Most entities undertake some form of risk management, often using derivatives for this purpose. Hedge accounting aims to represent the effect of an entity’s risk management activities, which use financial instruments to manage exposures arising from specific risks that could affect profit or loss or other comprehensive income (IFRS 9.6.1.1).

The application of hedge accounting is optional, but often beneficial (IFRS 9.6.5.1). Without specific hedge accounting requirements, many risk management strategies could result in an accounting mismatch, as differing accounting rules may be applicable to assets or liabilities that economically form a hedging relationship. For instance, companies frequently use derivatives, always measured at fair value through profit or loss, to hedge current or anticipated exposures. In contrast, the hedged exposures can be accounted for at cost (like inventories), amortised cost (such as debt), or might not yet be recognised in the financial statements (for example, highly probable future purchases or sales).

There are three types of hedge relationships: fair value hedges, cash flow hedges, and hedges of a net investment in a foreign operation. Entities choosing to apply hedge accounting must document the hedge relationship in advance and use only eligible hedged items and hedging instruments.

Let’s dive in.

Qualifying criteria for hedge accounting

A hedging relationship is eligible for hedge accounting only if all of the following criteria (IFRS 9.6.4.1) are met:

- The hedging relationship consists solely of eligible hedging instruments and eligible hedged items.

- At the inception of the hedging relationship, there is formal designation and documentation of the hedging relationship, along with the entity’s risk management objective and strategy for executing the hedge.

- The hedging relationship satisfies the hedge effectiveness requirements. This means:

– there’s an economic relationship between the hedged item and the hedging instrument, and

– the hedge ratio of the hedging relationship aligns with the quantity of the hedged item the entity actually hedges and the quantity of the hedging instrument used to hedge that quantity of the hedged item.

Too many IFRS updates? I know the feeling! That's why I created Reporting Period. It's a concise monthly summary of IFRS developments and Big 4 insights for accounting professionals. It's completely free, with zero spam, and you can unsubscribe anytime with one click. Interested? Leave your email below:

Hedging instruments

Qualifying instruments

The following are qualifying instruments, i.e. instruments that can be designated as hedging instruments (IFRS 9.6.2.1-2):

- Derivatives measured at FVTPL, except for most written options (refer to IFRS 9.B6.2.4), and

- Non-derivative financial assets or liabilities measured at FVTPL (excluding financial liabilities designated at FVTPL or assets measured at FVOCI).

A qualifying instrument must be designated in its entirety as a hedging instrument, barring the exceptions listed in paragraph IFRS 9.6.2.4 and discussed below.

Intrinsic value and time value of an option

Intrinsic value as a hedging instrument

IFRS 9 permits the alternative of designating either the full, or the intrinsic, value of an option as a hedging instrument (IFRS 9.6.2.4(a)). The time value of an option is often the sole component of a premium paid and is viewed by risk managers as a cost of hedging (IFRS 9.BC6.387). When only the intrinsic value of an option is designated as a hedging instrument, changes in the fair value of the time value of an option are recognised in OCI, and subsequent accounting depends on whether the hedged item is transaction-related or time-period related (IFRS 9.6.5.15).

Transaction-related hedged items

The time value of an option relates to a transaction-related hedged item if the nature of the hedged item is a transaction for which the time value has the character of the costs of that transaction. IFRS 9 provides an example of a commodity purchase where the initial measurement includes transaction costs (IFRS 9.B6.5.29(a)). Subsequent accounting for amounts accumulated in OCI is outlined in IFRS 9.6.5.15(b) and closely mirrors accounting for cash flow hedge reserves.

Example: Transaction-related hedged items

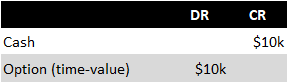

On 1 January, Entity A decides to purchase a piece of equipment, with the transaction expected to take place on 30 June of the same year. Entity A’s functional currency is the EUR, and the equipment will cost USD 300k. Entity A buys a call option for USD 300k to hedge the downside risk. The premium paid amounts to EUR 10k and represents the time value of the option. Entity A designates only the intrinsic value of the option as a hedging instrument in a cash flow hedge. The following entries illustrate the accounting for the time value of an option.

1. Entity A purchases the option on 1 January and pays a premium of EUR 10k:

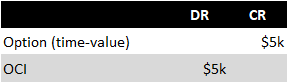

2. Entity A prepares financial statements on 31 March and recognises changes in the fair value of the time value of an option:

3. On 30 June, the fair value of the time value of the option falls to zero:

4. Entity A purchases the equipment for USD 300k, which, on the transaction date, equates to EUR 280k:

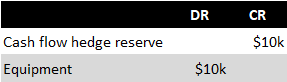

5. Entity A recognises the time value accumulated in OCI as a ‘basis adjustment’ that increases the cost of the equipment:

Time-period related hedged items

The time value of an option relates to a time-period related hedged item when the nature of the hedged item is such that the time value acts as a cost for obtaining protection against a particular risk over a specified period. IFRS 9 provides an example of a commodity inventory hedged against a fair value decrease for six months using a commodity option (IFRS 9.B6.5.29(b)). Any amounts accumulated in OCI should be subsequently amortised (as a reclassification adjustment) on a systematic and rational basis over the period during which the hedge adjustment for the option’s intrinsic value could affect profit or loss (IFRS 9.6.5.15(c)).

Example: Time-period related hedged items

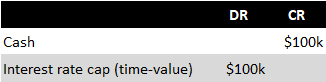

On 1 January 20X1, Entity A issues a 2-year floating rate bond and purchases an interest rate cap for the same period to safeguard itself from rising interest rates. The premium paid amounts to $100k. Only the intrinsic value of this cap is designated as a hedging instrument in a cash flow hedge. Entity A determines that a straight-line method offers a systematic and rational basis for amortising to P/L the time value of the interest rate cap. Accounting entries related to the time value of the interest rate cap are as follows:

1. Entity A purchases the interest rate cap on 1 January 20X1 and pays a premium of $100k:

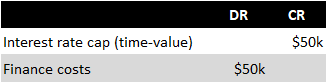

2. At 31 December 20X1, Entity A amortises to P/L the part relating to the first year:

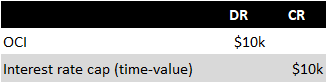

3. At 31 December 20X1, Entity A determines that the fair value of the time value of the interest rate cap amounts to $60k, thus it needs to be increased by $10k after considering the amortisation in point 2:

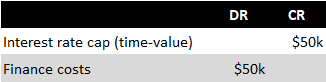

4. At 31 December 20X2, Entity A amortises to P/L the part relating to the second year:

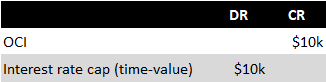

5. At 31 December 20X2, the fair value of the time value of the interest rate cap is nil, thus the entry at point 3 is reversed:

Aligned time value

The accounting for the time value of options, as mentioned above, applies only when the time value of the option and the hedged item are aligned. If the actual time value and the aligned time value differ, the provisions stated in IFRS 9.B6.5.33 apply.

Forward element and foreign currency basis spread of a forward contract

In a similar vein to the intrinsic value of an option, an entity can designate only the spot element of a forward contract as a hedging instrument according to IFRS 9.6.2.4(b). If this is the case, the general accounting requirements for the forward element and foreign currency basis spread are the same as for the intrinsic value of an option (IFRS 9.6.5.16, B6.5.34–B6.5.39).

Hedged items

Types of hedged items

Hedged items can be any of the following, as long as they are reliably measurable (IFRS 9.6.3.1-2):

- A recognised asset,

- A recognised liability,

- An unrecognised firm commitment,

- A highly probable forecast transaction (IFRS 9.6.3.3),

- Aggregated exposures,

- A net investment in a foreign operation.

