The way financial assets and liabilities are classified determines how they are accounted for in financial statements, particularly how these financial instruments are measured following their initial recognition.

Let’s dive in.

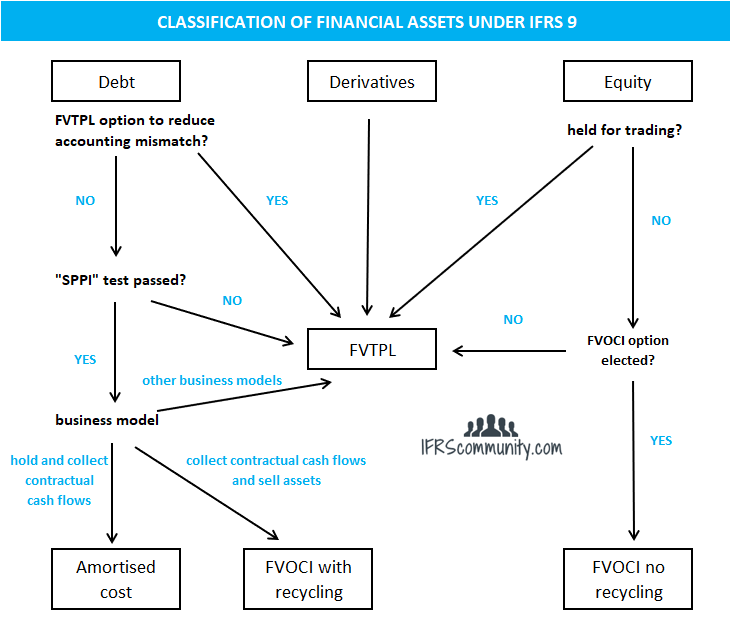

Classification of financial assets

The following decision tree summarises the classification of financial assets according to IFRS 9.

Too many IFRS updates? I know the feeling! That's why I created Reporting Period. It's a concise monthly summary of IFRS developments and Big 4 insights for accounting professionals. It's completely free, with zero spam, and you can unsubscribe anytime with one click. Interested? Leave your email below:

Categories of financial assets under IFRS 9

Financial assets are classified into one of the following measurement categories:

- Amortised cost.

- Fair value through other comprehensive income with recycling to P/L (‘FVOCI with recycling’).

- Fair value through other comprehensive income without recycling to P/L (‘FVOCI no recycling’).

- Fair value through profit or loss (‘FVTPL’).

These two factors are pivotal to classifying financial assets (IFRS 9.4.1.1):

- The entity’s business model for managing financial assets, and

- The contractual cash flow characteristics of the financial asset.

A financial asset should be measured at amortised cost if it satisfies both of the following conditions outlined in IFRS 9.4.1.2:

- The financial asset is held within a business model whose objective is to hold financial assets to collect contractual cash flows.

- The contractual terms of the financial asset generate cash flows on specified dates that solely constitute payments of principal and interest on the outstanding principal amount (‘SPPI’ test).

However, if a financial asset is held within a business model whose objective is achieved by both collecting contractual cash flows and selling financial assets, it is measured at fair value through other comprehensive income, with cumulative gains or losses recycled to P/L upon derecognition – a category referred to as ‘FVOCI with recycling’ (IFRS 9.4.1.2A). This is of course true if the SPPI test (point 2) is met. The order in which these two criteria (i.e. SPPI test and business model) are assessed is not particularly important, as we discussed in this forums topic.

If a financial asset does not fit into either of the two categories discussed above, it is measured at fair value through profit or loss – ‘FVTPL’ (IFRS 9.4.1.4). However, for equity instruments that are not held for trading or do not form part of a contingent consideration relating to business combination, an entity can irrevocably elect, at initial recognition, to present changes in their fair value in other comprehensive income without recycling to P/L upon derecognition – ‘FVOCI no recycling’ category (IFRS 9.4.1.4; 5.7.5).

Finally, IFRS 9 permits an entity, at initial recognition, to irrevocably designate a financial asset to the FVTPL category if this would eliminate or significantly decrease an inconsistency (‘accounting mismatch‘) in measurement or recognition (IFRS 9.4.1.5).

