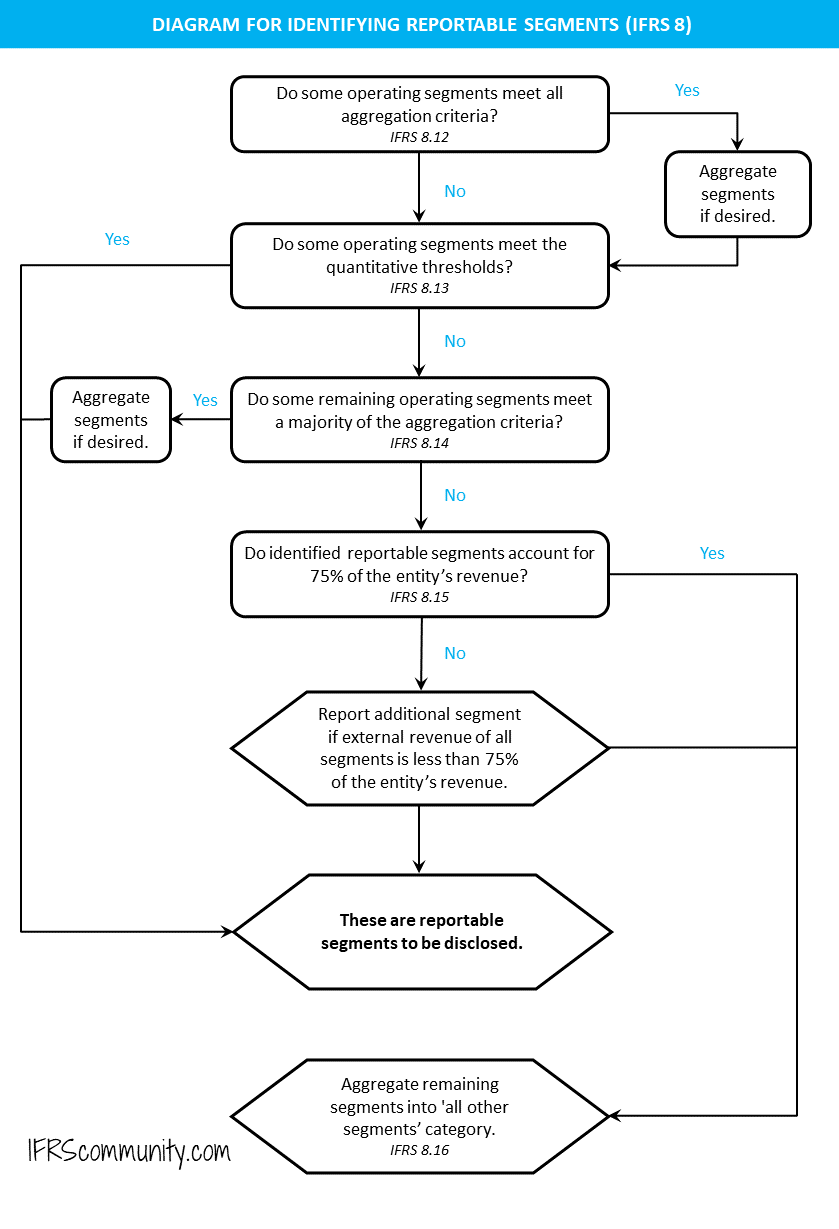

Not every identified operating segment must be reported separately (IFRS 8.11). IFRS 8 establishes quantitative thresholds for determining reportable segments and sets out separate criteria for the aggregation of operating segments. IFRS 8.IG7 includes a helpful diagram illustrating the process for identifying reportable segments:

Quantitative thresholds

An operating segment must be reported separately if it meets any of the following criteria (IFRS 8.13):

- its reported revenue, including inter-segment sales or transfers, is at least 10% of the combined internal and external revenue of all operating segments;

- the absolute amount of its reported profit or loss is at least 10% of the greater, in absolute terms, of the combined reported profit of all profitable segments and the combined reported loss of all loss-making segments; or

- its assets represent at least 10% of the combined assets of all operating segments.

If the combined external revenue of the reportable segments is less than 75% of the entity’s total external revenue, additional operating segments must be identified as reportable segments until the 75% threshold is met (IFRS 8.15).

There is also a practical consideration regarding the number of reportable segments, as reporting too many segments may result in excessively detailed information. IFRS 8 does not prescribe a fixed limit. However, where the number of reportable segments exceeds ten, the entity should consider whether a practical limit has been reached (IFRS 8.19).

Aggregation criteria

Two or more operating segments may be aggregated into a single operating segment if the aggregation is consistent with the core principle of IFRS 8. Aggregation is permitted where the segments have similar economic characteristics and are similar in each of the following respects:

- the nature of their products and services,

- the nature of their production processes,

- the type or class of customer for their products and services,

- the methods used to distribute their products or provide their services, and

- where applicable, the nature of the regulatory environment.

Applying these criteria may allow the entity to present segment information in a more streamlined and coherent manner (IFRS 8.12).

Disclosure of segment information

The fundamental objective of the disclosure of segment information under IFRS 8 is to help users of financial statements understand the nature and financial effects of an entity’s business activities and the economic environments in which it operates (IFRS 8.20). Importantly, IFRS 8 does not permit exemptions from these disclosure requirements on the grounds of potential ‘competitive harm’ (IFRS 8.BC43-45).

Entities must disclose the factors used to identify their reportable segments. This includes the basis of organisation and any judgements made in applying the criteria for aggregation. Entities must also provide a clear description of the business activities of each reportable segment (IFRS 8.22).

For each reportable segment, IFRS 8.23 requires an entity to disclose:

- a measure of profit or loss;

- total assets and liabilities, but only if those amounts are regularly provided to the CODM;

- the specified items listed in IFRS 8.23, if they are included in the measure of segment profit or loss reviewed by the CODM or are otherwise regularly provided to the CODM, even if they are not included in that measure; and

- additions to non-current assets, often referred to as ‘capex’, if they are included in the measure of segment assets reviewed by the CODM or are otherwise regularly provided to the CODM, even if they are not included in that measure (IFRS 8.24).

An entity isn’t required to disclose measures of segment performance that combine information relating to profit or loss, cash flows and financial position, even if those measures are provided to the CODM. In practice, however, entities frequently disclose such measures, particularly where they form part of other financial information presented to analysts. Common examples include return on capital employed (ROCE), the ratio of net debt to EBITDA and free cash flow (FCF).

Measuring segment information

The fundamental principle for the measurement of segment information is that the reported amounts should correspond to those provided to the CODM. Consequently, they may not always align with the amounts presented in the primary financial statements (IFRS 8.25-26).

This reflects the management approach underlying the requirements for segment reporting in IFRS 8, under which users are presented with the entity from the perspective of management. Entities must therefore explain the measurement of segment profit or loss, assets and liabilities for each reportable segment. IFRS 8.27 specifies the information that must be included in those explanations.

Reconciliations

Entities must reconcile the segment measures to the corresponding amounts in the primary financial statements (IFRS 8.28). The reconciliation doesn’t need to be presented separately for each individual segment (IFRS 8.BC42). IFRS 8.IG4 provides an example of such a reconciliation.

Additional requirements apply to management-defined performance measures (MPMs) under IFRS 18.

Entity-wide disclosures

IFRS 8 requires certain entity-wide disclosures (IFRS 8.31-34), including information about products and services, revenue attributed to foreign countries and non-current assets located in foreign countries. IFRS 8.IG5 illustrates these disclosures.

Entities must also disclose information about the extent of their reliance on major customers, including groups of entities known to be under common control.

Scope of IFRS 8

Scope overview

IFRS 8 applies to the separate and consolidated financial statements of entities whose securities are publicly traded or that are taking steps to issue securities for public trading (IFRS 8.2). Where both separate and consolidated financial statements are presented in a single financial report, segment information is required only in the consolidated financial statements (IFRS 8.4).

Interim financial statements

IFRS 8 introduced a consequential requirement in IAS 34 for the disclosure of selected segment information in interim financial statements (IAS 34.16A(g)).

Interaction with IAS 36

The identification of operating segments has implications for impairment testing. In particular, IAS 36.80(b) states that each cash-generating unit, or group of cash-generating units, to which goodwill is allocated must not be larger than an operating segment before aggregation.