Aggregated exposures

An aggregated exposure, consisting of a derivative and an exposure that could qualify as a hedged item under general rules, may be designated as a hedged item (IFRS 9.6.3.4). This is a significant change compared to IAS 39, which did not allow for derivatives to be designated as hedged items. Further discussion and examples can be found in paragraphs IFRS 9.B6.3.3-4 and in illustrative examples 16-18 accompanying IFRS 9.

Components of an item

IFRS 9.6.3.7 allows the designation of only a component of an item as a hedged item. The components include the following:

- Changes in the cash flows or fair value of an item due to a specific risk or risks (risk component).

- One or more selected contractual cash flows.

- Components of a nominal amount, i.e. a specified part of the amount of an item.

Risk components

A risk component of a financial or non-financial item must be separately identifiable and reliably measurable to qualify for designation as a hedged item. However, it does not have to be contractually specified. Further discussion and examples are provided in IFRS 9.B6.3.8-10. When a risk component is designated as a hedged item, the hedge accounting requirements apply to that risk component in the same way as they do to other hedged items (IFRS 9.B6.3.11). An entity can also designate changes in the cash flows or fair value of a hedged item above or below a specified price or other variable, referred to as a ‘one-sided risk’ (IFRS 9.B6.3.12).

Components of a nominal amount

Two types of nominal amount components can be designated as the hedged item (IFRS 9.B6.3.16):

- A proportion of an entire item (e.g. 50 per cent of the contractual cash flows of a loan), or

- A layer component (examples are provided in paragraph IFRS 9.B6.3.18).

Relationship between components and total cash flows

A component of the cash flows designated as the hedged item cannot exceed the total cash flows of the entire item. For further discussion and examples, refer to IFRS 9.B6.3.21-25.

Forecast transactions with owners

Forecast transactions with owners (e.g. share issuance, share buy-back, declaration of dividend) cannot be hedged items because such transactions will not impact P/L nor OCI, which is a necessary condition for a cash flow hedge (IFRS 9.6.5.2).

General business risks

General business risks cannot be hedged items as they cannot be specifically identified and measured (IFRS 9.B6.3.1). Examples of general business risks include the risk that a transaction will not occur or the obsolescence of a physical asset.

A firm commitment to acquire a business

A firm commitment to acquire a business in a business combination cannot be a hedged item, except for foreign currency risk. Risks other than foreign currency risk cannot be specifically identified and measured and are considered to be general business risks (IFRS 9.B6.3.1).

It may occur that the transactions of a business to be acquired qualify as a hedged item, provided they can be considered a highly probable forecast transaction from the perspective of the acquirer.

Meaning of highly probable

IFRS 9 does not provide guidance on what constitutes a ‘highly probable’ forecast transaction. IAS 39 did include such guidance, which can still be considered valid and can be found in IAS 39.F.3.7.

Hedges of a group of items

Under IFRS 9, a group of items, including a group that forms a net position, may qualify as an eligible hedged item, subject to the conditions in paragraph IFRS 9.6.6.1. More discussions on this can be found in IFRS 9.B6.6.1-6.

Components of a group

In a manner analogous to individual items, components within a group of items can also be designated as hedged items, provided they satisfy the criteria set out in IFRS 9.6.6.2-3.

Presentation

If a net position hedge impacts different line items in P/L or OCI, any hedging gains or losses should be presented in a line separate from those affected by the hedged items (IFRS 9.6.6.4).

Nil net positions

A nil net position arises when hedged items fully offset the risk managed on a group basis. Such a position can be designated in a hedging relationship that doesn’t include a hedging instrument if it meets the criteria in IFRS 9.6.6.6.

Formal designation and documentation

At the inception of the hedging relationship, a formal designation and documentation of the hedging relationship should be established, along with the entity’s risk management objective and strategy for undertaking the hedge. This documentation (IFRS 9.6.4.1(b)) should include:

- Identification of the hedging instrument,

- Identification of the hedged item,

- Description of the risk being hedged, and

- Explanation of how the entity will assess whether the hedging relationship meets the hedge effectiveness requirements (including its analysis of the sources of hedge ineffectiveness and how it determines the hedge ratio).

