The statement of cash flows is a primary financial statement, mandated for presentation by all entities, irrespective of their business profile. It holds equal prominence with other primary financial statements (IAS 1.10-11).

Cash flow information is crucial for investors when evaluating an entity’s ability to generate cash and assessing its liquidity and solvency. The cash flow statement shows how the entity generates and uses cash in its operations and investing activities, as well as how it secures funds through borrowings and services its debt. It also provides insights into the entity’s cash dividends and other cash distributions to investors.

The statement of cash flows is governed by IAS 7, which mandates the classification of cash flows into operating, investing, and financing activities in a manner that is most appropriate to a reporting entity’s business (IAS 7.10-11).

Let’s dive in.

Cash and cash equivalents

Cash

Cash, as defined in IAS 7.6, comprises both cash on hand and demand deposits. However, IAS 7 does not provide explicit definitions for either of these terms. Typically, cash on hand is interpreted as physical currency, including notes and coins, issued by a central bank. Demand deposits, on the other hand, should possess liquidity comparable to cash, allowing for the withdrawal of funds at any time without incurring substantial penalties, such as the loss of a significant portion of accrued interest. Nonetheless, a deposit that does not qualify as cash may still satisfy the criteria to be considered a cash equivalent.

--Too many IFRS updates? I know the feeling! That's why I created Reporting Period. It's a concise monthly summary of IFRS developments and Big 4 insights for accounting professionals. It's completely free, with zero spam, and you can unsubscribe anytime with one click. Interested? Leave your email below:

Cash equivalents

Cash equivalents are investments that are (IAS 7.6-9):

- Held for meeting short-term cash commitments rather than for investment or other purposes,

- Highly liquid,

- Readily convertible to known amounts of cash, and

- Subject to an insignificant risk of changes in value.

Generally, as stipulated by IAS 7.7, an investment should have a maturity of no more than three months from the acquisition date to be considered short-term. Although IAS 7 does not strictly enforce this three-month period, it is commonly viewed as a valid benchmark. The classification assigned at initial recognition remains unchanged as the investment approaches its maturity date. A deposit exceeding a three-month maturity period may still qualify as a cash equivalent if it allows early withdrawal without penalty, such as a loss of interest, and its primary purpose is to meet short-term cash commitments rather than for investment or other purposes.

Example: Investment held for other purposes

A parent company grants its subsidiary a 45-day loan to help manage a temporary cash shortage. The resulting loan receivable is short-term, can be readily converted to known amounts of cash, and carries an insignificant risk of changes in value. However, this asset cannot be classified by the parent company as a cash equivalent. The reason is that it is not intended to meet the parent’s own short-term cash commitments, and thus, it does not meet the definition of a cash equivalent.

Debt instruments and money market funds

Certain debt instruments, including government and high-quality corporate bonds, can potentially meet the criteria for cash equivalents. However, investments in debt securities carrying significant credit risk are not classified as cash equivalents, due to the risk of default by the issuer.

Money market funds, also known as liquidity funds, are often utilised by companies in their cash management processes. Despite being equity instruments, they may be treated as cash equivalents if they fulfil the aforementioned criteria. This topic was discussed by the IFRS Interpretations Committee, which clarified that the amount receivable must be known at the time of the initial investment. Thus, units cannot be considered cash equivalents solely because they can be converted to cash at any time at the market price in an active market. Entities must also ensure that any investment is subject to an insignificant risk of changes in value to classify it as a cash equivalent. To mitigate credit risk, entities should opt for funds investing exclusively in highly rated debt instruments with a maximum maturity of three months and a diversified portfolio.

It is noteworthy that the classification of cash equivalents does not align with the classification of financial assets under IFRS 9. For instance, the inclusion of investments in money market funds in the ‘fair value through profit or loss’ category under IFRS 9 does not prohibit their classification as cash equivalents in the statement of cash flows.