Business model for managing financial assets

An entity’s business model is determined at a level that reflects how groups of financial assets are managed together to achieve a business objective. This model is not based on intentions for individual instruments, but rather on a broader aggregation level, allowing for different business models within a single entity. For example, an entity might manage one portfolio for collecting contractual cash flows and another for trading to realise fair value changes.

The business model’s essence lies in its approach to generating cash flows, whether through collecting contractual flows, selling assets, or a combination of both. This assessment excludes unlikely scenarios like ‘worst case’ situations. Importantly, deviations in realising cash flows from previous expectations do not constitute prior period errors nor alter the classification of remaining financial assets, as long as the original assessment considered all relevant information.

The assessment of an entity’s business model for managing financial assets is a fact-based exercise, not merely an assertion. This assessment is evident through the activities conducted to meet the business model’s objectives and requires judgment. An entity must consider all relevant evidence available at the time of assessment. Such evidence includes how the business model and its financial assets’ performance are reported to key management, how risks affecting the model and assets are managed, and the basis of managers’ compensation (IFRS 9.B4.1.1-B4.1.2B).

Collecting contractual cash flows

A business model whose objective is to hold assets in order to collect contractual cash flows emphasises managing assets primarily for the collection of their contractual cash flows over their life, rather than for overall portfolio returns through both holding and selling. In assessing whether a business model is oriented towards collecting these cash flows, it’s crucial to consider the historical pattern of sales – their frequency, value, timing, and the reasons behind them – in conjunction with expectations about future sales activities. Thus, an entity must evaluate past sales in light of the reasons for these sales and the conditions at that time, comparing them with the present conditions.

Furthermore, the presence of sales in a portfolio does not negate a business model aimed at collecting contractual cash flows. For instance, sales triggered by an increase in the credit risk of financial assets, regardless of their frequency or value, align with the model’s objective. This is because managing credit risk is integral to ensuring the collection of contractual cash flows.

Sales for other reasons, like managing credit concentration risk without an increase in credit risk, can still be consistent with this model, provided these sales are infrequent or insignificant in value, individually and in aggregate. It’s essential for entities to assess the consistency of such sales with their objective of collecting cash flows. Furthermore, sales made close to maturity that approximate the collection of the remaining contractual cash flows also align with this business model’s objective.

Collecting contractual cash flows and selling assets

In a business model whose objective is achieved by both collecting contractual cash flows and selling financial assets, the management recognises that this dual approach is essential to achieving the model’s objectives. These objectives may vary, encompassing the management of daily liquidity needs, maintaining a specific interest yield profile, or aligning the duration of financial assets with the liabilities they fund. Unlike models focused solely on holding assets for cash flow collection, this approach typically involves a higher frequency and volume of sales, given that selling assets is a core component of the strategy, not merely incidental. Notably, there is no predefined threshold for sales frequency or volume in this model, as both collecting cash flows and selling assets are fundamental to achieving its intended goals (IFRS 9.B4.1.4A-C).

Example: Investing funds for future capital expenditure

Consider an entity that prepares for future capital expenditure and plans to invest its excess cash in both short and long-term financial assets. This strategy is tailored to fund the anticipated expenditure by balancing the collection of contractual cash flows with the opportunistic selling of financial assets. As many of these assets have contractual lives extending beyond the entity’s expected investment period, the entity’s business model is designed to maximise returns by deciding, on an ongoing basis, whether to collect cash flows or sell assets for reinvestment in higher-return options.

This approach, which involves both collecting cash flows and selling assets, contrasts with a different business model where an entity facing a similar capital expenditure timeline invests exclusively in short-term financial assets. In this alternative model, the entity continuously reinvests in new short-term assets until the need for capital arises, primarily focusing on holding assets to collect contractual cash flows, with only minor sales before maturity.

This comparison highlights two business models in financial asset management: one that balances collecting contractual cash flows and selling assets, and another that prioritises holding assets for their contractual cash flows.