Hedge effectiveness

A key requirement for hedge effectiveness is an economic relationship between the hedged item and the hedging instrument. This means that their values generally move in opposite directions in response to the same risk (the hedged risk). This doesn’t require that the values of the hedging instrument and the hedged item must invariably move in opposing directions. Further discussion on this can be found in IFRS 9.B6.4.4-6; B6.4.14.

There’s no ‘bright line’ set or objective-based assessment indicating when a hedging relationship qualifies for hedge accounting in terms of its effectiveness, unlike the 80%-125% threshold present in IAS 39 (IFRS 9.BC6.238). Generally, it will be apparent that the hedging instrument and the hedged item values move in opposite directions and a qualitative assessment will suffice. However, in some cases where hedge effectiveness is more difficult to predict, a quantitative assessment may be necessary (IFRS 9.B6.4.13-16).

Entities must assess whether a hedging relationship meets the hedge effectiveness requirements at each reporting date or when there is a significant change in circumstances. This assessment is forward-looking, focusing on expectations about future hedge effectiveness (IFRS 9.B6.4.12).

Impact of credit risk on hedge effectiveness

Changes in credit risk can affect the fair value of a financial instrument, but it’s rare for there to be corresponding changes in credit risk for the hedged item and the hedging instrument, leading to some hedge ineffectiveness. Paragraph IFRS 9.6.4.1(c)(ii) dictates that credit risk shouldn’t ‘dominate’ the value fluctuations resulting from the economic relationship determined for the hedge effectiveness criterion. This condition is typically satisfied for the most common hedging instruments, as they’re contracted with reputable financial institutions and/or are cash collateralised. For hedged items, there’s a possibility that at some point, credit risk will ‘dominate’ their value changes. However, it’s widely accepted that transitioning to Stage 3 in the impairment model doesn’t imply that credit risk dominates the value changes of a financial asset. Refer to IFRS 9.B6.4.7-8 for a more in-depth discussion.

Measuring hedge ineffectiveness

As previously stated, hedge documentation should include a description of how the entity will evaluate whether the hedging relationship satisfies the hedge effectiveness requirements, as well as an analysis of the sources of hedge ineffectiveness and the method used to determine the hedge ratio. Hedge ineffectiveness refers to the degree to which changes in the fair value or cash flows of the hedging instrument exceed or fall short of those of the hedged item. Any ineffectiveness is immediately recognised in profit or loss (IFRS 9.B6.4.1).

Ratio analysis

While IFRS 9 doesn’t dictate how to measure hedge ineffectiveness, ratio analysis can be used in simpler arrangements. This method involves comparing hedging gains and losses with the corresponding gains and losses on the hedged item at a specific point in time, as explicitly mentioned in IAS 39.F.4.4.

‘Hypothetical derivative’ method

IFRS 9 references the ‘hypothetical derivative’ method as a potential way to measure hedge effectiveness in more complex situations. This technique compares the change in fair value or cash flows of the hedging instrument with the change in fair value or cash flows of a hypothetical derivative that represents the hedged risk. The ineffectiveness recognised in P/L is based on comparing the actual hedging instrument with the hypothetical derivative (IFRS 9.B6.5.5). An illustrative example is provided in IAS 39.F.5.5.

Hedge ratio of the hedging relationship

The hedge ratio represents the relationship between hedging instruments and hedged items. IFRS 9 mandates that the hedge ratio used for accounting purposes should match that used for risk management purposes (see IFRS 9.B6.4.9). Nonetheless, paragraph IFRS 9.6.4.1(c)(iii) includes anti-abuse rules to prevent this ratio from being set too low to circumvent recognising hedge ineffectiveness for cash flow hedges or to secure fair value hedge adjustments for more hedged items with the intention of increasing the use of fair value accounting (see IFRS 9.B6.4.11).

Three types of hedging relationships

There are three types of hedging relationships (IFRS 9.6.5.2):

Detailed discussions of these types are provided in the following sections. Furthermore, see this topic on our Forums for additional insights.

Fair value hedges

Definition of fair value hedge

A fair value hedge, as defined by IFRS 9.6.5.2(a), mitigates the risk of exposure to changes in the fair value of a recognised asset or liability or an unrecognised firm commitment (or a component of such items). This change in fair value must be attributable to a specific risk that could affect profit or loss. Examples of fair value hedges include:

- Interest rate swaps used to hedge exposure to fair value changes of fixed-rate debt (either by issuer or holder), irrespective of whether the debt instrument is accounted for at amortised cost (IFRS 9.B6.5.1, see also IAS 39.F.2.13).

- A forecasted purchase of an equity instrument, which will be accounted for at FVTPL or FVOCI once acquired.

- Hedges of exposure to changes in the fair value of variable rate debt due to credit risk or fluctuations in the market interest rate during the periods between variable interest rate resets (IAS 39.F.3.5).

- Hedges of foreign currency risk in a monetary asset or liability, which could also be treated as cash flow hedges (IAS 39.F.3.3‐4).

- Forward contracts for inventory to hedge exposure to price changes, despite them being measured at the lower of cost and net realisable value. This is because changes in the fair value of inventory will affect profit or loss when they are sold or their carrying amount is written down (IAS 39.F.3.6).

- Hedges of price risk or currency risk in a firm commitment to purchase inventory (IFRS 9.B6.5.3).

Accounting for fair value hedges

The accounting for fair value hedges (IFRS 9.6.5.8) can be summarised as follows:

- Hedging instruments are measured at fair value, with gains or losses recognised in P/L (or OCI if the hedged item is an equity instrument at FVOCI without recycling).

- The changes in the fair value of the risk being hedged are recognised in both the carrying value of the hedged item and in P/L (or OCI if the hedged item is an equity instrument at FVOCI without recycling).

- When a hedged item is an unrecognised firm commitment, the subsequent change in its fair value post its designation is recognised as an asset or a liability with corresponding gains or losses recognised in P/L. When the firm commitment turns into an asset or a liability, its carrying amount includes the amount recognised as a basis adjustment (IFRS 9.6.5.9).

- Any ineffectiveness is recognised in profit or loss.

The adjustment to the carrying value of a hedged item is often referred to as a ‘basis adjustment’.

Basis adjustment to debt instruments measured at amortised cost

Any basis adjustment made to the carrying amount of a debt instrument measured at amortised cost should be amortised to P/L as an adjustment to the effective interest rate (EIR). However, to alleviate the need for constant adjustments to the EIR, entities are permitted to begin amortisation when the hedged instrument ceases to be adjusted for hedging gains and losses (IFRS 9.6.5.10).

Cash flow hedges

Definition of cash flow hedge

A cash flow hedge is a strategy to offset exposure to variability in cash flows. This variability is attributed to a particular risk linked to:

- A recognised asset or liability,

- A highly probable forecast transaction, or

- A firm commitment (exclusive to foreign currency risk as per IFRS 9.6.5.4).

Such variability should have the potential to influence profit or loss, as stated in IFRS 9.6.5.2(b). The goal of a cash flow hedge is to defer the gain or loss on the hedging instrument to a future period(s) when the hedged cash flows affect profit or loss.

Examples of cash flow hedges include:

- Interest rate swaps used to convert floating-rate debt (regardless of whether it’s measured at amortised cost or fair value) into fixed-rate debt. In this case, the hedge of future cash flows would be the future interest payments (IFRS 9.B6.5.2).

- Hedges against interest rate risk in an upcoming debt issuance (IAS 39.F.2.2).

- Forward contracts for inventory to hedge against cash flow exposure arising from future inventory sales (IAS 39.F.3.6).

- Hedges of the foreign currency risk in a firm commitment (only this risk in a firm commitment can be classified as a cash flow hedge) (IFRS 9.6.5.4).

- Hedges of foreign currency risk in a monetary asset or liability, which can also be classified as fair value hedges (IAS 39.F.3.3‐4).

Accounting for cash flow hedges

The accounting procedures for cash flow hedges can be summarised as follows, as per IFRS 9.6.5.11:

- Changes in the fair value of hedging instruments are recognised in OCI and are accumulated in a cash flow hedge reserve within equity.

- The cash flow hedge reserve is the lesser of the two following measures:

– the cumulative gain or loss on the hedging instrument since the inception of the hedge, and

– the cumulative change in the fair value (present value) of the hedged expected future cash flows since the inception of the hedge. Over-hedge ineffectiveness is not accumulated in OCI. - As a result, over-hedge ineffectiveness is recognised in profit or loss, whereas under-hedge ineffectiveness is not recognised.

- For hedges other than those specified below, gains or losses accumulated in a cash flow hedge reserve are reclassified to P/L as a reclassification adjustment, often referred to as ‘recycling’ that should be disclosed under IAS 1.92. This reclassification occurs during the same period(s) in which the hedged expected future cash flows affect profit or loss. For example, this could be when interest income (or expense) or foreign exchange gain (or loss) is recognised, or when a forecast sale takes place (see IAS 39.F.3.3-4).

- For hedges of a forecast transaction resulting in the recognition of a non-financial asset or liability (e.g., inventory), or when a hedged forecast transaction for a non-financial asset or liability becomes a firm commitment for which fair value hedge accounting is applied, the gains or losses accumulated in a cash flow hedge reserve are directly included in the carrying amount of the asset or liability. This is not a reclassification adjustment and therefore doesn’t impact OCI (see also IFRS 9.BC6.380). This is often referred to as a ‘basis adjustment’. An example is provided below.

- Any accumulated loss on a hedging instrument that is not expected to be recovered should be immediately reclassified to P/L as a reclassification adjustment.

Example: Basis adjustment in a forecast acquisition of inventory

Entity A, which has EUR as its functional currency, contracts on 1 January for a purchase of inventory on 30 September for USD 1 million. Entity A decides to hedge the foreign currency exposure and enters into a forward contract with a bank to purchase USD 1 million for EUR 1 million. The forward contract is treated as a cash flow hedge. Entity A prepares its interim financial statements on 30 June when the forward contract has a positive fair value of EUR 0.1 million. On 30 September, the forward contract has a positive fair value of EUR 0.15 million. The accounting entries are as follows:

1. Impact of a change in fair value as at 30 June:

2. Change in fair value between 30 June and 30 September:

3. Settlement of a forward contract:

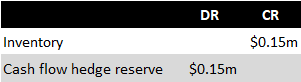

4. Purchase of inventory:

5. Recognition of basis adjustment:

The use of the cash flow hedge reserve in entry no. 5 is not treated as a reclassification adjustment and hence does not impact OCI (IFRS 9.6.5.11(d)(i); BC6.380). However, it does impact total equity, and therefore it should be included in the statement of changes in equity as a separate movement.

For additional insights, see this discussion on our Forums regarding presentation in OCI (items that will not be reclassified subsequently to profit or loss vs items that will be reclassified).

Hedges of a net investment in a foreign operation

Hedging a net investment in a foreign operation, as outlined in IFRS 9.6.5.13-14, operates similarly to a cash flow hedge. Further details are available in IFRIC 16.

Rebalancing

In IFRS 9, ‘rebalancing’ refers to the adjustments made to the hedged item or the hedging instrument within an existing hedging relationship. This is done to maintain a hedge ratio that complies with hedge effectiveness requirements. Accounting for rebalancing is considered a continuation of the hedging relationship, with immediate recognition of any hedge ineffectiveness. However, if the risk management objective for a hedging relationship changes, rebalancing provisions do not apply. Instead, hedge accounting for that hedging relationship should be discontinued. Additional discussion and examples can be found in IFRS 9.B6.5.7-21.

Discontinuing hedge accounting

Hedge accounting should be discontinued prospectively when the hedging relationship no longer meets the qualifying criteria. This discontinuation can also apply to a part of a hedging relationship. If a hedging instrument is replaced or rolled over into another instrument, it does not constitute an expiration or termination, provided this is in line with the entity’s documented risk management objective (IFRS 9.6.5.6). Further discussion and examples are provided in IFRS 9.B6.5.22-28.

Discontinuation of fair value hedge

When a fair value hedge is discontinued, the basis adjustment is amortised to P/L as per IFRS 9.6.5.10 (IFRS 9.6.5.7).

Discontinuation of cash flow hedge

Upon discontinuation of a cash flow hedge, the accounting procedure depends on whether the hedged cash flows are still expected to occur. If they are, the accumulated cash flow hedge reserve remains until the hedged cash flows occur. If they are no longer expected to occur, the amount accumulated in the cash flow hedge reserve is recycled to P/L as outlined in IFRS 9.6.5.12.

Intragroup transactions

Generally, intragroup items cannot be considered as hedged items in the consolidated financial statements (IFRS 9.6.3.5). However, an exception applies to the foreign currency risk of an intragroup monetary item (e.g. receivables and payables) if group entities have different functional currencies. This is because exchange rate gains and losses on such items affect the consolidated profit or loss.

Similarly, the foreign currency risk of a highly probable forecast intragroup transaction may qualify as a hedged item in consolidated financial statements, provided the transaction is denominated in a currency other than the functional currency of the entity entering into the transaction, and the foreign currency risk will affect the consolidated profit or loss (IFRS 9.6.3.6). More discussion can be found in IFRS 9.B6.3.5.

Hedged item and hedging instrument held by different group entities

For large corporations with centralised treasury functions, it’s common for one entity to contract a derivative to hedge a risk to which another group entity is exposed. IFRS 9 does not prohibit such arrangements from being accounted for using hedge accounting principles in consolidated financial statements. This practice was explicitly allowed in IAS 39 (IAS 39.F.2.14).

Presentation of gains or losses on hedging instruments

In the case where a group of hedged items does not possess any offsetting risk positions, the gains or losses from the hedging instrument are presented in the financial statement line items affected by the hedged items. If multiple lines are impacted, the allocation of gains or losses on the hedging instrument must be carried out systematically and rationally. Conversely, if the group of hedged items does contain offsetting risk positions (for example, the net position of forecast sales and expenses), the gains or losses on the hedging instrument are presented in a separate line item (IFRS 9.B6.6.13-16).

Risk management strategy and risk management objectives

Under IFRS 9, a clear distinction is made between risk management strategy and risk management objectives.

A risk management strategy, as outlined in IFRS 9.B6.5.24:

- Is established at the highest level where an entity determines how it manages its risk.

- Typically identifies the risks that the entity faces.

- Dictates how the entity responds to these risks.

In contrast, a risk management objective:

- Is established for a specific hedging relationship.

- Applies at the level of that particular hedging relationship.

- Is linked to how the specified hedging instrument is used to hedge the exposure designated as the hedged item.

The importance of this distinction is that certain hedge accounting eligibility is based on risk management strategy, which also needs to be disclosed in financial statements (IFRS 7.21A(a)).

Hedge accounting under IAS 39

IFRS 9.7.2.21 permits entities to continue applying hedge accounting as outlined in IAS 39. This will remain so until the IASB finalises its project for the so-called ‘macro hedging’, officially known as Dynamic Risk Management.

Disclosure

Disclosure requirements for hedge accounting are detailed in IFRS 7.21A-24G.

More about financial instruments

See other pages relating to financial instruments:

Scope of IAS 32

Financial Instruments: Definitions

Derivatives and Embedded Derivatives: Definitions and Characteristics

Classification of Financial Assets and Financial Liabilities

Measurement of Financial Instruments

Amortised Cost and Effective Interest Rate

Impairment of Financial Assets

Derecognition of Financial Assets

Derecognition of Financial Liabilities

Factoring

Interest-Free Loans or Loans at Below-Market Interest Rate

Offsetting of Financial Instruments

Hedge Accounting

Financial Liabilities vs Equity

IFRS 7 Financial Instruments: Disclosures