At the commencement of a lease, a lessee recognises the following:

- Right-of-use (RoU) asset representing its right to use the underlying leased asset throughout the lease term, and

- Lease liability representing its obligation to make lease payments.

The RoU asset is initially measured at cost, primarily comprising of an amount equivalent to the recognised lease liability, and any initial direct costs. The subsequent measurement involves applying depreciation and assessing impairment charges.

On the other hand, the lease liability is initially measured at the present value of lease payments. These primarily include fixed and certain variable lease payments. The subsequent measurement of the lease liability is impacted by the accumulation of interest, scheduled repayments, and remeasurements that reflect any lease reassessments or modifications.

Let’s dive in.

Initial measurement of the right-of-use asset

Components of the right-of-use asset

The right-of-use asset is measured at cost at the commencement date. As outlined in IFRS 16.24, the RoU cost includes:

- An amount equivalent to the lease liability on initial recognition,

- Lease payments made on or before the lease’s commencement date, less any lease incentives received,

- Any initial direct costs incurred by the lessee; and

- An estimate of costs expected to be incurred by the lessee for dismantling and removing the underlying asset, restoring the site where it is located or restoring the underlying asset to the condition stipulated by the lease terms and conditions, excluding those costs related to producing inventories.

Example: Initial measurement of the right-of-use asset and lease liability

Let’s explore an example to illustrate the initial measurement of a lease based on the following assumptions:

- Commencement date: 1 January 20X1

- Discount rate: 5%

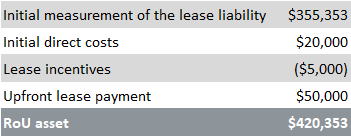

- Initial direct costs: $20,000

- Lease incentives: $5,000

- Upfront lease payment made before lease commencement date: $50,000

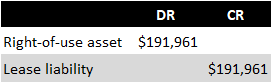

Initially, it’s essential to calculate the present value of the lease liability. This is done by discounting future lease payments to the lease commencement date. A handy tool for this is the XNPV spreadsheet function, producing a present value of future lease payments amounting to $355,353. Please refer to the included Excel file to view all calculations related to this example.

With the lease liability established, we can then determine the right-of-use asset, which stands at $420,353:

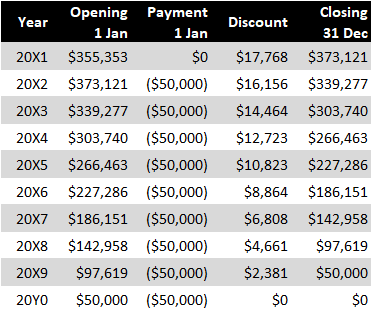

The subsequent lease liability and RoU accounting schedules are presented below.

Each year, the lease liability increases due to the unwinding of the discount (charged as finance costs in P/L) and decreases with each payment made:

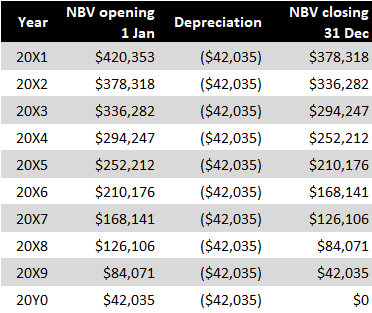

The carrying amount of the RoU asset decreases with depreciation charged each year:

As we can see, total lease payments amount to $515,000 (including initial direct costs, lease incentives, and the upfront lease payment). The total expense recognised during the lease term also amounts to $515,000, divided between depreciation expense ($420,353) and discounting expense ($94,647).

It’s worth noting that in most lease agreements, payments are made monthly, often mid-month. As such, I’ve created an additional Excel file showcasing the recognition and measurement of a lease that involves monthly payments.

