Entities often undertake transactions denominated in foreign currencies. These transactions must be translated into the currency that the company uses to present its financial statements. In addition, a parent company may conduct foreign operations through subsidiaries, associates or joint arrangements. In such cases, the financial statements of these investees need to be translated to the currency used in the consolidated financial statements. Furthermore, an entity may opt to present its financial statements in a currency different from the one used in its economic environment. All these considerations are addressed by IAS 21.

Let’s dive in.

Translating foreign currency transactions

Initial recognition

Initially, a foreign currency transaction is recognised at the spot exchange rate (i.e., the rate for immediate delivery) between the functional currency and the foreign currency at the date of the transaction (IAS 21.21). A foreign currency transaction is a transaction denominated or requiring settlement in a foreign currency, including transactions arising when an entity (IAS 21.20):

- Buys or sells goods or services priced in a foreign currency,

- Borrows or lends funds with amounts payable or receivable denominated in a foreign currency, or

- Otherwise acquires or disposes of assets, or incurs or settles liabilities, denominated in a foreign currency.

The transaction date is when the transaction first qualifies for recognition under applicable IFRS standard (IAS 21.22).

IAS 21 permits the use of simplifications in determining the foreign exchange rate, such as using an average rate, as long as exchange rates don’t fluctuate significantly (IAS 21.22). In practice, entities often use the average of monthly rates, as central banks publish these for most currencies.

--Too many IFRS updates? I know the feeling! That's why I created Reporting Period. It's a concise monthly summary of IFRS developments and Big 4 insights for accounting professionals. It's completely free, with zero spam, and you can unsubscribe anytime with one click. Interested? Leave your email below:

Translation at reporting dates

At the end of each reporting period (IAS 21.23):

- Foreign currency monetary items are translated using the closing rate (i.e., the spot exchange rate at the end of the reporting period).

- Non-monetary items that are measured in terms of historical cost in a foreign currency are translated using the exchange rate at the date of the transaction. They are not re-translated using the closing rate.

- Non-monetary items measured at fair value in a foreign currency are translated using the exchange rates at the date when the fair value was determined.

Specific procedures for translating foreign operations are discussed below.

Monetary and non-monetary items

Monetary items are defined as units of currency held and assets and liabilities to be received or paid in a fixed or determinable number of units of currency (IAS 21.8). Common examples of monetary items include trade receivables and payables or loans. Other examples are given in paragraph IAS 21.16.

Non-monetary items lack the right to receive (or the obligation to deliver) a fixed or determinable number of units of currency. Examples of non-monetary items include advance consideration paid or received, goodwill, items of PP&E, intangible assets and inventories (IAS 21.16).

Investments in equity instruments are also non-monetary items (IFRS 9.B5.7.3), but they are measured at fair value and therefore their carrying amount is effectively impacted by foreign exchange movements.

Recognition of exchange differences

As a general rule, exchange differences arising from the settlement or translation of a monetary asset are recognised in P/L (IAS 21.28).

When non-monetary assets are measured at fair value (or revalued amount) in a foreign currency, exchange differences are treated similarly to gains or losses on remeasurement. That is, they can be recognised in OCI under circumstances specified by other IFRS standards (IAS 21.30-31).

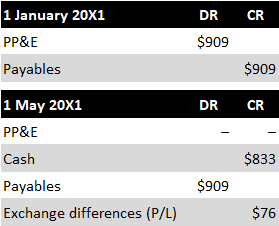

Suppose Entity A buys an item of PP&E on 1 January 20X1. Entity A’s functional and presentation currency is the Euro (EUR), but the invoice for the PP&E is for 1,000 US dollars (USD). The EUR/USD exchange rate on 1 January 20X1 is 1.1 (i.e., 1 EUR = 1.1 USD). The invoice is paid on 1 May 20X1 when the EUR/USD rate is 1.2. All calculations used in this example are available for download in an Excel file.

Entity A would make the following entries in EUR:

As shown, the PP&E item is carried at historical cost and is not subsequently retranslated to reflect exchange rate movements between initial recognition and invoice payment.

Use of multiple exchange rates

When several exchange rates are available, the rate used is the one at which the future cash flows represented by the transaction or balance could have been settled if those cash flows had occurred at the measurement date (IAS 21.26).

Lack of exchangeability

In 2023, the IASB issued amendments to IAS 21 that will require companies to provide more information in their financial statements when a currency cannot be exchanged into another currency, an issue that wasn’t previously covered. The amendments are effective for annual reporting periods beginning from 1 January 2025, with early application permitted. Read more in EY’s publication.

Advance Consideration (IFRIC 22)

IFRIC Interpretation 22 ‘Foreign Currency Transactions and Advance Consideration’ stipulates that the transaction date for determining the exchange rate used for initial recognition of the related asset, expense, or income is the date an entity first recognises the non-monetary asset or non-monetary liability arising from the payment or receipt of advance consideration (IFRIC 22.8-9).

Exchange differences on borrowings

According to paragraph IAS 23.6(e), borrowing costs may include exchange differences resulting from foreign currency borrowings to the extent that they are regarded as an adjustment to interest costs.

Exchange differences on deferred tax

Exchange differences on deferred foreign tax liabilities or assets may be classified as deferred tax expense or income if that presentation is considered to be the most useful to financial statement users (IAS 12.78).

Change in functional currency

A change in functional currency can only occur if there are changes to the underlying transactions, events, and conditions that the functional currency reflects. Any change in functional currency is accounted for prospectively (IAS 21.35-37).

Translating a foreign operation

When an entity within a group uses a different presentation currency from that of the consolidated financial statements, translations are performed using the following procedures as per IAS 21.39:

- Assets, including goodwill and fair value adjustments (IAS 21.47), and liabilities, are translated at the closing rate at the reporting date. This includes comparatives translated using historical rates.

- Income and expenses are translated at exchange rates applicable at the transaction dates. This also includes comparatives translated using historical rates.

- All resulting exchange differences are recognised in OCI.

IAS 21.40 allows for simplifications in determining the foreign exchange rate, for example, using an average rate, assuming exchange rates do not significantly fluctuate. In practice, an average rate for each month is most commonly used.

Cumulative translation adjustment (CTA)

Exchange differences referred to in IAS 21.39(c) are commonly identified as either ‘Cumulative Translation Adjustment’ (CTA) or ‘Foreign Currency Translation Reserve’ (FCTR). The two primary sources for CTA, as per IAS 21.41, include:

- Translating income and expenses at the transaction date exchange rates, while assets and liabilities are translated at the closing rate.

- Translating opening assets and liabilities at a closing rate that differs from the opening rate.

CTA is recognised in OCI, presented as a distinct item within equity, and not recycled to P/L until the foreign operation is disposed of. CTA is further divided between controlling and non-controlling interests (IAS 21.41). It is also recognised in OCI for investments accounted for using the equity method (IAS 21.44).

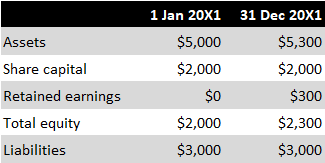

Consider Group A with the Euro as its presentation currency. Entity X, one of Group A’s subsidiaries, uses the US Dollar as its presentation currency. The following EUR/USD exchange rates apply:

- Opening rate at 1 January 20X1: 1.1

- Average rate in 20X1: 1.2

- Closing rate at 31 December 20X1: 1.3

All calculations and tables presented in this example can be downloaded in an Excel file.

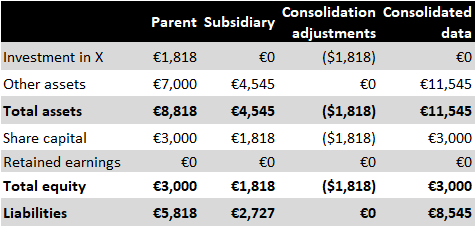

Entity X is consolidated to Group A consolidated financial statements as follows:

Entity X stand-alone data

Statement of financial position in USD:

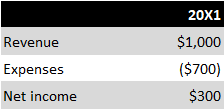

P/L in USD:

Consolidation of Group A

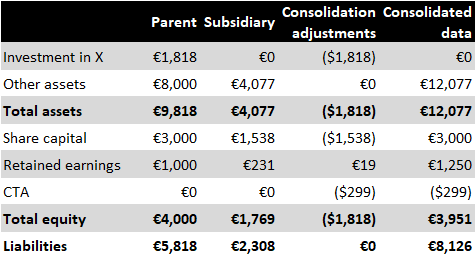

Consolidated statement of financial position in EUR at 1 January 20X1:

Consolidated statement of financial position in EUR at 31 December 20X1:

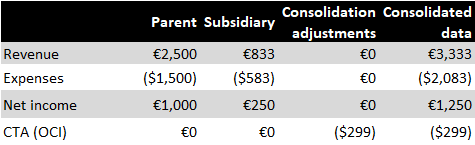

Consolidated P/L for 20X1 in EUR:

Intragroup balances

Exchange differences on intragroup balances

Although intragroup balances are eliminated during consolidation, any exchange differences arising from those balances are not. This is because the group is effectively exposed to foreign exchange gains and losses, even on intragroup transactions, including dividend receivables and payables (IAS 21.45).

Goodwill considerations

Goodwill, as previously stated, is considered an asset of a foreign operation and is retranslated at each reporting date. For multinational group acquisitions, goodwill should be allocated to each functional currency level of the acquired foreign operation (IAS 21.BC32).

Net investment in a foreign operation

A net investment in a foreign operation represents the reporting entity’s interest in the net assets of that operation (IAS 21.8). Monetary items receivable from, or payable to, a foreign operation, where settlement is neither planned nor likely to occur in the foreseeable future, are treated as part of the entity’s net investment in that operation (IAS 21.15-15A). Exchange differences arising from such monetary items are recognised in P/L in separate financial statements, but in OCI (as part of CTA) in consolidated financial statements (IAS 21.32-33).

Disposal or partial disposal of a foreign operation

On disposing of a foreign operation, the cumulative amount of exchange differences relating to that operation, recognised in OCI and accumulated in the separate component of equity (i.e. CTA), is reclassified from equity to P/L (as a reclassification adjustment) when the gain or loss on disposal is recognised (IAS 21.48). Furthermore, paragraph IAS 21.48A outlines accounting procedures for partial disposals.

Translation from the currency of a hyperinflationary economy

IAS 21.42-43 provides specific provisions for translating from the currency of a hyperinflationary economy.

Functional and foreign currencies

Defining functional and foreign currencies

The functional currency of an entity is determined by the primary economic environment in which it operates, primarily focusing on the currency that significantly influences its revenue generation and expense management. This typically includes the currency in which sales prices for goods and services are denominated and settled, as well as the currency that dictates costs related to labour, materials, and other expenses. Additional considerations include the currency used for financing activities, such as issuing debt or equity, and the currency in which operating receipts are usually retained (IAS 21.9-10).

The foreign currency is any currency that is different from the entity’s functional currency (IAS 21.8).

Functional currency of a foreign operation

Identifying the functional currency can be particularly complex when a reporting entity is a foreign operation of another entity and fundamentally an extension of its operations. For instance, a ‘financial’ subsidiary (i.e., a subsidiary primarily holding financial assets or issuing debt) whose core financial assets and liabilities are denominated in the parent’s functional currency may have the same functional currency as the parent, regardless of its operational country. IAS 21.11 outlines additional factors to be considered when determining the functional currency of a foreign operation. If these indicators are mixed, priority is given to the primary indicators described in IAS 21.9.

Use of a presentation currency other than the functional currency

The rules regarding the translation of a foreign operation are equally applicable to the use of a presentation currency that is different from the functional currency.

Presentation in financial statements

IAS 21 does not specify in which part of the income statement foreign exchange differences should be presented. Therefore, entities must develop an accounting policy. The most common approach is to report exchange differences in the same section of the income statement where the original income or expense was (or will be) recognised for the item that subsequently led to exchange differences. For example, exchange differences on trade receivables are presented within operating profit, while exchange differences on debt are presented within finance costs. This method aligns with the one mandated by IFRS 18.

Cash flows in foreign currency

IAS 21 does not cover the statement of cash flows as it falls under the scope of IAS 7. This includes the presentation of cash flows resulting from transactions in a foreign currency and the translation of cash flows from a foreign operation (IAS 21.7).

Disclosure

The disclosure requirements are provided in IAS 21.51-57.