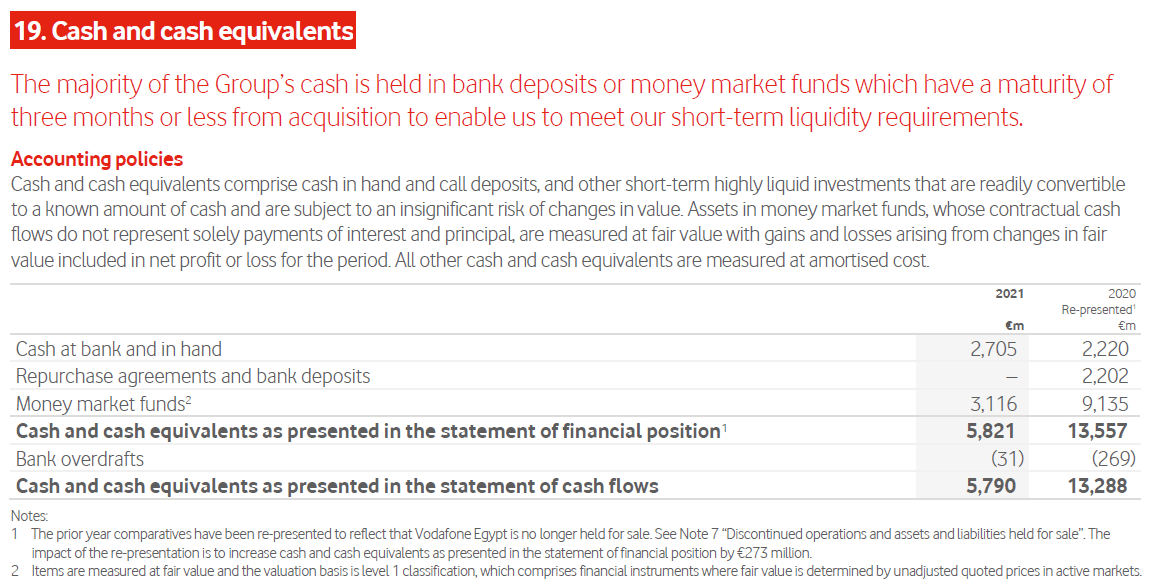

Vodafone provides a related disclosure in their financial statements:

Equity instruments

Equity investments are generally not included in cash equivalents, even when they are highly liquid. This exclusion is due to two main reasons: firstly, the amount of cash to which they can be converted is uncertain at the time of initial investment; secondly, they typically bear a significant risk of changes in value.

However, an exception is mentioned in IAS 7.7, citing the example of preference shares acquired shortly before their maturity and with a specified redemption date. These can be considered as cash equivalents if they are readily convertible into cash, carry no significant risk of changes in value, and are not held for investment purposes.

Intragroup cash pooling arrangements

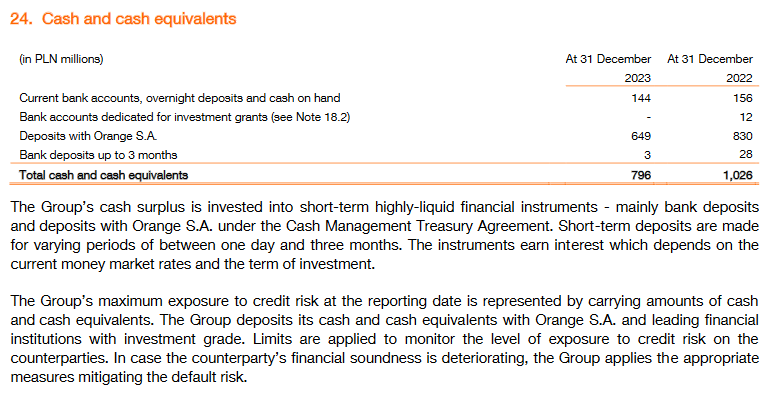

Some groups utilise central pooling for all cash and cash equivalents, effectively resulting in subsidiaries depositing cash with a parent company or another group entity. These balances must be assessed against IAS 7 criteria, but it is entirely plausible to classify them as cash equivalents. Considerations include the terms and conditions of the intragroup arrangement, the group’s credit rating, liquidity, and access to external financial resources. For instance, Orange’s Polish subsidiary classifies such funds as cash equivalents:

Bank borrowings

Bank borrowings are generally classified as financing activities. However, there exists an exception for bank overdrafts, which may be considered as part of cash and cash equivalents if they are repayable on demand and constitute an integral component of the company’s cash management. A notable characteristic of such arrangements is the frequent fluctuation of the bank balance between positive and overdrawn states (IAS 7.8).

The IFRS Interpretations Committee deliberated on the types of borrowings that could be included as cash and cash equivalents. They reviewed a scenario in which an entity utilised short-term loans and credit facilities with short contractual notice periods (e.g., 14 days) for purported cash management purposes. In this instance, the balance of the short-term arrangements did not regularly oscillate between negative and positive. After consideration, the Committee determined that such an arrangement did not meet the definition of cash and cash equivalents. The absence of an on-demand repayment feature and the lack of fluctuation in the balance were strong indicators that the setup was more akin to a financing arrangement than a cash management one.

Gold and cryptocurrencies

Gold and cryptocurrencies cannot be classified as cash equivalents as they are not readily convertible to known amounts of cash.

Reconciliation to the statement of financial position

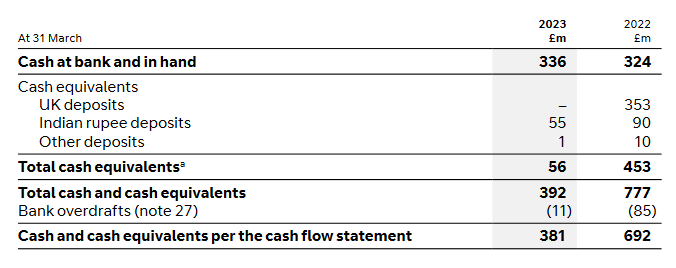

Cash and cash equivalents reported in the statement of cash flows may not always align with the corresponding line in the statement of financial position. Some entities present the cash balance in the statement of cash flows net of on-demand bank overdrafts, treating it as a liability in the statement of financial position. Another discrepancy can arise from cash and cash equivalents of a subsidiary classified as assets held for sale under IFRS 5. If such differences exist, IAS 7.45 mandates entities to provide a reconciliation between the amounts in these two statements, as illustrated in this extract from BT’s annual report:

Disclosure

Entities must disclose their policy for determining the composition of cash and cash equivalents and the components comprising the overall balance (IAS 7.45-46). If significant judgement is involved in classifying a particular asset as a cash equivalent, relevant disclosures should be made in accordance with IAS 1.122.

Restricted cash

Restricted cash refers to cash and cash equivalent balances that have usage constraints. IAS 7 provides an example of balances held by a subsidiary, which are not accessible by the group due to exchange controls or other legal restrictions. Such instances should be disclosed under IAS 7.48-49, as shown in this extract from Vodafone’s annual report:

While not explicitly required, disclosing other types of restrictions on cash and cash equivalents (e.g., government grant funds earmarked for specific expenditures) is common practice. Such restricted cash balances should be carefully examined against the definition of cash and cash equivalents as they might need to be reclassified as other assets if they do not meet the criteria.

The IFRS Interpretations Committee deliberated on scenarios where an entity can freely access a deposit but is contractually obligated to maintain a specified amount of cash for designated purposes. Breaching this obligation would result in contractual violations. The Committee concluded that such restrictions do not alter the classification of the deposit as cash, provided the entity can access the funds on demand.

Example: Restricted cash

Entity A secured an investment loan of $100 million from a bank, allocated to a dedicated account. To transfer funds from this account, Entity A must obtain bank approval, ensuring the expenditure aligns with the agreed-upon budget and schedule. In this scenario, it is unlikely that the $100 million will be classified as cash and cash equivalents since Entity A requires third-party (bank) approval for use. Ideally, the $100 million should be kept off-balance sheet. When actual transfers occur, Entity A should report inflows from financing activities.

Operating activities

Operating activities constitute the principal revenue-producing activities of an entity and serve as the default category for cash flows that do not align with the definitions of either investing or financing cash flows. Typically, cash flows resulting from transactions or events directly impacting profit or loss are presented under operating activities. However, a notable exception exists for the disposal of long-term assets (IAS 7.6,13-15). It’s noteworthy that a specific type of transaction could be classified as both an operating and investing activity, depending on the entity’s business model.

Examples of cash flows from operating activities include:

- Cash receipts from selling goods, rendering services, and other revenue streams.

- Cash payments to suppliers for goods and services and to, and on behalf of, employees.

- Cash payments in contracts held for dealing or trading purposes.

- Cash payments related to loans and deposits reported by financial institutions.

- Cash payments or refunds of income taxes, unless specifically associated with financing or investing activities.

- Cash payments in hedge contracts when the hedged item is classified as an operating activity.

Direct or indirect method

An entity must report cash flows from operating activities using one of the following methods (IAS 7.18):

- The direct method, which discloses major classes of gross cash receipts and gross cash payments; or

- The indirect method, which adjusts profit or loss for non-cash transactions, deferrals or accruals of past or future operating cash receipts or payments, and items of income or expense related to investing or financing cash flows.

Direct method

IAS 7 encourages entities to report cash flows from operating activities using the direct method. Under this method, data on major classes of gross cash receipts and gross cash payments can be derived in one of two ways (IAS 7.19):

- Directly from the entity’s financial software; or

- By adjusting sales, cost of sales, and other P/L items for working capital movements, non-cash charges, and items where the cash effects are related to investing or financing activities.

Entities using the second approach are not required to present a reconciliation showing the adjustments made between the income statement and the corresponding cash receipts or payments.

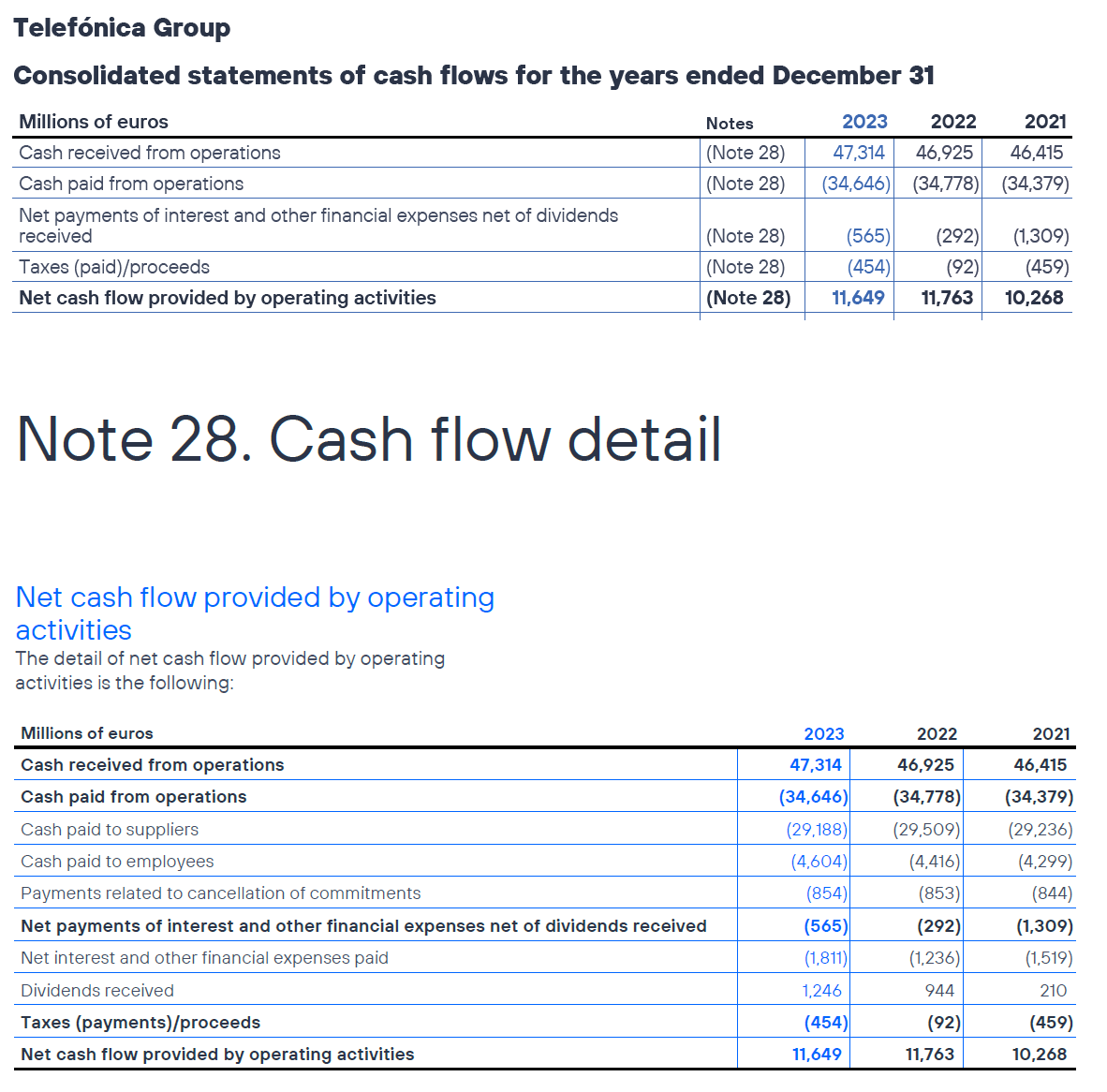

The direct method is most commonly used in the financial sector. However, a notable example of a non-financial company that reports its cash flows using the direct method is Telefonica SA:

Indirect method

Under the indirect method, net cash flow from operating activities is calculated by adjusting profit or loss for the following:

- Changes in working capital;

- Non-cash charges in profit or loss, such as depreciation; and

- Items where the cash effects relate to investing or financing activities.

IAS 7.20 stipulates the use of profit or loss as a starting point when reporting cash flows from operating activities using the indirect method. Nonetheless, several reporting entities use subtotals like operating profit, which don’t equate to ‘profit or loss’ as they exclude certain items of income and expense. However, the upcoming IFRS 18 will change the existing requirements so that entities will be required to use operating profit or loss as the starting point for the indirect method.

Investing activities

Investing activities involve acquiring and disposing of long-term assets and other investments not classified as cash equivalents. Such cash flows must lead to a recognised asset in the statement of financial position (IAS 7.6,16) – a crucial point to note. Items intrinsically related to investing activities that don’t result in a recognised asset are excluded. For instance, internal development expenditures are classified as operating activities if expensed and as investing activities if capitalised. Transaction costs for business combinations, which must be expensed under IFRS 3, are another relevant example of operating cash payments.

Examples of cash flows from investing activities include:

- Cash payments to acquire PP&E, intangibles, and other long-term assets.

- Cash payments related to internally generated assets.

- Cash receipts from selling long-term assets.

- Cash payments/receipts for acquiring/selling equity or debt instruments, excluding cash equivalents or instruments held for dealing/trading.

- Cash payments related to loans made to other parties by non-financial institutions.

- Cash payments in derivative contracts, except those for dealing/trading or classified as financing activities.

- Cash payments in hedge contracts when the hedged item is classified as an investing activity.

Financing activities

Financing activities result in changes in the size and composition of the entity’s contributed equity and borrowings (IAS 7.6,17). Examples of such activities encompass:

- Cash proceeds from issuing shares or other equity instruments.

- Cash payments to owners for acquiring or redeeming the entity’s own shares.

- Cash payments for acquiring non-controlling interest.

