A lease modification refers to any change to the original terms of a lease agreement. This may include changes to the scope of the lease, its contractual duration, or the consideration involved. However, re-evaluations of the terms initially included in the lease contract do not constitute lease modifications. Instead, they are regarded as reassessments of the lease liability.

Depending on the specific circumstances, lease modifications can either be accounted for as a new lease or an adjustment to the pre-existing lease.

Let’s dive in.

Lease modification as a separate lease

Under IFRS 16.44, a lessee (customer) accounts for a lease modification as a separate lease if both of the following conditions are met:

- The modification increases the scope of the lease by granting the right to use one or more underlying assets; and

- The consideration for the lease increases proportionately with the stand-alone price for the increased scope, along with any necessary adjustments to reflect the specifics of the contract.

When treated as a separate lease, the original right-of-use asset remains unaffected, and the new lease is recognised following the general recognition principles. Example 15 accompanying IFRS 16 provides further detail.

Lease modification not accounted for as a separate lease

If a lease modification does not qualify as a separate lease (IFRS 16.45), the lessee:

- Allocates the consideration in the modified contract as when separating components of a contract.

- Determines the lease term of the modified lease; and

- Remeasures the lease liability by discounting the updated lease payments using a revised discount rate.

These steps are executed on the effective date of the lease modification, which is when both parties agree to the change in lease terms.

--Too many IFRS updates? I know the feeling! That's why I created Reporting Period. It's a concise monthly summary of IFRS developments and Big 4 insights for accounting professionals. It's completely free, with zero spam, and you can unsubscribe anytime with one click. Interested? Leave your email below:

Lease modifications that do not decrease the scope of a lease

When a lease modification does not reduce scope of the lease, the changes in lease liability have a corresponding effect on the right-of-use asset, with no one-off recognition in P/L (IFRS 16.46(b)).

For lease modifications that change the lease consideration, the adjustment to the right-of-use asset essentially represents a change in its cost resulting from the modification. Similarly, for modifications that increase the scope of the lease, the adjustment to the right-of-use asset represents the cost of the additional right of use obtained due to the modification.

As explained in IFRS 16.BC203, the use of a revised discount rate in remeasuring the lease liability signifies a change in the lease’s implicit interest rate on its modification.

An Excel example based on Example 19 from IFRS 16 follows. Example 16, which details a modification that extends the lease term, is also a helpful resource.

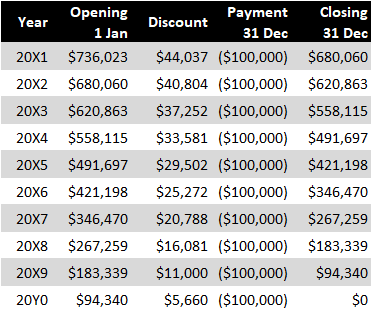

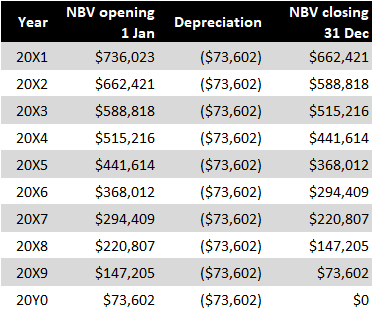

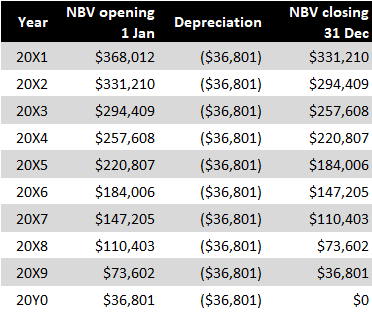

Entity A signs a 10-year lease for 2,000 square metres of office space with annual lease payments of $100,000, payable at the end of each year. The lease starts on 1 January 20X1, with a discount rate of 6%. The initial lease liability and right-of-use asset amount to $736,023. All calculations used in this example can be downloaded in an Excel file.

The accounting schedules for the lease liability and right-of-use asset before the lease modification are as follows:

Lease liability:

Right-of-use asset:

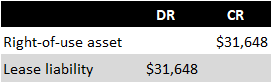

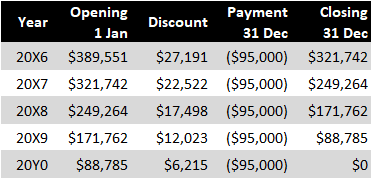

Let’s suppose that on 1 January 20X6, both parties agree to modify a lease, reducing the annual lease payments to $95,000. The lease term and scope remain the same. Entity A determines that the discount rate at the modification date increases to 7%.

Entity A recalculates to $389,551 the present value of the lease liability by discounting the revised lease payments for years 20X6 – 20Y0 using the revised discount rate. Given that the revised amount is less than the lease liability prior to the modification ($421,198), the difference is accounted for as follows:

The accounting for the lease liability and right-of-use asset in the years post-modification will be as follows:

Lease liability:

Right-of-use asset:

Please note, this example is based on illustrative Example 19 accompanying IFRS 16.

Decrease in the scope of a lease

Under IFRS 16.46(a), when a lease modification results in a reduction in the scope of a lease:

- Both the right-of-use asset and lease liability are reduced to account for a partial or full termination of the lease, and

- Any gain or loss arising from this derecognition is immediately recognised in profit or loss.