Other business models

Financial assets that do not align with either of the two business models are measured at fair value through profit or loss. This measurement applies, for instance, to a business model where the primary objective is to realise cash flows through the active buying and selling of assets. In such a model, the collection of contractual cash flows occurs, but it is incidental, not integral, to achieving the business model’s objective.

This approach is also exemplified by portfolios managed and evaluated on a fair value basis, as outlined in IFRS 9.4.2.2(b), where the focus is solely on fair value for assessing performance and making decisions. Similarly, portfolios that meet the definition of being held for trading fall under this category, as their management is not aimed at collecting contractual cash flows but primarily on realising fair value (IFRS 9.B4.1.5-6).

Contractual cash flow characteristics (‘SPPI test’)

The SPPI (Solely Payments of Principal and Interest) test assesses whether the cash flows from a financial asset are solely payments of principal and interest on the outstanding principal amount, as expected in a basic lending arrangement. If a financial asset fails this test, it must be measured at fair value through profit or loss (FVTPL). This is because, as stated by the IASB in IFRS 9.BC4.158, the amortised cost measurement only provides relevant and useful information for financial assets with ‘simple’ contractual cash flows. More complex cash flows require a fair value overlay to contractual cash flows to ensure that the reported financial information provides useful information (IFRS 9.BC4.172).

Examples of financial assets that pass the SPPI test include (IFRS 9.B4.1.13):

- A bond denominated in Euros, with a specified maturity date. The payments, consisting of principal and interest on the outstanding principal, are indexed to Eurozone inflation. This inflation linkage is not leveraged.

- A variable interest rate loan, also with a defined maturity date, which allows the borrower to select the applicable market interest rate at regular intervals. For instance, at each rate reset date, the borrower may choose either the three-month SONIA benchmark rate for a three-month period or the one-month SONIA rate for a one-month period.

- A bond with a predetermined maturity date that offers a variable market interest rate, subject to a maximum cap.

In contrast, examples of financial assets that do not pass the SPPI test include (IFRS 9.B4.1.14):

- A bond with a specified maturity date, where payments of principal and/or interest on the outstanding principal amount are tied to the issuer’s revenue growth.

- A convertible bond that can be exchanged for a fixed number of the issuer’s equity instruments.

- A loan featuring an inverse floating interest rate, meaning the interest rate moves inversely to market interest rates.

- A perpetual bond which the issuer has the option to redeem at any time, paying the holder the face value plus any accrued interest. In this case, deferred interest does not accumulate additional interest.

Principal

‘Principal’ in the context of the SPPI test refers to the fair value of the financial asset at initial recognition. Naturally, the principal amount may change over the life of the financial asset, for instance, if there are repayments of principal (IFRS 9.4.1.3(a); B4.1.7B). It is critical to note that ‘principal’ in this context does not equate to the face value of an instrument. However, in practical terms, the terms ‘principal’ and ‘face value’ are often used interchangeably. Consider the following example:

Example: Principal vs face value in the SPPI test

Entity A purchases a bond with a face value of $1,000 and an annual coupon of 5%. Due to falling market interest rates, the bond trades at $1,020, which is the amount Entity A pays for the bond (i.e., its fair value). In this context, the bond’s principal for Entity A is $1,020.

Interest

‘Interest’ is considered in IFRS 9.4.1.3(b) as the compensation for:

- The time value of money,

- Credit risk associated with the outstanding principal amount,

- Other basic lending risks and costs, and

- Profit margin.

However, if contractual terms introduce exposure to risks or volatility unrelated to a basic lending arrangement, such as exposure to changes in equity prices or commodity prices, the SPPI test is not met because the contractual cash flows are not solely payments of principal and interest (IFRS 9. B4.1.7A).

Generally, the market in which the transaction occurs is relevant to the assessment of the time value of money element. For instance, in the UK, it is common to reference interest rates to SONIA benchmark. If the time value of money element is modified (‘imperfect’), such as when the interest rate resets every month to a one-year rate, an additional assessment is needed to determine if the SPPI test is met, as described in IFRS 9.B4.1.9A-E.