--

Too many IFRS updates? I know the feeling! That's why I created Reporting Period. It's a concise monthly summary of IFRS developments and Big 4 insights for accounting professionals. It's completely free, with zero spam, and you can unsubscribe anytime with one click. Interested? Leave your email below:

Occasionally, a lease might start with a rent-free period. Though these periods are sometimes labelled as ‘lease incentives,’ it’s important to note that they don’t meet the definition of lease incentives in IFRS 16. Rent-free periods are, in essence, a way of distributing lease payments throughout the lease term. As such, the IFRS 16 requirements lead to depreciation and interest charges being spread across the lease period, including rent-free periods, without any manual adjustments to the general recognition model.

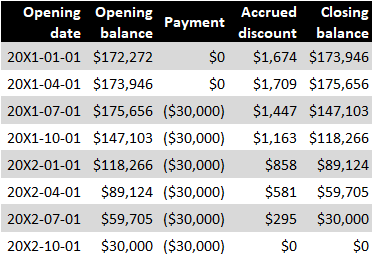

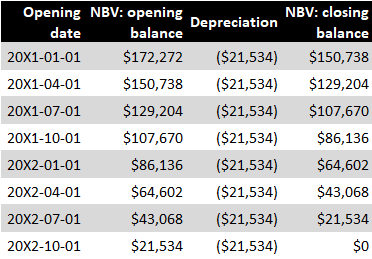

Here’s an example of a 2-year lease commencing on 1 January 20X1 with a quarterly rent of $30,000 paid upfront, but with the first two quarters being rent-free. The discount rate in this example is 4%. For a more detailed explanation of how to account for a typical lease, please refer to the previous example.

In this case, assume that there are no initial direct costs or lease incentives received, so the RoU asset at initial recognition equals the lease liability’s initial measurement, totalling $172,272. Please refer to this Excel file for the calculations.

Subsequent accounting is identical to a lease without rent-free periods. The RoU asset is depreciated each year, and the interest expense is accrued on the lease liability. The only difference, compared to a lease without any rent-free periods, concerns lease liability repayments as there aren’t any during the first two quarters. Consequently, the carrying amount of a lease liability increases during these rent-free periods due to accrued interest (discount).

Here’s the subsequent lease liability accounting:

As usual, the carrying amount of the RoU asset decreases each quarter with the depreciation charged:

Initial direct costs

Initial direct costs are incremental costs of obtaining a lease that would not have been incurred if the lease had not been obtained (IFRS 16 Appendix A). The concept of initial direct costs aligns closely with the definition of incremental costs of obtaining a contract in IFRS 15.

Examples of initial direct costs added to the cost of a right-of-use asset under IFRS 16.24(c) include:

- Commissions paid to employees or external agents who facilitated the lease agreement, provided that these are payable only upon the lease contract’s signing,

- Legal expenses such as stamp duties that are incurred during the signing of the contract.

However, not all direct costs can be incorporated in the cost of the RoU asset. These include:

- Overhead cost allocations,

- Advisory fees that are incremental but would be incurred regardless of whether a lease contract is ultimately signed.

There is also a category of initial direct costs about which IFRS 16 does not provide explicit guidance. This involves costs directly attributable to bringing a RoU asset to the location and condition necessary for it to be capable of operating in the manner intended by management, also known as ‘asset costs’ rather than ‘contract costs’. This is linked to IAS 16, which explicitly permits the inclusion of such costs in the cost of property, plant and equipment (PP&E). The same approach can be applied to RoU assets, a perspective indirectly supported by IFRS 16.BC149.

Lease payments made at or before the commencement date

Lease payments made at or before the commencement date are excluded from the lease liability. However, they are incorporated into the measurement of right-of-use assets under IFRS 16.24(b).

Security deposits paid

Some lessors demand a security deposit that will be refunded when the leased asset is returned by the lessee. These deposits are considered a separate financial asset at amortised cost under IFRS 9. As these deposits often do not bear interest, their initial recognition‘s fair value is less than the cash paid. This difference should be treated as an initial direct cost and added to the RoU asset (see a similar example with security deposit paid by a contractor).

Lease incentives

Lease incentives are commonly used by lessors to encourage potential lessees to enter into lease agreements, and these incentives can take various forms, such as upfront cash payments, reimbursement of costs, rent-free periods, and more.

According to the definition in Appendix A of IFRS 16, lease incentives are payments made by a lessor to a lessee, or reimbursements or assumptions of the lessee’s costs. The standard does not elaborate extensively on this definition, nor does it provide comprehensive guidance on the different types of arrangements that may qualify as lease incentives. In general, payments that are not made for the transfer of distinct goods or services or costs incurred on behalf of the lessor are considered lease incentives.

Lease incentives are accounted for as a reduction of the RoU asset in accordance with IFRS 16.24(b). For further information, refer to Grant Thornton’s technical publication on this topic.

Reimbursement of leasehold improvements

In 2020, the IASB amended Illustrative Example 13 to IFRS 16, clarifying that reimbursements of leasehold improvements could not be automatically classified as non-lease incentives. If these payments economically indicate reimbursement for improvements made to the lessor’s asset, then indeed – they are not lease incentives. Indicators that leasehold improvements benefit the lessor’s asset include:

- Leasehold improvements would be necessary for most entities to use the leased asset (e.g., installing walls in a building),

- Assets constructed during the leasehold improvement process are not specialised to the lessee’s needs,

- Economic useful life of leasehold improvements exceeds enforceable lease term.

Leasehold improvements are separately recognised under IAS 16. If the reimbursement is not classified as a lease incentive, it is treated as a reduction of their cost.

Conversely, if the leasehold improvements are considered an asset of the lessee, any reimbursement made by the lessor should be treated as a lease incentive and accounted for as a reduction of the right-of-use asset recognised under IFRS 16.

Initial measurement of the lease liability

Components of the lease liability

The lease liability should be initially recognised and measured at the present value of the lease payments for the right to use the underlying asset during the lease term (IFRS 16.26-27). These payments include:

- Fixed payments, less any lease incentives receivable,

- Variable lease payments that depend on an index or a rate,

- Amounts the lessee expects to pay under residual value guarantees,

- Exercise price of a purchase option if the lessee is reasonably certain to exercise that option; and

- Penalty payments for lease termination if the lease term reflects the lessee’s choice to terminate the lease.

An example of the initial measurement of the right-of-use asset and lease liability can be found in earlier sections. Please also refer to Example 13 accompanying IFRS 16.

Fixed payments

Fixed payments refer to the sums paid by a lessee to a lessor for the right to use an underlying asset during the lease term, excluding variable lease payments (IFRS 16 Appendix A).

Variable lease payments

Variable lease payments are a portion of payments made by a lessee to a lessor during the lease term that can change due to changes in facts or circumstances occurring after the commencement date, excluding passage of time (IFRS 16 Appendix A). It’s important to remember that not all variable payments are included in the measurement of lease liability and right-of-use assets. Only those variable payments tied to an index or a rate are considered in both initial and subsequent measurements. These payments could be tied to a predetermined index (e.g., CPI), benchmark rate (e.g., LIBOR), or may fluctuate to mirror changes in market rental rates (IFRS 16.28).

In the initial recognition of lease liability, variable lease payments are measured using the actual value of an index or a rate at the commencement date (IFRS 16.27(b)). This implies that the lessee cannot use forward rates or forecasting techniques in measuring variable lease payments (IFRS 16.BC166).

Variable payments that are independent of an index or a rate, particularly those tied to the future activity of a lessee or a leased asset, are excluded from the measurement of lease liability and right-of-use asset. These are recognised in P/L (or capitalised in another asset’s cost) in the period in which the event or condition that triggers the payments occurs (IFRS 16.38(b)). Typical examples of such payments recognised in P/L as they occur include:

- Payments tied to the performance of the leased asset (e.g., a specified % of revenue, physical output of the leased asset),

- Payments for specific units related to future usage (e.g., specified mileage of a leased car),

- Payments linked to taxes or levies imposed on the leased asset (see this forums post).

Please see paragraphs IFRS 16.BC168-BC169 for more discussion and Example 14 accompanying IFRS 16.

Please note that some variable lease payments may actually be in-substance fixed lease payments.