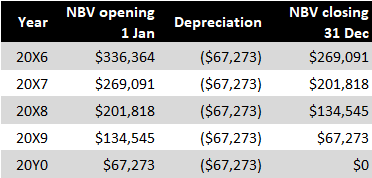

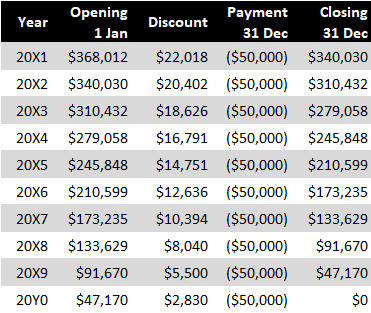

Consider the scenario where Entity A has a 10-year lease agreement for 5,000 square metres of office space. The annual lease payments are $50,000, paid at the end of each year. The lease commences on 1 January 20X1 with a 6% discount rate, resulting in a present value of the lease liability amounting to $368,012. Since there were no payments at the lease’s commencement, the initial lease liability and the right-of-use asset are the same. All calculations for this example can be downloaded in an Excel file.

Subsequent accounting for the lease liability and right-of-use asset is displayed below.

The lease liability increases annually due to the unwinding of the discount (charged as finance costs in P/L), and decreases with each payment:

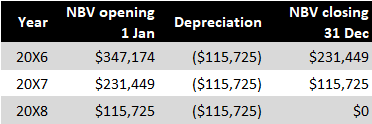

The carrying amount of the right-of-use asset reduces each year due to charged depreciation:

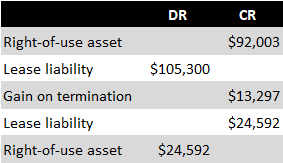

Suppose that on 1 January 20X6, a lease modification reduces the lease scope by 50%. Therefore, Entity A now leases only 2,500 square metres out of the original 5,000 square metres. The annual payment also decreases from $50,000 to $30,000, and the discount rate is revised to 5% at the modification date. Entity A calculates a gain in P/L as follows:

- Scope modified by: 50% (2,500 sq m out of original 5,000 sq m)

- Right-of-use asset before modification: $184,006

- Reduction of right-of-use asset by 50%: $92,003

- Right-of-use asset after scope reduction: $92,003

- Lease liability before modification: $210,599

- Reduction of liability by 50%: $105,300

- Liability after scope reduction: $105,300

Based on the calculations above, Entity A recognises $13,297 ($105,300 – $92,003) as a gain on terminating the lease under the old terms (immediately recognised in P/L).

On the date of modification, Entity A determines the lease liability’s present value to be $129,892, based on annual payments of $30,000 and a revised discount rate of 5%.

Entity A records the following accounting entries on the lease modification date:

Note: This example is based on Illustrative Example 17 accompanying IFRS 16.

Example: Lease modification – both increase and decrease in scope

In this example, Entity A initiates a 10-year lease for office space. The original assumptions, calculations, and inception of the lease liability and right-of-use asset at $736,023 are identical to those in the prior example. All related calculations for this example can be accessed in the downloadable Excel file.

Suppose a lease modification is made on 1 January 20X6, involving the following changes:

- The lease scope is increased by an additional 1,500 square metres.

- The lease term is reduced from 10 to 8 years.

- The annual payments are increased to $150,000.

The revised discount rate at the lease modification date is 7%.

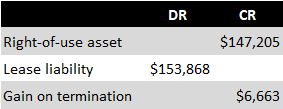

Entity A concludes that the increase of the lease scope doesn’t satisfy the criteria in IFRS 16.44, thus it is not accounted for as a separate lease. Consequently, on the modification date, Entity A calculates the gain on the termination of the lease of 2,000 square metres under old terms for years 9 and 10 as follows:

- Right-of-use asset before modification: $368,012

- Modified (remaining) scope: 60% (3 out of 5 remaining years)

- Decrease of right-of-use asset by 40%: $147,205

- Right-of-use asset after scope reduction (remaining 60%): $220,807

- Liability before modification: $421,198

- Remaining liability related to the modified scope (at original discount rate): $267,330

- Decrease of liability: $153,868

As a result, Entity A recognises a gain of $6,663 ($153,868 – $147,205) on the termination of the lease under the previous terms, which is immediately recognised in P/L.

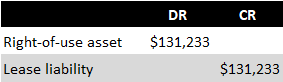

Next, Entity A calculates the lease liability and the right-of-use asset corresponding to the extra 1,500 square metres, amounting to $131,233. This is done by discounting the additional annual payments of $50,000 at 7%. This sum is added to the value of the right-of-use asset (all accounting entries are summarised at the end of this example).

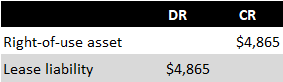

As a final step, Entity A determines the impact of the revised discount rate on the portion of the lease liability that reflects the annual payments of $100,000 for the years 20X6-20X8. The liability discounted at the original rate of 6% ($267,330) is compared to the amount discounted at 7% ($262,465). The difference of $4,865 is subtracted from both the right-of-use asset and lease liability.

In summary, Entity A makes the following accounting entries at the modification date:

1. Gain on the termination of the lease of 2,000 sq metres for years 9 and 10, with immediate recognition in P/L:

2. Impact of revised discount rate for years 6-8 on the lease of 2,000 sq metres:

3. Impact of increased leased space (an additional 1,500 sq metres):

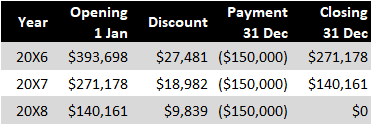

Accounting for the lease liability and right-of-use asset in the subsequent years following the modification is as follows:

Lease liability:

Right-of-use asset:

Note: This example is modelled after Illustrative Example 18 accompanying IFRS 16.

More about IFRS 16

See other pages relating to IFRS 16: