Cost of sales is a functional line item within operating expenses classified by function. IFRS 18.82(a) requires an entity that presents at least one line item comprising expenses classified by function in the operating category to present a separate line item for cost of sales, unless the entity does not identify a cost of sales function.

A cost of sales function is most likely to be identifiable when gross profit is a useful measure of performance. Evidence will often include internal reporting of gross profit or gross margin, monitoring by management of the cost of goods or services sold, and a practice within the industry of presenting cost of sales. Cost of sales and gross profit are commonly presented by retailers, wholesalers, manufacturers, real estate developers and some service or technology businesses.

--Too many IFRS updates? I know the feeling! That's why I created Reporting Period. It's a concise monthly summary of IFRS developments and Big 4 insights for accounting professionals. It's completely free, with zero spam, and you can unsubscribe anytime with one click. Interested? Leave your email below:

During the development of IFRS 18, many stakeholders asked the IASB to define cost of sales because of diversity in the scope of costs included in that line item. The IASB acknowledged those concerns but concluded that developing such a definition within a reasonable timeframe would be too difficult. Instead, IFRS 18.82(a) requires an entity that presents cost of sales to include in that line item the expense of inventories recognised under IAS 2.38. However, determining which additional expenses are included in cost of sales remains a matter of judgement. As a result, comparability between entities remains limited (IFRS 18.BC256-BC257).

IAS 2.38 states that the amount of inventories recognised as an expense during the period, often referred to as cost of sales, consists of costs previously included in the measurement of inventory that has now been sold, together with unallocated production overheads and abnormal amounts of production costs of inventories. Depending on the entity’s circumstances, other amounts may also be included, such as distribution costs. Write-downs of inventories to net realisable value are also commonly presented within cost of sales.

IFRS 18.82(b) requires an entity that presents a line item for cost of sales to disclose a qualitative description of the nature of expenses included in that line item.

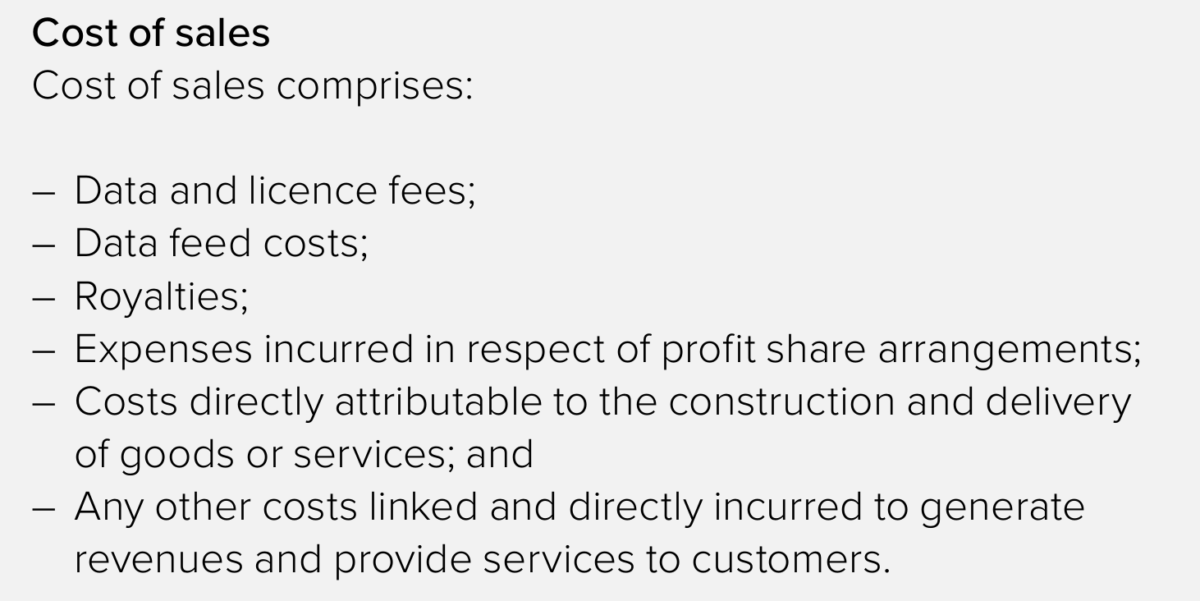

The following are a few examples of disclosures about cost of sales:

Unilever:

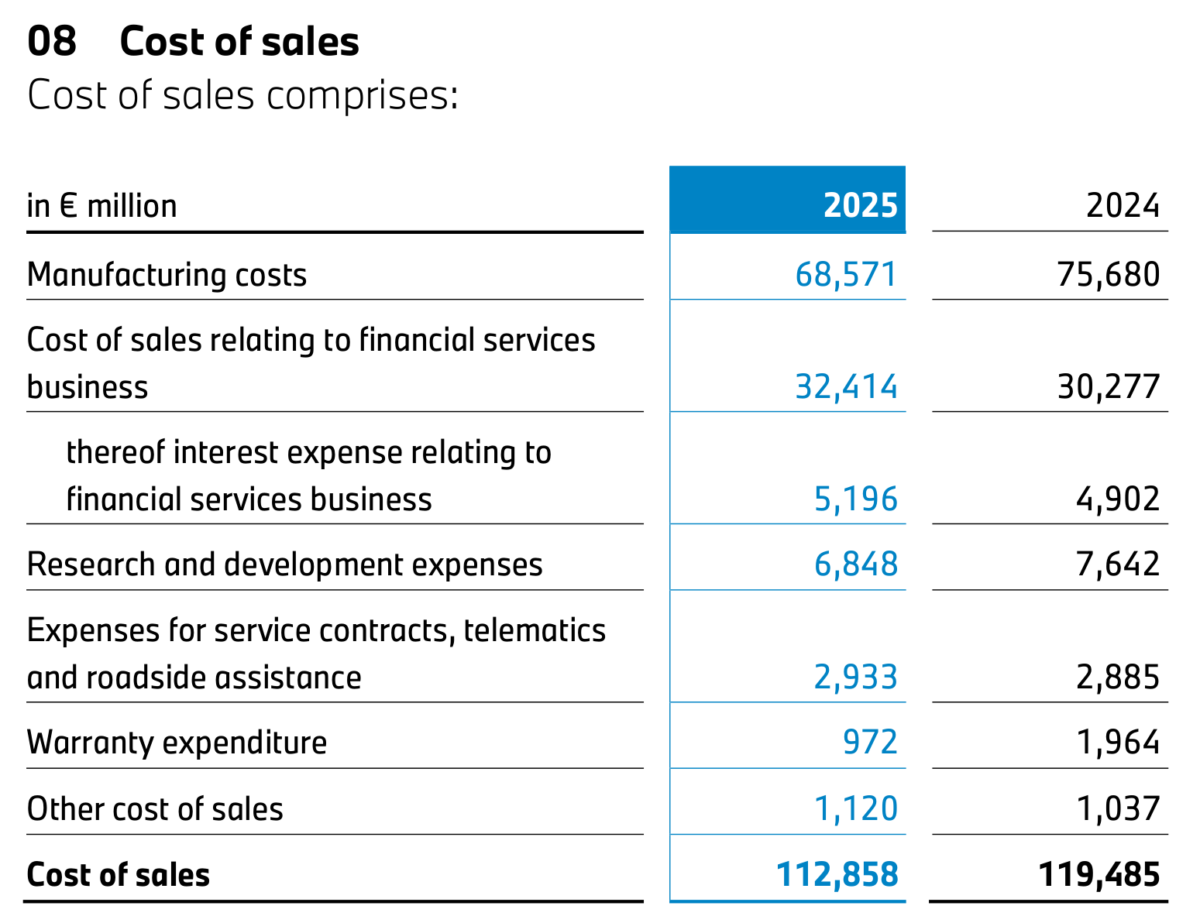

BMW:

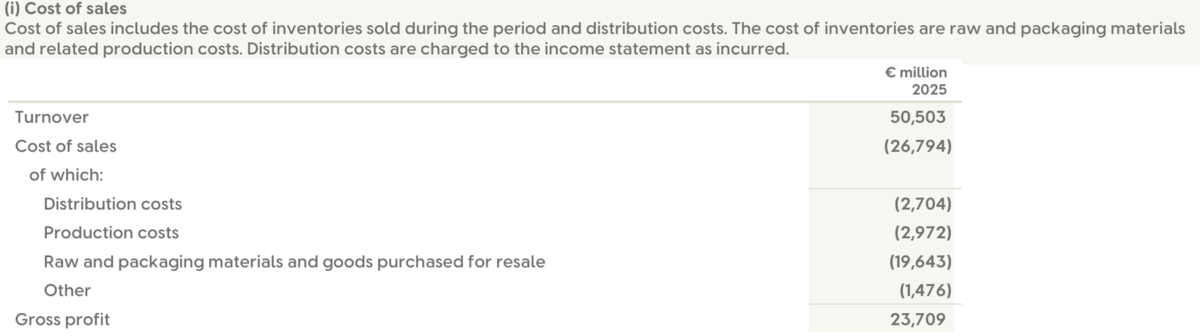

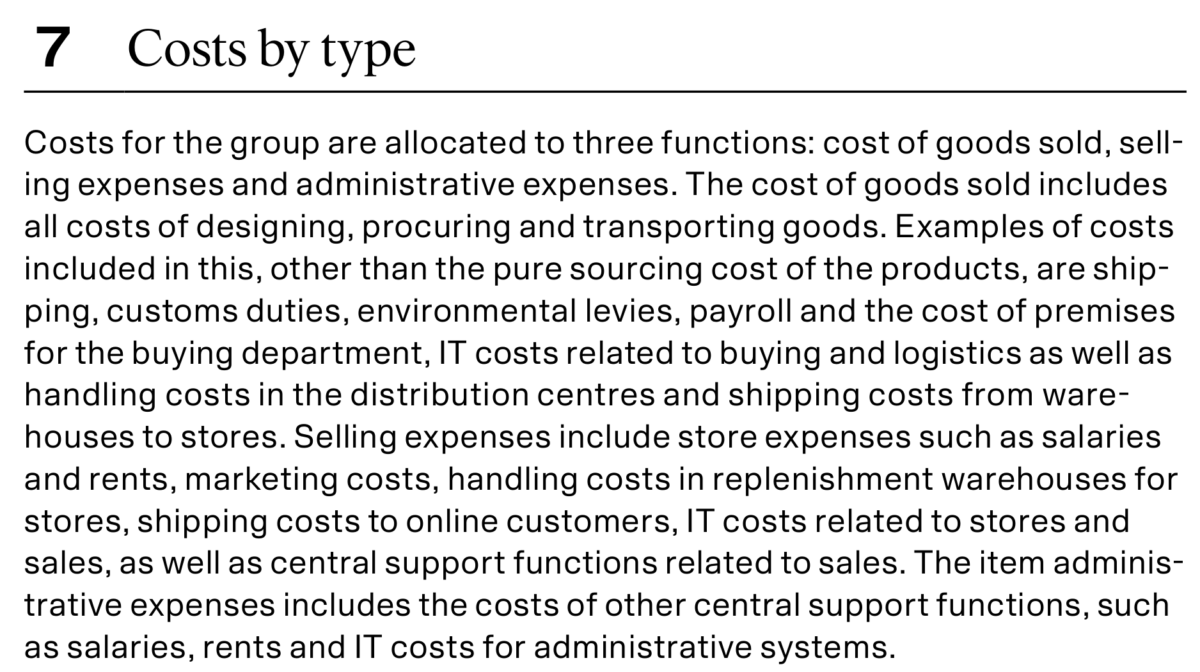

London Stock Exchange Group:

L’Oréal:

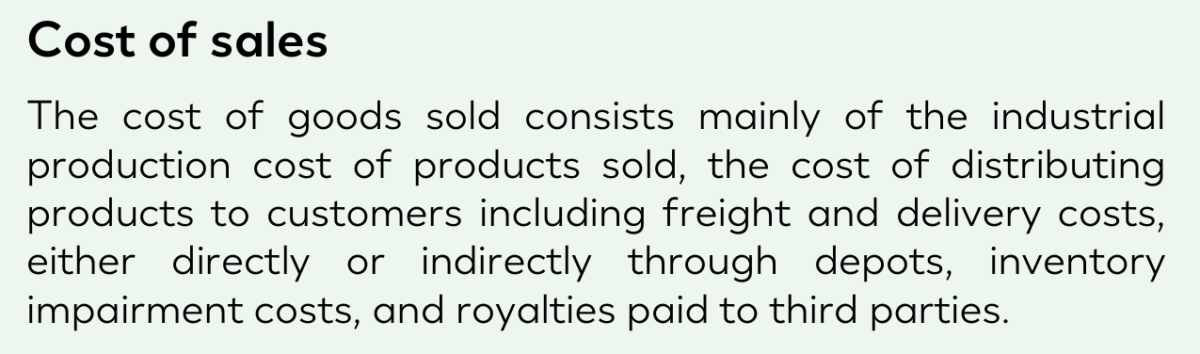

H&M Hennes & Mauritz:

Hermès International: