Employee benefits encompass all forms of compensation offered by a company in exchange for services performed by employees, or upon the termination of employment. These benefits can arise from formal agreements between the company and the employee, be mandated by local laws (such as state pension plans), or stem from implied commitments. The benefits can be paid either in cash or in kind and may extend to an employee’s family members as well (IAS 19.4-7).

According to IAS 19.5, employee benefits are categorised into four main types:

- Short-term employee benefits.

- Post-employment benefits.

- Other long-term employee benefits.

- Termination benefits.

It’s worth noting that all types of employee benefits fall under the scope of IAS 19, with the exception of share-based payments.

Let’s dive in.

Short-term employee benefits

Definition of short-term employee benefits

Short-term employee benefits are those expected to be fully settled within 12 months after the end of the year in which the employee performed the service. As specified in IAS 19.9, these benefits include:

- Wages, salaries, bonuses (including profit-sharing) and social security contributions,

- Paid absences,

- Free or subsidised non-monetary benefits, such as medical care and housing.

The term ‘fully settled’ is important to note, as it distinguishes these benefits from long-term benefits. Therefore, even if certain arrangements, like bonuses, appear similar to short-term benefits, they should be accounted for as other long-term benefits if they are not fully settled within the 12-month time frame.

--Too many IFRS updates? I know the feeling! That's why I created Reporting Period. It's a concise monthly summary of IFRS developments and Big 4 insights for accounting professionals. It's completely free, with zero spam, and you can unsubscribe anytime with one click. Interested? Leave your email below:

Recognition of short-term employee benefits

According to IAS 19.11, a short-term employee benefit is recognised when an employee provides a service. This is typically recognised as an expense, unless it can be capitalised as part of an asset’s cost (e.g., inventories or property, plant, and equipment).

Short-term paid absences

Paid absences commonly include holidays, sick leave, and maternity leave. IAS 19 differentiates between accumulating and non-accumulating paid absences. Accumulating absences are those which can be carried over for future use if not fully utilised in the current period (IAS 19.15). Holidays usually fall under this category, although this may vary between countries. Non-accumulating paid absences, like sick or maternity leave, do not carry forward and expire if not used within the current period. Additionally, they don’t result in a cash payment upon an employee’s departure from the company (IAS 19.18).

For accumulating paid absences, entities should recognise the employee benefit expense as the employee earns their entitlement to a paid absence (IAS 19.13(a)). If these benefits are non-vesting—meaning an employee won’t receive a cash payment for unused leave upon departure—the expense should still be recognised, but adjusted for the expected unused absences (IAS 19.15).

In contrast, for non-accumulating paid absences, the expense should only be recognised when the absence actually occurs (IAS 19.13(a)).

Example: Holiday pay accrual (accumulating paid absence)

Employees at Entity A are entitled to 20 days of paid leave annually. Unused holidays can be carried over indefinitely but are non-vesting, meaning employees do not receive cash for unused days. Entity A uses software to track unused holidays for each employee.

For instance, as of 31 December 20X1, John Smith has 15 unused holiday days. His total annual remuneration is $60,000, comprising a salary of $50,000 and $10,000 in state-imposed levies paid by the employer. Given an average working year has 250 working days, one working day for John costs $240 ($60,000/250). Based on past experience, Entity A estimates that an average employee leaves the company with 2 unused holiday days. Hence, Entity A recognises a holiday pay accrual of $3,120 [$240 x (15 days – 2 days)]. This calculation is performed for each employee. If the holiday pay were vesting, the accrual would be for all 15 days.

Profit sharing and bonuses

Entities should recognise the expected costs of profit-sharing and bonuses when there’s either a legal or constructive obligation to make such payments, and the amount can be reliably estimated.

Profit-sharing plans where employees receive a share of the profits only if they stay with the entity for a specified period create a constructive obligation. This obligation arises as employees provide service that increases the payable amount, contingent on their continued employment until the end of the specified period. The measurement of such obligations must consider the likelihood of some employees leaving without receiving their profit-sharing payments.

Even in the absence of a legal obligation to pay bonuses, an entity may have a constructive obligation if it has a history or practice of paying bonuses, thereby leaving it with no realistic alternative but to make these payments. The measurement of this constructive obligation similarly reflects the possibility of employees departing without receiving a bonus. An entity can reliably estimate its legal or constructive obligations under a profit-sharing or bonus plan when there is a formula in the plan’s formal terms, when amounts are determined before the financial statements are authorised, or when past practices provide clear evidence of the obligation’s amount (IAS 19.19-22).

Under some national GAAP, profit-sharing payments are directly deducted from equity rather than being expensed. However, IAS 19 prohibits this practice, stating that employee profit-sharing plans do not constitute transactions with owners acting in their capacity as owners (IAS 19.23).

Post-employment benefits

Definition of post-employment benefits

Post-employment benefits are benefits provided to employees after their period of employment has ended. Examples include:

- Pensions,

- One-off payments upon retirement,

- Certain severance payments (note the distinction from termination benefits),

- Post-employment medical care.

Distinguishing between defined contribution and defined benefit plans

Post-employment benefit plans are classified as either defined contribution or defined benefit plans. The accounting treatment for each differs significantly, as detailed in IAS 19.26-49.

In a defined contribution plan, an entity contributes a fixed sum to a fund on behalf of the employee. The entity has no legal or constructive obligation to make additional payments, even if the fund lacks sufficient money to meet future benefits. A common example is a retirement plan where the employer contributes to an employee’s individual account, which is then invested. The eventual payouts to the employee depend on both the employer’s contributions and the investment returns. If the investments perform poorly, the employer is not required to contribute further.

Conversely, a defined benefit plan obliges the employer to provide a predetermined level of benefits to employees, irrespective of the contributions made. A classic example is a pension plan where the employer promises a monthly pension amount, bearing any actuarial or investment risks. For instance, a pension equalling 50% of the employee’s final salary is a defined benefit plan.

State-managed plans are usually funded on a pay-as-you-go basis. Future benefits for current employees are generally financed by future contributions from younger workers. Therefore, the entity has no obligation for these future payments, classifying most state plans as defined contribution plans (IAS 19.45).

Other long-term employee benefits

According to IAS 19.8, other long-term employee benefits are those that are neither short-term, post-employment, nor termination benefits. While these benefits might appear similar to short-term ones, they aren’t expected to be settled within 12 months following the end of the service year (e.g., multi-year bonuses or profit-sharing plans). For these, the accounting principles related to short-term benefits should be applied, including any necessary discounting.

However, accounting for certain other long-term employee benefits, like jubilee / anniversary bonuses, can be as complex as that for post-employment benefits. For these benefits, it’s vital to differentiate between defined benefit and defined contribution plans, and then follow the IAS 19 guidelines accordingly (IAS 19.153-158). Notably, actuarial gains or losses (remeasurements) for other long-term benefits are recognised in profit or loss, as opposed to OCI for post-employment benefits (IAS 19.156). Furthermore, IAS 19 doesn’t mandate specific disclosures for other long-term benefits.

Constructive obligation

IAS 19 specifies that an entity should account not just for the legal obligations stipulated in the terms of a defined benefit plan, but also for any constructive obligations arising from informal practices (IAS 19.61-62). A constructive obligation arises from the company’s informal practices that aren’t legally binding. Nevertheless, the standard assumes that if a company currently offers certain benefits, it will continue to do so throughout the employees’ remaining working lives, unless evidence suggests otherwise.

Defined contribution plans

Accounting for defined contribution plans is outlined in IAS 19.50-54 and is generally straightforward: the employee benefit is recognised when a service is rendered by the employee, much like regular wages. Typically, there is no need for actuarial valuations or discounting of future payments.

Entities are required to disclose the expense recognised for defined contribution plans. This requirement also applies to state-operated schemes that mandate additional contributions on top of an employee’s gross salary. However, it’s worth noting that entities seldom provide this disclosure.

Defined benefit plans

Accounting for defined benefit plans is considerably more complex, often requiring actuarial valuation through the projected unit credit method. This entails attributing benefits to specific service periods and making relevant actuarial assumptions. The rules governing defined benefit plans are covered in paragraphs IAS 19.55-152.

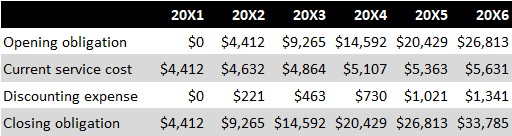

Example: Calculating defined benefit plan costs and obligations for a single employee

Let’s consider the case of John Smith, who joins a company on 31 December 20X0. All employees in this company are entitled to a one-off retirement payment equal to three months of their final monthly salary. The following facts and assumptions apply to this example:

- John Smith joins the company on 31 December 20X0.

- He will be eligible for retirement on 31 December 20X6.

- His starting salary is $10,000.

- The estimated annual salary increase rate is 2%.

- The projected salary at the retirement date is $11,262 ($10,000 x 1.02^6).

- The estimated retirement payment totals $33,785 (3 x $11,262).

- The discount rate is 5%.

Please refer to the included Excel file to view all calculations related to this example.

The current service cost represents the portion of the retirement payment earned by John Smith in a given year, discounted to its present value. Let’s examine the year 20X3 in greater detail.

John will be eligible for his retirement payment in six years (from 20X1 to 20X6). Consequently, he earns 1/6 of his retirement payment each year. Given the anticipated salary increase, John’s estimated salary at retirement will be $11,262, making his projected retirement payment $33,785. For the year 20X3, John earns 1/6 of this amount, which is $5,631. However, this sum will only be paid out on 31 December 20X6, so it needs to be discounted to its present value. After applying a 5% discount rate, the discounted value for the year 20X3 stands at $4,864.

Besides the current service cost, entities also recognise a discounting expense. This is similar to the discounting of other liabilities and represents the unwinding of the discount applied to the liability recognised in previous periods. This expense is generally presented as financing or interest expenses, although IAS 19 doesn’t specify where these should appear in financial statements.

Current service cost and attributing benefit to periods of service

General attribution criteria

The term ‘current service cost’ refers to the growth in the present value of the defined benefit obligation due to an employee’s service in the current period. This cost is generally recognised as an expense, except when it is considered part of the cost of another asset (IAS 19.120(a),121).

The criteria for attributing benefits to specific periods of service are detailed in paragraphs IAS 19.70-74. The general rule instructs entities to allocate benefits according to the plan’s benefit formula. However, if applying the benefit formula would disproportionately allocate a higher level of benefit to future years, a straight-line attribution should be used instead. In this approach, benefits are attributed from the point at which an employee’s service first entitles them to receive plan benefits—regardless of whether these benefits are conditional on future service—until the point where additional service will not materially increase those benefits, aside from potential salary increases. Refer also to this agenda decision.

Example: Attributing benefit to periods of service

Consider a company that offers a retirement benefit equivalent to a month’s salary for employees who have worked for at least five years. In this scenario, the benefits are attributed to the initial five years of employment. This is because serving additional years won’t increase the benefit amount, aside from adjustments due to salary increases.

Impact of vesting conditions

It’s important to note that an employee benefit obligation and its associated expense are recognised even if they are subject to vesting conditions. The likelihood that some employees may not meet these conditions is factored into the benefit measurement. For example, adjustments may be made based on the expected employee turnover rate (IAS 19.72).

Immediate vesting of benefits

Immediate vesting of benefits, wherein employees become eligible for specific benefits from their first day of employment without changes in value due to seniority (except for potential salary increases), presents several practical challenges. For instance, if an employee is entitled to receive an equivalent of three months’ salary upon leaving the company for any reason, traditional attribution of benefits to specific periods of service becomes problematic. This is because the benefit vests immediately and is not dependent on the duration of employment. Likewise, additional years of service do not lead to significant increases in the level of the benefit.

Some guidance can be gleaned from IAS 19.157, which discusses disability benefits. According to this paragraph, if the benefit level is consistent for any disabled employee regardless of years of service, the expected cost should be recognised when an event occurs that leads to long-term disability. Therefore, the most pragmatic approach for benefits that vest immediately is to recognise the obligation when the triggering event for payment occurs.

The exposure draft of IAS 19 also examined a similar issue concerning death-in-service benefits. The IASB proposed the following guidelines for recognising these benefits:

- When benefits are insured or re-insured with third parties, the cost should be recognised in the period when the related insurance premiums are due.

- For non-insured benefits, recognition occurs to the extent that deaths have taken place before the end of the reporting period.

- For death-in-service benefits provided through a post-employment benefit plan, their present value should be included in the post-employment benefit obligation.

- If the entity provides these benefits directly and not via a post-employment plan, this future commitment is not considered a present obligation and does not warrant liability recognition. A liability arises only if a death has occurred by the end of the reporting period.

This issue was also considered by the Interpretations Committee, but they were unable to agree on a conclusive wording for their agenda decision.

Given the complexities, the most straightforward recommendation is to recognise the liability relating to such immediate-vesting benefits when the event triggering the payment occurs. However, if these benefits can be integrated with other defined benefit plans, they should be accounted for concurrently. For example, in the case of death-in-service benefits, if an entity also offers a pension scheme, the estimated deaths during employment would reduce the value of the overall defined benefit obligation relating to pensions.

Actuarial assumptions

Definition and types of actuarial assumptions

Paragraphs IAS 19.75-98 outline actuarial assumptions as estimates of the variables used to calculate the ultimate cost of providing post-employment benefits. These assumptions are categorised into two main groups:

Demographic assumptions, including:

- Mortality rates (refer to IAS 19.81-82),

- Employee turnover rates, disability rates, and early retirement rates,

- The proportion of plan members eligible for benefits,

- Claim rates.

Financial assumptions, including:

- Discount rate,

- Benefit costs.

According to IAS 19.77-78, actuarial assumptions should be both unbiased, meaning neither imprudent nor excessively conservative, and mutually compatible.

Discount rate

The discount rate is determined by referring to the market yields on high-quality corporate bonds (HQCB) as of the end of the reporting period. In the absence of a deep market for HQCB in a particular currency, government bond yields should be utilised. The bonds’ currency and term should align with those of the post-employment benefit obligations. This alignment can be achieved through a single weighted average discount rate, which reflects the estimated timing and amount of benefit payments (IAS 19.83-86).

IAS 19 doesn’t explicitly define what constitutes HQCB. However, bonds issued by entities with the two highest investment ratings (AAA, AA) are generally considered as HQCB. Furthermore, this agenda decision confirmed that a pre-tax discount rate should be used.

Actuarial gains and losses

Actuarial gains or losses arise when actual outcomes differ from actuarial assumptions (‘experience adjustments’), or when actuarial assumptions themselves change (see IAS 19.128 for more examples). These gains or losses are different from past service cost or gains or losses on settlement (IAS 19.129).

Actuarial gains or losses impact the value of the defined benefit obligation recognised in previous periods. For post-employment benefits, actuarial gains and losses are recognised in OCI (IAS 19.120(c)), and for other long-term benefits, they are included in P/L (IAS 19.156). Note that these actuarial gains or losses are never recycled back into P/L, even if the benefit plan is amended or curtailed (IAS 19.122).

Past service cost

Past service cost refers to changes in the present value of the defined benefit obligation resulting from either a plan amendment or a curtailment. A curtailment significantly reduces the number of employees covered by the plan, whereas a plan amendment alters the value of benefits payable or introduces/withdraws a plan (IAS 19.102-105).

Past service cost is always recognised in P/L. Under certain conditions, it can be a credit to the P/L, for instance, when an entity reduces the value of benefits payable (IAS 19.106). This recognition happens at the earlier of two dates: when the plan amendment or curtailment occurs, or when the entity recognises related restructuring costs as per IAS 37 (IAS 19.103).

Past service cost excludes the effect of actuarial gains or losses (see IAS 19.108 for examples).

Gains and losses on settlement

A settlement takes place when an entity undertakes a transaction that eliminates all further legal or constructive obligations for part or all benefits provided under a defined benefit plan, such as making a lump sum cash payment to employees (IAS 19.111). Any gain or loss on settlement—calculated as the difference between the present value of the defined benefit obligation being settled and the settlement price—is immediately recognised in P/L (IAS 19.109).

The extract below discusses a settlement of a pension scheme by Smiths Group plc:

It’s worth noting that entities are not required to distinguish between past service cost due to a plan amendment, past service cost due to a curtailment, and gains or losses on settlement if these transactions happen concurrently (IAS 19.100).

Plan assets

Plan assets refer to financial resources managed by a legally separate entity (often referred to as a ‘fund’) whose sole purpose is to pay or fund employee benefits. These assets are earmarked specifically for employee benefits and cannot be used for other purposes. A qualifying insurance policy may also be considered a plan asset, as stated in IAS 19.115. For a comprehensive set of definitions, refer to IAS 19.8.

If assets meet the criteria laid out in IAS 19, their fair value is deducted from the present value of the defined benefit obligation in the statement of financial position. For further discussion on this, refer to IAS 19.113-119. Any changes in the fair value of plan assets, including the costs associated with managing these assets, are treated in a manner similar to actuarial gains or losses. Specifically, they are included in OCI for post-employment benefits and in P/L for other long-term benefits.

Typically, if plan assets are present, entities include a line in their financial statements referred to as ‘remeasurements of the net defined benefit liability (asset)’. This line consolidates both actuarial gains or losses and changes in the fair value of plan assets.

The discount expense associated with the defined benefit obligation is offset by interest income earned on the plan assets. The same discount rate used for calculating the obligation is applied to determine this interest income, which is based on the fair value of the plan assets.

Disclosure

IAS 19 mandates that entities disclose various aspects of defined benefit plans, including their characteristics and associated risks. The standard also stipulates specific requirements for disclosing any estimation uncertainties. For a comprehensive list of disclosure requirements related to defined benefit plans, consult paragraphs IAS 19.135-152.

Termination benefits

Definition of termination benefits

Termination benefits, as outlined in IAS 19.159-171, form a unique category of employee benefits that arise upon the termination of employment, rather than accruing during an employee’s ongoing service. However, it’s crucial to note that not all payments made at the end of employment qualify as termination benefits. According to IAS 19, termination benefits are specific to situations where:

- The entity decides to end an employee’s employment before the standard retirement age; or

- The employee chooses to accept a benefits package in return for voluntarily leaving the company.

In contrast, if a benefit is due to an employee upon ending their employment, regardless of the reason or manner of termination, it falls under the category of post-employment benefits, not termination benefits. Additionally, benefits aren’t considered termination benefits if they result from an employee’s unilateral decision to leave without an offer from the employer.

The line between termination benefits and post-employment benefits can sometimes blur. This is because many benefits granted at termination may legally be described as ‘termination benefits’. However, IAS 19 classifies them based on specific criteria, as discussed above.

Recognition and measurement

Entities should recognise termination benefits at the earliest of the following dates, according to IAS 19.165:

- When the entity can no longer withdraw the offer of those benefits (refer to IAS 19.166-167 for more details);

- When the entity recognises costs for a restructuring that is within the scope of IAS 37 and involves the payment of termination benefits.

Typically, measuring termination benefits is straightforward since they are often paid as a lump sum. Since these benefits are not for the future service of an employee, they should be recognised immediately in P/L, even if the actual payments are spread over time. In complex scenarios, such as when the termination benefit resembles a pension plan, an actuarial valuation may be required.

On occasion, the termination benefit might be the difference between what an employee would have received upon leaving without a formal offer and a higher amount offered because the entity initiated the termination (IAS 19.160). An example is provided in IAS 19.170.

Disclosure

IAS 19 does not prescribe any specific disclosure requirements in relation to termination benefits, as indicated in IAS 19.171.