In-substance fixed lease payments

Fixed payments may also include those that, though variable in form, are unavoidable in reality. These payments are referred to as ‘in-substance fixed lease payments’ and are further discussed in IFRS 16.B42.

Example: In-substance fixed lease payments

Scenario A

Retailer A signs a five-year lease for retail space. The fixed monthly lease payments amount to only $50, but this increases to $1,000 if the revenue from the point of sale situated on the leased space surpasses $3,000 per month. Retailer A must keep the point of sale open for at least eight hours a day. The likelihood of revenue not exceeding $3,000 per month is remote.

According to IFRS 16.B42(a)(ii), in-substance fixed payments are payments originally structured as variable lease payments linked to the use of the underlying asset, but their variability is resolved at some point after the start date, thus making the payments fixed for the remainder of the lease term. These payments turn into in-substance fixed payments when the variability is resolved and are then recognised in the lease liability and RoU asset.

In the scenario outlined above, Retailer A recognises a lease liability composed of monthly lease payments of $1,000 as there is no real variability in these lease payments.

Scenario B

Retailer B signs a four-year lease for retail space with no fixed lease payments. Instead, Retailer B pays the lessor a variable lease fee equivalent to 4% of revenue generated from the point of sale situated on the leased space.

In this case, the lease payments exhibit genuine variability. Hence, there are no lease payments to include in the lease liability measurement. Instead, the variable lease fee is charged directly to P/L every month.

VAT and other non-recoverable taxes

IFRS 16 does not provide guidance on the treatment of VAT, sales tax, and similar taxes imposed on lease payments (all these taxes are referred to as ‘VAT’ in this section). When VAT can be reclaimed from tax authorities via some form of tax returns, the accounting is straightforward: VAT is recognised as a receivable from, or payable to, tax authorities when the obligation arises. It becomes more complex when such taxes cannot be reclaimed.

As VAT is a levy imposed by the government, it falls under the scope of IFRIC 21. Consequently, VAT payments not being lease payments made by the lessee to the lessor in exchange for the right to use an underlying asset should be excluded from the lease liability. Instead, they should be expensed in the P/L immediately when they are due. VAT can be added to RoU’s initial recognition amount as initial direct costs, but only if the VAT is payable upfront at the commencement of the lease. For more information, refer to this staff paper and this topic.

Residual value guarantees

A residual value guarantee is an assurance to a lessor that the value of an asset at the end of a lease will be a minimum specified amount. The estimated payments by the lessee under such guarantees are included in the initial measurement of a lease liability (IFRS 16.27(c)).

Purchase option

If the lessee is reasonably certain to exercise a purchase option, the exercise price of this option is included in the initial measurement of a lease liability. The same criteria used for assessing lease term should be applied when determining whether a lessee is reasonably certain to exercise the option.

Non-lease components

Payments relating to non-lease components are excluded from the measurement of lease liability, unless the lessee applies this practical expedient.

Discount rate

Determining the discount rate

In measuring lease liability, lease payments are discounted using the interest rate implicit in the lease, assuming this rate can be readily determined. However, IFRS 16 doesn’t define what ‘readily determined’ means. One possible interpretation could be that a rate is easily determinable if its calculation does not require significant estimates or assumptions.

More often than not, lessees find it difficult to readily determine the rate implicit in the lease, primarily because it is influenced by factors only the lessors know (e.g. lessor’s initial direct costs). Furthermore, this implicit interest rate differs from the rate explicitly stated in the lease contract. Consequently, lessees typically use their incremental borrowing rates, as permitted by IFRS 16.26.

Interest rate implicit in the lease

The interest rate implicit in the lease is a rate that makes the present value of both (a) the lease payments and (b) the unguaranteed residual value equivalent to the sum of (i) the fair value of the underlying asset and (ii) any initial direct costs of the lessor (IFRS 16 Appendix A).

The unguaranteed residual value refers to the part of the residual value of the underlying asset, the realisation of which is uncertain for the lessor or is guaranteed solely by a party related to the lessor (IFRS 16 Appendix A).

