IAS 1 outlines the general requirements for presenting financial statements. It is applicable to ‘general purpose financial statements’, which are designed to meet the informational needs of users who cannot demand customised reports from an entity. Documents like management commentary or sustainability reports, which are often included in annual reports, fall outside the scope of IFRS, as indicated in IAS 1.13-14. Similarly, financial statements submitted to a court registry are not considered general purpose financial statements (IAS 1.BC11-13).

The standard primarily focuses on annual financial statements, but its guidelines in IAS 1.15-35 also extend to interim financial reports (IAS 1.4). These guidelines address key elements such as fair presentation, compliance with IFRS, the going concern principle, the accrual basis of accounting, offsetting, materiality, and aggregation. For comprehensive guidance on interim reporting, please refer to IAS 34.

Note that IAS 1 will be superseded by IFRS 18 Presentation and Disclosure in Financial Statements.

Let’s dive in.

Financial statements

Components of a complete set of financial statements

Paragraph IAS 1.10 outlines the elements that make up a complete set of financial statements. Companies have the flexibility to use different titles for these documents, but each statement must be presented with equal prominence (IAS 1.11). The terminology used in IAS 1 is tailored for profit-oriented entities. However, not-for-profit organisations or entities without equity (as defined in IAS 32), may use alternative terminology for specific items in their financial statements (IAS 1.5-6).

--Too many IFRS updates? I know the feeling! That's why I created Reporting Period. It's a concise monthly summary of IFRS developments and Big 4 insights for accounting professionals. It's completely free, with zero spam, and you can unsubscribe anytime with one click. Interested? Leave your email below:

Compliance with IFRS

Financial statements must include an explicit and unreserved statement of compliance with IFRS in the accompanying notes. This statement is only valid if the entity adheres to all the requirements of every IFRS standard (IAS 1.16). In many jurisdictions, such as the European Union, laws mandate compliance with a locally adopted version of IFRS.

IAS 1 does consider extremely rare situations where an entity might diverge from a specific IFRS requirement. Such a departure is permissible only if it prevents the presentation of misleading information that would conflict with the objectives of general-purpose financial reporting (IAS 1.20-22). Alternatively, entities can disclose the impact of such a departure in the notes, explaining how the statements would appear if the exception were made (IAS 1.23).

Identification of financial statements

The guidelines for identifying financial statements outlined in IAS 1.49-53 are straightforward and rarely cause issues in practice.

Going concern

The ‘going concern’ principle is a cornerstone of IFRS and other major GAAP. It assumes that an entity will continue to operate for the foreseeable future (at least 12 months). IAS 1 mandates management to assess whether the entity is a ‘going concern’. Should there be any material uncertainties regarding the entity’s future, these must be disclosed (IAS 1.25-26). IFRSs do not provide specific accounting principles for entities that are not going concerns, other than requiring disclosure of the accounting policies used. One of the possible approaches is to measure all assets and liabilities using their liquidation value.

Further reading:

- Educational material of the IFRS Foundation.

- UK FRC’s guidance.

Materiality and aggregation

IAS 1.29-31 emphasise the importance of materiality in preparing user-friendly financial statements. While IFRS mandates numerous disclosures, entities should only include information that is material. This concept should be at the forefront when preparing financial statements, as reminders about materiality are seldom provided in other IFRS standards or publications.

Offsetting

Generally, entities should not offset assets against liabilities or income against expenses unless a specific IFRS standard allows or requires it. IAS 1.32-35 offer guidance on what can and cannot be offset. Offsetting of financial instruments is discussed further in IAS 32.

Frequency of reporting

Entities are required to present a complete set of financial statements at least annually (IAS 1.36). However, some Public Interest Entities (PIEs) may be obliged to release financial statements more frequently, depending on local regulations. However, these are typically interim financial statements compiled under IAS 34.

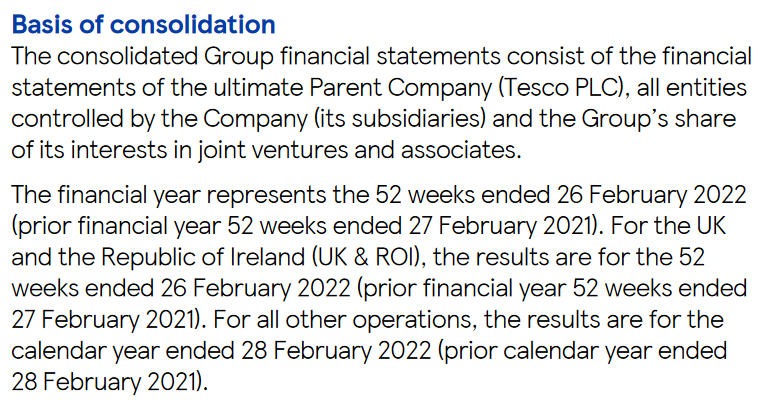

IAS 1 also allows for a 52-week reporting period instead of a calendar year (IAS 1.37). This excerpt from Tesco’s annual report serves to demonstrate this point, showing that the group uses 52-week periods for their financial year, even when some subsidiaries operate on a calendar-year basis:

If an entity changes its reporting period, it must clearly disclose this modification and provide the rationale for the change (IAS 1.36). It is advisable to include an explanatory note with comparative data that aligns with the new reporting period for clarity.

Comparative information

As a general guideline, entities should present comparative data for the prior period alongside all amounts reported for the current period, even when specific requirements in a given IFRS do not require it. However, there’s no obligation to include narrative or descriptive information about the preceding period if it isn’t necessary for understanding the current period (IAS 1.38).

If an entity opts to provide comparative data for more than the immediately preceding period, this additional information can be included in selected primary financial statements only. However, these additional comparative periods should also be detailed in the relevant accompanying notes (IAS 1.38C-38D).

IAS 1.40A-46 outlines how to present the statement of financial position when there are changes in accounting policies, retrospective restatements, or reclassifications. This entails producing a ‘third balance sheet’ at the start of the preceding period (which may differ from the earliest comparative period, if more than one is presented). Key points to note are:

- The third balance sheet is required only if there’s a material impact on the opening balance of the preceding period (IAS 1.40A(b)).

- If a third balance sheet is presented, there’s no requirement to add a corresponding third column in the notes, although this could be useful where numbers have been altered by the change (IAS 1.40C).

- Interim financial statements do not require a third balance sheet (IAS 1.BC33).

IAS 8 also requires comprehensive disclosures concerning changes in accounting policies and corrections of errors.

Statement of financial position

IAS 1.54 enumerates the line items that must, at a minimum, appear in the statement of financial position. Entities should note that separate lines are not required for immaterial items (IAS 1.31). Additional line items can be added for entity-specific or industry-specific matters. IAS 1 permits the inclusion of subtotals, provided the criteria set out in IAS 1.55A are met.

Additional disclosure requirements are set out in IAS 1.77-80A. Of particular interest are the requirements relating to equity (IAS 1.79), which begin with the number of shares and extend to include details such as ‘rights, preferences, and restrictions relating to share capital, including restrictions on the distribution of dividends and the repayment of capital.’ While these kinds of limitations are common across various legal jurisdictions (for example, not all retained earnings can be distributed as dividends), many companies neglect to disclose such limitations in their financial statements.

For guidance on classifying assets and liabilities as either current or non-current, please refer to the separate page dedicated to this topic.

Statement of profit or loss and other comprehensive income

IAS 1 provides two methods for presenting profit or loss (P/L) and other comprehensive income (OCI). Entities can either combine both P/L and OCI into a single statement or present them in separate statements (IAS 1.81A-B). Additionally, the P/L and total comprehensive income for a given period should be allocated between the owners of the parent company and non-controlling interests (IAS 1.81B).

Minimum contents in P/L and OCI

IAS 1.82-82A specifies the minimum items that must appear in the P/L and OCI statements. These items are required only if they materially impact the financial statements (IAS 1.31).

Finance costs

IAS 1 requires finance costs to be presented on the face of the income statement but doesn’t define the term. IFRS 7.IG13 clarifies that finance costs may also include amounts related to non-financial liabilities. In practice, this means finance costs include expenses recognised on non-financial liabilities, such as the unwinding of discount on long-term employee benefits.

Subtotals

Entities are permitted to add subtotals to the P/L statement if they meet the criteria specified in IAS 1.85A. Operating income is often the most commonly used subtotal in P/L. This practice may be attributed to the 1997 version of IAS 1, which mandated the inclusion of this subtotal—although this is no longer the case. IAS 1.BC56 clarifies that an operating profit subtotal should not exclude items commonly considered operational, such as inventory write-downs, restructuring costs, or depreciation/amortisation expenses.

Profit or loss (P/L)

All items of income and expense must be recognised in P/L (or OCI). This means that no income or expenses should be recognised directly in the statement of changes in equity, unless another IFRS specifically mandates it (IAS 1.88). Direct recognition in equity may also result from intra-group transactions. IAS 1.97-98 require separate disclosure of material items of income and expense, either directly in the income statement or in the notes.

Expenses in P/L can be presented in one of two ways (IAS 1.99-105):

- By their nature (e.g., depreciation, employee benefits); or

- By their function within the entity (e.g., cost of sales, distribution costs, administrative expenses).

When opting for the latter, entities must provide additional details on the nature of the expenses in the accompanying notes (IAS 1.104).

Other comprehensive income (OCI)

OCI encompasses income and expenses that other IFRS specifically exclude from P/L. There is no conceptual basis for deciding which items should appear in OCI rather than in P/L. Most companies present P/L and OCI as separate statements, partly because OCI is generally overlooked by investors and those outside of accounting and financial reporting circles. The concern is that combining the two could reduce net profit to merely a subtotal within total comprehensive income.

All elements that constitute OCI are specifically outlined in IAS 1.7, as part of its definitions.

Reclassification adjustments

A reclassification adjustment refers to the amount reclassified to P/L in the current period that was recognised in OCI in the current or previous periods (IAS 1.7). All items in OCI must be grouped into one of two categories: those that will or will not be subsequently reclassified to P/L (IAS 1.82A). Reclassification adjustments must be disclosed either within the OCI statement or in the accompanying notes (IAS 1.92-96).

To illustrate, foreign exchange differences arising on translation of foreign operations and gains or losses from certain cash flow hedges are examples of items that will be reclassified to P/L. In contrast, remeasurement gains and losses on defined benefit employee plans or revaluation gains on properties will not be reclassified to P/L.

The practice of transferring items from OCI to P/L, commonly known as ‘recycling’, lacks a concrete conceptual basis and the criteria for allowing such transfers in IFRS are often considered arbitrary.

Tax effects

OCI items can be presented either net of tax effects or before tax, with the overall tax impact disclosed separately. In either case, entities must specify the tax amount related to each item in OCI, including any reclassification adjustments (IAS 1.90-91). Interestingly, there is no such requirement to disclose tax effects for individual items in the income statement.

Statement of changes in equity

IAS 1.106 outlines the minimum line items that must be included in the statement of changes in equity. Subsequent paragraphs specify the disclosure requirements, which can be addressed either within the statement itself or in the accompanying notes. It’s crucial to note that changes in equity during a reporting period can arise either from income and expense items or from transactions involving owners acting in their capacity as owners (IAS 1.109). This means that entities cannot adjust equity directly due to changes in assets or liabilities unless these adjustments result from transactions with owners, such as capital contributions or dividend payments, or are otherwise mandated by other IFRSs.

Statement of cash flows

The statement of cash flows is governed by IAS 7.

Explanatory notes

Structure of explanatory notes

The structure for explanatory notes is detailed in IAS 1.112-116. In practice, there are several commonly adopted approaches to organising the financial statements:

Approach #1:

- Primary financial statements (P/L, OCI, etc.)

- Statement of compliance and basis of preparation

- Accounting policies

- Explanatory notes

Approach #1 is logically coherent, as understanding accounting policies is crucial before delving into the financial data. However, in reality, few people read the accounting policies in their entirety. Consequently, users often have to navigate past several pages of accounting policies to reach the explanatory notes.

Approach #2:

- Primary financial statements (P/L, OCI, etc)

- Statement of compliance and basis of preparation

- Explanatory notes

- Accounting policies

In Approach #2, accounting policies are treated as an appendix and positioned at the end of the financial statements. The advantage here is that all numerical data is clustered together, uninterrupted by extensive descriptions of accounting policies.

Approach #3:

- Primary financial statements (P/L, OCI, etc)

- Statement of compliance and basis of preparation

- Explanatory notes integrated with relevant accounting policies

Approach #3 pairs accounting policies directly with the associated explanatory notes. For example, accounting policies relating to inventory would appear alongside the explanatory note that breaks down inventory components.

Management of capital

IAS 1.134-136 outline the disclosures related to capital management. These provisions apply to all entities, whether or not they are subject to external capital requirements. An important note here is that entities are not obligated to disclose specific values or ratios concerning capital objectives or requirements.

Dividends

IAS 1.137 mandates disclosure of dividends proposed or declared before the financial statements were authorised for issue but not recognised as a distribution to owners during the period. Furthermore, entities are required to disclose the amount of any cumulative preference dividends not recognised.

Disclosure of accounting policies

IAS 1 specifies the requirements for disclosing accounting policy information which are discussed here.

Disclosing judgements and sources of estimation uncertainty

IAS 1 mandates disclosing judgements and sources of estimation uncertainty.

Other disclosures

Additional miscellaneous disclosure requirements are detailed in paragraphs IAS 1.138.

IFRS 18 Presentation and Disclosure in Financial Statements

On 9 April 2024, the IASB issued IFRS 18 Presentation and Disclosure in Financial Statements, which replaces IAS 1 and amends IAS 7. This new standard will be effective from 2027 with early application permitted.

Here are the key changes under IFRS 18:

- Two new subtotals have been added to the income statement: ‘Operating Profit’ and ‘Profit Before Financing and Income Taxes’. This change requires companies to categorise income and expenses into operating, investing, and financing activities.

- A new requirement mandates the reconciliation of non-GAAP measures with IFRS-specified subtotals, but this only applies to P/L measures such as adjusted profit. Other metrics like free/organic cash flow or net debt are not included.

- The statement of cash flows will start with operating profit for the indirect method, and the classification of cash flows related to interest and dividends has been standardised. Typically, dividends and interest paid will fall under financing activities, while those received will be recorded under investing activities.

While many IAS 1 provisions remain under IFRS 18, others, including the basis of financial statement preparation and disclosure of accounting policies, have moved to IAS 8, which will be retitled Basis of Preparation of Financial Statements.

For further insights see: