IAS 23.8 prescribes that borrowing costs directly attributable to the acquisition, construction, or production of a qualifying asset must be capitalised as part of the cost of that asset, with a few exceptions. These borrowing costs can arise from both specific and general borrowings.

The previous version of IAS 23, in effect until 2009, permitted two methods for accounting for borrowing costs related to qualifying assets: the costs could either be capitalised or instantly recognised as an expense. However, entities are now prohibited from expensing these borrowing costs immediately in profit or loss. They must be capitalised when they meet the criteria of IAS 23 and expensed otherwise.

Let’s dive in.

Borrowing costs eligible for capitalisation

Borrowing costs in the scope of IAS 23 comprise interest and other costs incurred by an entity in relation to the borrowing of funds (IAS 23.5). IAS 23 lists examples of borrowing costs, including:

- Interest expense calculated using the effective interest method under IFRS 9,

- Interest in respect of lease liabilities recognised under IFRS 16,

- Exchange differences arising from foreign currency borrowings to the extent that they are regarded as adjustments to interest costs (IAS 23.6).

These examples are not exhaustive, and other borrowing costs can also be capitalised, provided they are connected to the borrowing of funds and would have been avoided had the expenditure on the qualifying asset not occurred (i.e., are directly attributable) (IAS 23.10). However, the actual or imputed cost of equity instruments is excluded from the scope of IAS 23 (IAS 23.3).

Finance costs associated with the unwinding of discount for liabilities which fall outside the scope of IFRS 9 are generally not eligible for capitalisation as they are not connected with borrowing of funds. This includes the unwinding of discount on, for example, employee benefits (IAS 19) or provisions (IAS 37).

--Too many IFRS updates? I know the feeling! That's why I created Reporting Period. It's a concise monthly summary of IFRS developments and Big 4 insights for accounting professionals. It's completely free, with zero spam, and you can unsubscribe anytime with one click. Interested? Leave your email below:

Specific borrowings

When funds are borrowed specifically for obtaining a qualifying asset, the borrowing costs eligible for capitalisation are the actual costs incurred on that borrowing during the period (IAS 23.12).

General borrowings

Entities often use general borrowings, making it challenging to establish a direct relationship between borrowings and a qualifying asset and to determine the borrowings that could have been avoided (IAS 23.11). Despite this, entities must determine a capitalisation rate to apply to expenditures on a qualifying asset (IAS 23.14). The average carrying amount of the asset during a period, inclusive of previously capitalised borrowing costs, is usually a reasonable approximation of the expenditures to which the capitalisation rate is applied in that period (IAS 23.18). Moreover, the IFRS Interpretations Committee clarified that expenditures on a qualifying asset incurred before obtaining general borrowings should be included when determining the expenditures to which the capitalisation rate is applied.

The capitalisation rate represents the weighted average of the borrowing costs applicable to the entity’s outstanding borrowings during the period, excluding specific borrowings. The borrowing costs capitalised by an entity during a period should not exceed actual costs incurred in that period.

Example: Capitalisation rate

On 1 March 20X1, Entity A commenced construction of a property, incurring the following expenditures during the year 20X1:

- 1 March 20X1: $100,000

- 1 June 20X1: $300,000

- 1 October 20X1: $600,000

Entity A had $500,000 of general borrowings on 1 January 20X1, which increased by $1 million to a total of $1.5 million on 1 July 20X1. The interest expense on these borrowings, calculated under IFRS 9, amounted to $50,000 for the full year 20X1.

The capitalisation rate was 5%, determined as: $50,000 / ($500,000 x 0.5 years + $1,500,000 x 0.5 years).

Consequently, Entity A capitalised $20,417 of borrowing costs, calculated as: ($100,000 x 10/12 + $300,000 x 7/12 + $600,000 x 3/12) x 5%.

Investment income

IAS 23.13 stipulates that any investment income generated from the temporary investment of specific borrowings must be subtracted from the borrowing costs eligible for capitalisation. Although IAS 23 doesn’t address investment losses, incorporating such losses would contradict the general definitions of borrowing costs.

For general borrowings, unlike specific ones, IAS 23 doesn’t detail how investment income affects the capitalisation rate. Consequently, entities must establish their accounting policy in instances where investment income is significant. Typically, investment income is ignored when determining the capitalisation rate for general borrowings.

Foreign exchange differences and hedging derivatives

IAS 23.6(e) outlines that borrowing costs can encompass exchange differences arising on foreign currency borrowings, provided they are considered adjustments to interest costs. Regrettably, IAS 23 offers no further guidance. One of the IFRS Interpretations Committee’s agenda decision touches on this matter, concluding that entities must establish their own accounting policy, often necessitating judgement, as indicated in IAS 23.11.

It’s common for exchange differences from foreign currency borrowings to be integrated into eligible borrowing costs. However, caution is essential in determining to what extent these differences constitute adjustments to interest costs, considering other potential causes of exchange differences. This is because IAS 21 mandates immediate recognition of exchange differences on monetary items in profit or loss. Consequently, entities with significant exchange differences from foreign currency borrowings should disclose the applied accounting policy.

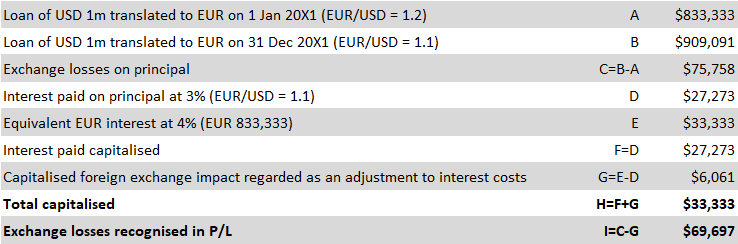

Entity A, with EUR as its functional currency, borrows USD 1 million on 1 January 20X1, to be repaid on 31 December 20X1, with a fixed interest rate of 3%. The EUR/USD rate is 1.2 on 1 January 20X1 (i.e., 1 EUR = 1.2 USD) and 1.1 on 31 December 20X1. An equivalent loan in EUR would have an interest of 4%. Entity A calculates the eligible exchange differences for capitalisation as presented below, with calculations available for download in an Excel file.

An entity might use derivatives, like interest rate swaps, to hedge against foreign currency risks. The accounting policies for such entities should clarify whether borrowing costs encompass the payments and accruals of interest under the swap, and any changes in the swap’s fair value. Payments and accruals of interest linked to such derivatives are generally considered part of the capitalised borrowing costs, assuming they hedge eligible borrowings. This holds true regardless of whether these derivatives are designated as hedging instruments under IFRS 9. On the other hand, changes in fair value are typically not capitalised, primarily because they reflect the present value of expected future cash flows, which doesn’t match the IAS 23 definition of borrowing costs.

Qualifying asset

Definition

A qualifying asset, as per IAS 23.5, requires a substantial period to be ready for intended use or sale. Examples of such assets include inventories, PP&E, intangible assets, investment properties, and bearer plants (IAS 23.7). The term ‘substantial period of time’ lacks a concrete definition in IFRS, hence entities exercise judgement and establish their own accounting policies under IAS 8.10-12. However, periods exceeding 12 months are commonly considered substantial.

IAS 23.18 clarifies that only expenditures resulting in cash payments, transfers of other assets, or the assumption of interest-bearing liabilities are expenditures on a qualifying asset. Consequently, borrowing costs concerning assets against which only trade payables have been incurred cannot be capitalised, unless these are interest-bearing. Capitalisation can commence once the payment is made, although typically the time difference between assuming a trade payable and the actual payment is insignificant.

Asset constructed by a third party

Assets constructed by a third party can also qualify, provided they meet the general IAS 23 criteria. Borrowing costs related to upfront payments for such assets can be capitalised, although IAS 23 does not specifically address this scenario.

Scope exemptions for certain qualifying assets

IAS 23.4 specifies that the application of IAS 23 isn’t mandatory for:

- Qualifying assets measured at fair value.

- Inventories manufactured or produced in large quantities on a repetitive basis, even if they require a substantial period to be ready for sale.

While IAS 23 isn’t obligatory for qualifying assets measured at fair value, it doesn’t restrict entities from presenting items in profit or loss as though borrowing costs had been capitalised prior to fair value measurement (IAS 23.BC4). An example of such an asset is a biological asset under IAS 41.

Concerning inventories manufactured in large quantities on a repetitive basis, the IASB recognises the difficulty in allocating and tracking borrowing costs (IAS 23.BC6). Capitalising these costs is optional, provided other IAS 23 criteria are satisfied. This exemption applies to items like maturing food produced in bulk repetitively. However, for specific, custom-made inventories meeting the qualifying criteria, the capitalisation of borrowing costs is obligatory.

Recognition of borrowing costs

Recognition principle

Borrowing costs directly attributable to acquiring, constructing, or producing a qualifying asset should be capitalised as part of the asset’s cost. Conversely, all other borrowing costs are recognised in profit or loss as incurred (IAS 23.8). Furthermore, borrowing costs are only capitalised when it is probable they will result in future economic benefits to the entity and can be measured reliably (IAS 23.9).

Commencement of capitalisation

An entity should start capitalising borrowing costs from the commencement date. This is the date when the entity simultaneously meets three conditions (IAS 23.17):

- It has incurred expenditures for the asset.

- It has incurred borrowing costs.

- It is undertaking necessary activities to prepare the asset for its intended use or sale.

These preparatory activities are interpreted broadly, encompassing not only physical construction but also preceding technical and administrative work, such as obtaining permits. However, if an asset, like land, is acquired for development but no associated activities have begun, borrowing costs are expensed in profit or loss as incurred (IAS 23.19).

Suspension of capitalisation

Capitalisation should be suspended during extended periods when active development of a qualifying asset stops (IAS 23.20). This occurs, for example, when the entity redirects its workforce and efforts towards another asset. However, capitalisation is not suspended when (IAS 23.21):

- Physical construction is temporarily stopped while substantial technical and administrative work continues; or

- Delays are an intrinsic part of preparing an asset for its intended use or sale, such as high water levels during bridge construction.

End of capitalisation

The capitalisation of borrowing costs ceases once substantially all the activities needed to prepare the qualifying asset for its intended use or sale are completed. Non-substantial activities include routine administrative work at a project’s end and minor pending modifications (IAS 23.22-23).

If a qualifying asset is constructed in parts, with each part capable of being used while construction continues on others, the entity stops capitalising borrowing costs for each completed part. IAS 23 illustrates that a business park with multiple buildings, where each building can be used individually while construction continues on other parts, is an example of a qualifying asset for which each part is capable of being usable while construction continues on other parts. Conversely, an industrial plant requiring completion of all parts before any can be used, such as a steel mill where several processes are carried out sequentially within the same site, is an example of a qualifying asset that needs to be complete before any part can be used (IAS 23.24-25).

Example: Borrowing costs on land

The IFRS Interpretations Committee addressed a query regarding the cessation of capitalising borrowing costs on land. The scenario presented involved an entity acquiring and developing land, subsequently constructing a building on that land, with both the land and the building classified as qualifying assets. The entity utilised general borrowings to finance both the land and building expenditures. The query specifically inquired whether the capitalisation of borrowing costs for land expenditures should cease upon the commencement of building construction or continue throughout the construction phase.

The Committee determined that the entity must consider the land’s intended use, which may be for owner-occupation, rental or capital appreciation, or sale, and not merely for the building’s construction. Furthermore, according to IAS 23.24, if the land cannot be used for its intended purpose during the building’s construction, the entity should evaluate the land and building together to determine when to cease capitalising borrowing costs. This means the land would not be ready for its intended use or sale until the completion of all activities necessary for both the land and the building.

Grants

Expenditures on an asset, which are subject to a capitalisation rate, should be reduced by any received progress payments and grants related to the asset (IAS 23.18).

Disclosure

Entities must disclose (IAS 23.26):

- The amount of borrowing costs capitalised during the period;

- The capitalisation rate used to determine the borrowing costs eligible for capitalisation.