- Cash proceeds from, and repayments of, loans, bonds, and other borrowings.

- Repayments of lease liabilities.

Practical application issues: operating, investing, and financing activities

Interest and dividends

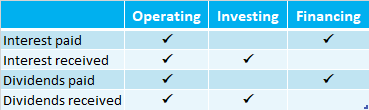

A dedicated section of IAS 7 (IAS 7.31-34) addresses interest and dividends, given the lack of consensus on their classification as operating, investing, or financing activities. The following table provides a summary of the categories they may be included in:

The inclusion of interest paid or received and dividends received within operating activities aligns with the rationale that these items impact the profit or loss of the entity. Including dividends paid in operating activities can depict the sustainability of such payments from these activities, although they are more commonly classified within financing activities. An alternative approach classifies these items according to their ‘nature’, with, for example, interest paid on debt classified within financing activities.

However, the upcoming IFRS 18 will change the existing requirements so that most entities would present interest and dividends paid within financing activities and interest and dividends received within investing activities.

In the case of zero-coupon and similar instruments, the payment at maturity should be divided between the interest and principal amount. Consider the following example:

Example: Interest on zero-coupon instruments in cash flow statement

Entity A, a manufacturing company, opts to present interest received under operating activities in the statement of cash flows. On 1 January 20X1, it purchases a 2-year zero-coupon government bond with a face value of $10 million for $9 million. In 20X1, a $9 million outflow is reported under investing activities. Although interest on the bond is accrued and presented as interest income in 20X1 and 20X2, no cash flow occurs concerning interest in these years. Upon redemption in 20X3, Entity A receives $10 million, divided between the repayment of originally invested funds ($9 million in investing activities) and interest earned ($1 million in operating activities).

Factoring of trade receivables

IAS 7 does not specifically address the factoring of trade receivables. The presentation in the statement of cash flows depends on whether the receivables subjected to factoring are derecognised. If so, this implies that they have, in substance, been paid, warranting a cash inflow from operating activities.

If not derecognised, factoring is essentially a borrowing, with the receivables treated as collateral, hence recognised as a financial liability and cash receipt in financing activities. The receipt of a customer payment results in the derecognition of a trade receivable with an inflow in operating activities and the effective repayment of a financial liability with a cash outflow in financing activities. This holds true even when the customer pays directly to the financial institution (the factor) as the payment is considered collected on behalf of the entity.

While it might be argued that the customer’s payment to the financial institution could be treated as a non-cash transaction, resulting in no reported cash flow by the entity, this approach is, in my opinion, the least preferable. This is because it would mean the entity never reports cash flow from its principal activities even after payment by the customer.

Supplier finance arrangements

Supplier finance arrangements present similar challenges in presentation as factoring of trade receivables. The pivotal question, once again, is whether the derecognition criteria set out in IFRS 9 have been satisfied. The discussion on the presentation in the cash flow statement is analogous to the one about trade receivables presented above.

Acquisition by assumption of long-term payables

In certain instances, an entity might acquire, for example, a piece of equipment on credit, with repayments distributed over several years. This raises the question: should such repayments be classified within investing or financing activities? IAS 7 does not provide a clear-cut answer to this query. Some propose that when payments are significantly deferred beyond the acquisition date, such a liability is tantamount to financing, with repayments presented within financing activities, akin to leases. Conversely, others posit that such liabilities do not qualify as borrowings unless they involve a counterparty typically engaged in financing. Drawing an analogy, situations may arise where an entity considerably extends credit to its customers (trade receivables with a significant financing component under IFRS 15), and classifying these receivables as loans for non-financial entities could be counter-intuitive.

In my opinion, both approaches hold merit. The critical aspect is making a well-informed decision. It’s noteworthy that US GAAP explicitly address this issue, stipulating that only payments to suppliers at or around the time of purchase can be presented in investing activities. Conversely, assuming directly related long-term payables to the seller constitutes a financing transaction, and subsequent repayments are classified as financing cash outflows (ASC Topic 230, 230-10-45-13 to 15).

Taxes

Income tax payments are typically classified as operating activities. However, IAS 7 mandates alternative classifications if they can be clearly associated with financing or investing activities (IAS 7.35-36). Nonetheless, classifications outside of operating activities are uncommon.

Notably, IAS 7 does not specify how to classify VAT payments, and there are two prevailing approaches in practice: these payments can either be consolidated with the receipt/payment of the associated receivable/payable, or presented separately.

Changes in ownership interests in subsidiaries and other businesses

IAS 7.39-42B include certain disclosure and classification requirements relating to the changes in ownership interests in subsidiaries and other businesses. Transaction costs associated with business combinations should be shown as operating activities, as they are not capitalised and, thus, cannot be incorporated in investing activities. The situation becomes more intricate with contingent consideration, recognised at the acquisition date at fair value, with a corresponding debit entry attributed to acquired assets or goodwill. The value of such contingent consideration may fluctuate due to post-acquisition events (e.g., achieving a specified revenue target). When paid, it should be apportioned between operating and investing activities. The amount recognised at the acquisition date is reported under investing activities, with the remaining balance allocated to operating activities.

Reporting cash flows on a gross vs. net basis

Generally, cash flows are reported on a gross basis, meaning cash receipts and cash payments are presented separately (IAS 7.21). This, of course, does not apply to the presentation of cash flows from operating activities using the indirect method. However, in specific scenarios, cash flows can be reported on a net basis (IAS 7.22-24). When an entity acts solely as an agent in handling cash receipts and payments on behalf of third parties, a net cash flow presentation is utilised (IAS 7.23). Additionally, cash receipts and payments for items characterised by quick turnover and short maturities are also reported on a net basis (IAS 7.23A). This typically concerns short-term borrowings, such as revolving credit lines.

Foreign currency cash flows

Typically, cash flows in foreign currency should be translated using the exchange rate applicable on the date of the cash flow. This translation rule extends to the cash flows of a foreign subsidiary in consolidated financial statements. As a practical expedient, IAS 7, like IAS 21, permits the use of the average exchange rate for the period when translating the cash flows of a foreign subsidiary (IAS 7.25-27). The effect of exchange rate fluctuations on cash and cash equivalents held in foreign currency is presented in the cash flow statement to reconcile the opening and closing balances of cash and cash equivalents. However, it is excluded from the three major activities and instead, presented as a reconciling item at the end of the cash flow statement (IAS 7.28).

Non-cash transactions

Investing and financing transactions that don’t directly impact current cash flows are not included in the statement of cash flows. Nevertheless, such transactions must be disclosed elsewhere in the financial statements (IAS 7.43-44). Examples include acquiring assets by assuming liabilities, through leases, or simply by exchanging one asset for another. However, non-cash transactions are presented under operating activities as adjustments to profit or loss when using the indirect method.

This extract from Severn Trent’s annual report illustrates disclosure of non-cash transactions:

Changes in liabilities arising from financing activities

IAS 7.44A-E stipulate a requirement for reconciliation between the opening and closing balances in the statement of financial position for liabilities arising from financing activities. This requirement is also applicable to changes in financial assets, such as hedging derivatives, if the cash flows from these assets were, or will be, included in cash flows from financing activities. Such reconciliation should encompass both cash and non-cash changes, including accrued interest, fluctuations in foreign exchange rates, or changes in fair values. It might prove beneficial to broaden such disclosure and combine it with the reconciliation of the opening and closing balance of net debt (if disclosed by the entity). Nonetheless, such a comprehensive reconciliation should distinctly outline changes in liabilities resulting from financing activities.

Voluntary disclosure

IAS 7.50-51 suggest voluntary disclosures relating to undrawn borrowing facilities, cash flows of each reportable segment, or differentiating cash flows that represent increases in operating capacity from those necessary to maintain it. The latter disclosure is seldom made in practice, particularly as IAS 7 does not provide additional guidance on distinguishing such cash flows.