Prepayable financial assets

For financial assets that are prepayable, IFRS 9.B4.1.12 offers an exception to the general criteria, allowing certain instruments with contractual prepayment features to pass the SPPI test. This exception applies to many purchased credit-impaired financial assets and financial assets originated at below-market interest rates (IFRS 9.BC4.193-195), among others.

Option to designate a financial asset at FVTPL

IFRS 9.4.1.5 states that an entity may, upon initial recognition, irrevocably designate a financial asset as measured at FVTPL if this classification significantly reduces or eliminates a measurement or recognition inconsistency, commonly known as ‘accounting mismatch’.

Understanding accounting mismatch

The concept of an accounting mismatch involves two ideas. Firstly, certain assets and liabilities of an entity are measured, or gains and losses are recognised, inconsistently. Secondly, there exists a perceived economic relationship between these assets and liabilities. For instance, a liability may be perceived as related to an asset if they share a risk that causes opposite changes in fair value that typically offset each other, or when the entity considers the liability as funding for the asset (IFRS 9.BCZ4.61). IFRS 9.B4.1.30 provides examples when these conditions could be met. For practical reasons, the entity doesn’t have to enter into all the assets and liabilities creating the accounting mismatch simultaneously (IFRS 9.B4.1.31).

It’s permissible to designate only a portion of a set of similar financial assets or liabilities if this results in a greater reduction of the accounting mismatch. However, IFRS 9.B4.1.32 prohibits to designate only a component of a financial instrument (such as a specific risk) or a proportion of it.

Hybrid contract with non-financial asset as a host

IFRS 9 also provides a fair value option for hybrid contracts that contain embedded derivatives with a non-financial asset as the host (IFRS 9.4.3.5). IFRS 9.B4.3.9 points out that measuring an entire hybrid contract at FVTPL can be simpler than separating embedded derivatives. However, this option is not permitted if any of the conditions outlined in IFRS 9.4.3.5 are applicable (refer to IFRS 9.BCZ4.70 for further discussion).

Option to designate an equity instrument at FVOCI (no recycling)

Upon initial recognition, an entity may irrevocably elect to present subsequent changes in the fair value of an investment in an equity instrument within the scope of IFRS 9 in OCI, provided the instrument is neither held for trading nor contingent consideration recognised by an acquirer in a business combination (IFRS 9.5.7.5). This election is made on an instrument-by-instrument basis (i.e., share-by-share) (IFRS 9.B5.7.1).

The definition of equity instruments can be found in IAS 32. It should be noted that the specific treatment of certain puttable instruments (for example, investment funds), which can be classified as equity by the issuer, does not apply to the option available for the holder discussed here (IFRS 9.BC5.21 and this agenda decision). Hence, the FVOCI (no recycling) option cannot be used in accounting for investments in mutual or hedge funds. This forums topic discusses this further.

Hybrid contracts

The criteria for the classification of financial assets should be applied to the entire hybrid contract, that is, both the host and the embedded derivative together (IFRS 9.4.3.2).

Reclassification of financial assets

Reclassification criteria

An entity should reclassify all impacted financial assets only when there is a change in its business model for managing these assets (IFRS 9.4.4.1). Changes in the business model are inherently infrequent and significant to the entity’s operations. They stem from internal or external factors, are approved by senior management, and must be apparent to external parties (IFRS 9.B4.4.1).

A change in business model can be exemplified by scenarios such as an entity shifting from holding commercial loans for short-term sale to acquiring them for long-term cash flow collection. This is seen when an entity acquires a company that manages loans differently, leading to a strategic change in managing their loan portfolio. Another instance is a financial services firm closing its retail mortgage sector, ceasing new business and actively selling its mortgage loan portfolio. However, mere changes in intentions towards specific financial assets, reactions to market condition fluctuations, the temporary loss of a market, or transfers of assets between different business models within an entity do not qualify as changes in the business model (IFRS 9.B4.4.1-3).

Measurement implications

The reclassification is accounted for prospectively from the reclassification date, defined as the first day of the first reporting period following the business model change. As a result, previously recognised gains, losses (including impairments), or interest are not restated (IFRS 9.5.6.1). Guidance on accounting for reclassifications between specific categories is given in IFRS 9.5.6.2-7 and IFRS 9.B5.6.1-2, with accompanying illustrations in Example 15 to IFRS 9.

Disclosure

IFRS 7.12B-D detail the disclosure requirements relating to the reclassification of financial assets.

Financial assets and liabilities held for trading

A financial asset or liability is classified as ‘held for trading’ if it fulfils, as per IFRS 9 Appendix A, at least one of the following criteria:

- It is primarily acquired or incurred for selling or repurchasing in the near future.

- Upon initial recognition, it’s part of a portfolio of identified financial instruments managed together and showing evidence of a recent pattern of short-term profit-taking (refer to IFRS 9.IG.B.11).

- It is a derivative, excluding a derivative that is a financial guarantee contract or a designated and effective hedging instrument.

IFRS 9 further elaborates that ‘held for trading’ usually indicates active and frequent buying and selling. Financial instruments under this classification are generally used to generate profit from short-term price fluctuations or dealer’s margin (IFRS 9.BA.6). Examples of financial liabilities held for trading are provided in IFRS 9.BA.7. When classified as ‘held for trading’, a financial asset or liability is measured at fair value through profit or loss (FVTPL).

Classification of financial liabilities

Categories of financial liabilities under IFRS 9

Financial liabilities are classified into one of the following categories (IFRS 9.4.2.1):

- Measured at amortised cost.

- Measured at fair value through profit or loss (FVTPL).

- Designated at fair value through profit or loss (FVTPL).

Generally, a liability is measured at amortised cost, unless it is a financial liability held for trading or designated at FVTPL. In addition, specific measurement requirements are given for:

- Financial guarantee contracts,

- Commitments to provide a loan at below-market interest rate,

- Contingent consideration recognised by an acquirer in a business combination; and

- Financial liabilities that arise when a transfer of a financial asset does not qualify for derecognition or when the continuing involvement approach applies (IFRS 9.4.2.1).

Liabilities designated at FVTPL

At initial recognition, an entity may irrevocably designate a financial liability to be measured at FVTPL when:

- it contains embedded derivatives (subject to conditions outlined in IFRS 9.4.3.5),

- doing so eliminates an accounting mismatch, or

- when a group of financial liabilities or financial assets and financial liabilities is managed and evaluated on a fair value basis (IFRS 9.4.2.2).

Financial liability managed on a fair value basis

This option to designate financial liabilities to be measured at FVTPL applies when an entity manages a group of financial liabilities or financial assets and financial liabilities in a manner that results in more relevant information if the group is measured at FVTPL. The emphasis here is on how the entity manages and evaluates performance, rather than the nature of its financial instruments (IFRS 9.B4.1.33).

To use this option (IFRS 9.4.2.2(b)), an entity must:

- Have a documented risk management or investment strategy (refer also to IFRS 9. B4.1.36); and

- Provide information about the group of financial liabilities (and financial assets, if relevant) internally to its key management personnel on that basis.

Although this option is not explicitly available for financial assets, there’s no need for it as financial assets managed on a fair value basis would fall into the FVTPL category based on the business model criterion.

Reclassification of financial liabilities

Reclassification of financial liabilities is prohibited as per IFRS 9.4.4.2.

More about financial instruments

See other pages relating to financial instruments:

Scope of IAS 32

Financial Instruments: Definitions

Derivatives and Embedded Derivatives: Definitions and Characteristics

Classification of Financial Assets and Financial Liabilities

Measurement of Financial Instruments

Amortised Cost and Effective Interest Rate

Impairment of Financial Assets

Derecognition of Financial Assets

Derecognition of Financial Liabilities

Factoring

Interest-Free Loans or Loans at Below-Market Interest Rate

Offsetting of Financial Instruments

Hedge Accounting

Financial Liabilities vs Equity

IFRS 7 Financial Instruments: Disclosures