As previously noted, it’s rare for a lessee to easily determine the implicit interest rate, thus they often resort to using the incremental borrowing rate. You can find an example of the calculation of an interest rate implicit in the lease on the page on lessor accounting.

Incremental borrowing rate

The lessee’s incremental borrowing rate is the interest rate a lessee would need to pay to borrow, over a similar term and with comparable security, the funds required to obtain an asset of similar value to the right-of-use asset in a comparable economic environment (IFRS 16 Appendix A). A rate that can be readily observed is typically used as a starting point when determining the incremental borrowing rate (IFRS 16.BC162). This observable rate might be an entity’s actual borrowing rate or a property yield for property leases. Entities may also use their cost of debt.

This observable rate must then be adjusted to reflect the maturity profile of a lease and the type of asset being leased.

In situations where a subsidiary uses financing centralised by a parent, the actual borrowing rate should be adjusted to account for differences in the credit ratings of these entities.

For lease payments denominated in foreign currency, the discount rate appropriate for that specific foreign currency should be used.

Lease commencement date

A right-of-use asset and the related lease liability are recognised at the commencement date, defined as the date a lessor makes an underlying asset available for use by the lessee. For recognition purposes, it’s not the lease agreement date or commitment date that matters (i.e., lease inception), but rather the lease commencement date (IFRS 16.BC141-BC144). Lease commencement and inception dates are defined in Appendix A to IFRS 16.

It might seem counter-intuitive, but in some instances, the lease commencement date can occur before the date specified in the lease contract. For example, a lessee may take control of the leased space and use it for constructing leasehold improvements before deploying it for operational activity. In such cases, the start of lease payments or the date specified in the contract does not impact the IFRS-compliant lease commencement date. If the lease commencement date determined under IFRS 16 precedes the payment initiation, the right-of-use asset and related liability should be recognised at the commencement date. The gap between this date and when the payments begin should be treated as a ‘rent-free‘ period (IFRS 16.B36).

Subsequent measurement of the right-of-use asset

The right-of-use asset is typically measured at cost unless the lessee opts to apply the fair value model as per IAS 40 or the revaluation model under IAS 16 (as per IFRS 16.29).

Elements of cost

Under the cost model, the subsequent measurement of a right-of-use asset is its cost, after deducting any depreciation and accumulated impairment losses (IFRS 16.30). This cost is then subsequently adjusted to reflect any remeasurements of the lease liability due to reassessments or modifications to the lease.

Depreciation

The RoU asset is depreciated according to the requirements set forth in IAS 16 (IFRS 16.31). However, unlike for owned assets, the depreciation of RoU asset should start on the lease commencement date irrespective of whether the underlying asset is ‘in the location and condition necessary for it to be capable of operating in the manner intended by management’ (IFRS 16.32).

The depreciation period for RoU should not extend beyond the lease term, except when the lease agreement provides for the transfer of the underlying asset’s ownership to the lessee at the lease term’s end, or if the cost of the right-of-use asset indicates that the lessee intends to exercise a purchase option (IFRS 16.32).

Impairment

Right-of-use assets are subject to impairment requirements of IAS 36. Typically, RoU assets are integrated into a cash generating unit and, as such, are not individually tested for impairment. For further details, refer to this comprehensive publication by EY.

Fair value and revaluation model

If a lessee applies the fair value model to its investment properties, this same accounting approach should be applied to RoU assets that are classified as investment property under IAS 40 (IFRS 16.34).

Furthermore, if a lessee uses the revaluation model for property, plant, and equipment under IAS 16, they may choose to apply this model to all RoU assets associated with the same class of PP&E (IFRS 16.35).

Subsequent measurement of the lease liability

Following initial recognition, the measurement of a lease liability is influenced by the following factors as per IFRS 16.36:

- Interest accrued on the lease liability,

- Lease payments made, and

- Remeasurements due to any reassessment or lease modifications.

Accruing interest on the lease liability

Lease liabilities are measured on an amortised cost basis, similar to other financial liabilities, as stated in IFRS 16.37. Interest is recognised in P/L unless it can be capitalised under IAS 23.

Lease payments

Lease payments reduce the carrying amount of the lease liability. Variable lease payments not included in the initial measurement are recognised in P/L when the event or condition triggering these payments occurs.

Reassessments of the lease liability

Reassessments of lease liability are treated as adjustments to the RoU asset. If the carrying amount decreases to zero, any further reduction is immediately recognised in P/L as mandated by IFRS 16.39.

The lease liability is reassessed under the following circumstances (IFRS 16.40,42):

- Change in the lease term assessment.

- Reassessment of an option to purchase the underlying asset.

- Revision to the amounts expected to be payable under a residual value guarantee.

- Adjustment to future lease payments resulting from a change in an index or rate used to determine those payments.

Reassessments under points 1 and 2 require a revised discount rate, while those under points 3 and 4 use the original discount rate. However, if the reassessment under point 4 is triggered by a change in floating interest rates, a revised discount rate is used (IFRS 16.41,43).

Note that reassessments are different from remeasurements resulting from lease modifications.

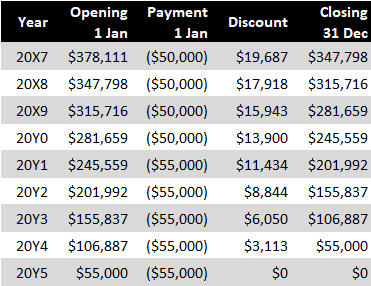

Example: Reassessment of the lease term with updated discount rate

In this example, we will reuse the data from the initial recognition example. Let’s assume that the lease term is reassessed at the end of year 20X6 and extended to 31 December 20Y5. The payments for years 20Y1-20Y5 will be $55,000, and the discount rate is also revised upwards from 5% to 6%. On the reassessment date, the entity determines the lease liability’s present value to be $378,111. All calculations are available for download in an Excel file.

Prior to reassessment, the lease liability was valued at $186,151 (value at the end of year 20X6, refer to the initial recognition example). The entity should recognise the increase in lease liability as follows:

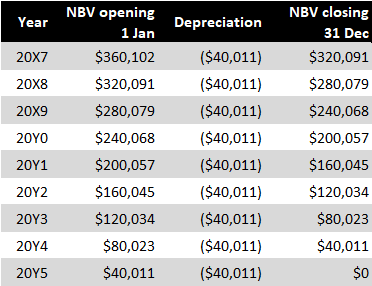

The resulting entries increase the value of the RoU asset to $360,102 (which was $168,141 at the end of year 20X6). The subsequent accounting schedules for the lease liability and right-of-use asset are presented below.

Lease liability:

RoU asset:

Changes in an index or a rate

Variable lease payments linked to an index or a rate are reassessed when future lease payments change. In other words, the adjustment is recognised only when the change to lease payments takes effect (IFRS 16.BC188-BC190).

Foreign currency exchange

IFRS 16 does not provide specific provisions regarding the impact of foreign currency exchange differences on lease liabilities. Consequently, general IAS 21 provisions apply. Particularly, this implies that the right-of-use asset’s value cannot be adjusted by the foreign currency exchange differences arising on lease liabilities (IFRS 16.BC196-BC199).

Consolidation procedures for intragroup leases

Accounting for leases differs considerably between lessees and lessors, which often complicates the preparation of consolidated financial statements for groups involved in intragroup leases. Regrettably, this issue doesn’t have a straightforward resolution.

One approach to address this issue is that, within the consolidation journal alone, the lessee could treat the lease contract as a traditional operating lease. This method could facilitate automatic intragroup eliminations by the consolidation software.

An alternative strategy could involve the consolidation team manually reversing all balances related to the intragroup leases, thereby cancelling out lease income against the depreciation of the right-of-use asset and associated finance costs. It’s important to note that these amounts won’t be identical. Therefore, any discrepancies must be tracked and accounted for within retained earnings until the lease period concludes.

For additional information on this topic, please refer to the summary provided by KPMG.

More about IFRS 16

See other pages relating to IFRS 16: