Lessors are required to classify each of their leases as either an operating lease or a finance lease. This classification is fundamental in lessor accounting, given that the accounting requirements considerably differ between these two lease types.

In the case of finance leases, the lessor derecognises the leased asset from its statement of financial position. Instead, it recognises a lease receivable equivalent to the net investment in the lease. Following this, the lessor recognises interest income on this receivable, with the lease payments made by the lessee reducing the outstanding balance.

On the other hand, assets leased through an operating lease remain on the lessor’s statement of financial position and continue to be depreciated according to the customary depreciation policy. Payments received from operating leases are usually recognised as income on a straight-line basis.

Let’s dive in.

Classification of leases

Finance lease vs operating lease

In accordance with IFRS 16.61, a lessor should classify each of its leases as either a finance lease or an operating lease. Leases that transfer substantially all of the risks and rewards incidental to ownership of the underlying asset are finance leases, and all other leases are operating leases.

Risks might involve potential losses from idle capacity or technological obsolescence, and fluctuations in returns due to changing economic conditions. Rewards, on the other hand, might be associated with the expectation of profitable operation throughout the asset’s economic life, and the potential gain from an increase in value or the realisation of a residual value (IFRS 16.B53).

Paragraphs IFRS 16.63-65 provide examples and indicators that, either individually or collectively, could typically lead to a lease being classified as a finance lease. These criteria are explored further below. It’s important to note that lessees, in contrast to lessors, do not distinguish between operating and finance leases, as they adopt a uniform ‘right-of-use‘ accounting model for all leases.

- Transfer of ownership and purchase options: A lease qualifies as a finance lease if it results in the lessee acquiring legal ownership of the asset, either during or at the conclusion of the lease term. Similarly, a lease offering the lessee a purchase option for the asset at a significantly reduced price compared to its expected fair value is also considered a finance lease.

- Lease term and asset’s economic life: If the lease term covers the ‘major part’ of the asset’s economic life it’s classified as a finance lease. Notably, IFRS 16 does not specify what constitutes the ‘major part’ of an asset’s economic life. Under certain GAAP, a 75% quantitative benchmark is often used for this evaluation.

- Present value of lease payments: A contract is a finance lease if the present value of the lease payments is equivalent to almost all the fair value of the underlying asset. IFRS 16 does not define a specific threshold, but a 90% benchmark, commonly used in more rule-based GAAP, can be a practical reference. This calculation must include any residual value guarantees provided by the lessee or related parties.

- Specialised nature of the asset: If the asset is so specialised that it requires significant modification for use by anyone other than the lessee, the lease should be classified as a finance lease. This typically applies to assets tailored to the lessee’s specifications or those integral to the lessee’s operations.

Too many IFRS updates? I know the feeling! That's why I created Reporting Period. It's a concise monthly summary of IFRS developments and Big 4 insights for accounting professionals. It's completely free, with zero spam, and you can unsubscribe anytime with one click. Interested? Leave your email below:

Lease of land and buildings

When a lease involves both land and buildings, the lessor should independently evaluate the classification of each component as either a finance lease or an operating lease. Lease payments must be allocated between the land and buildings components, reflecting the relative fair values of the leasehold interests in the land and buildings at the inception of the lease.

The fair value of a leasehold interest can be defined as the underlying asset’s fair value minus its present residual value. The IASB argues that allocation based on the leasehold interests’ fair values provides a more accurate reflection of compensating the lessor for the benefits depleted during the lease term (IFRS 16.BCZ245-BCZ247).

IFRS 16 highlights that land typically has an indefinite economic life (IFRS 16.B55-B57). Consequently, it’s implausible that the lease term will cover the majority of the economic life of the underlying land. However, for extremely long-term leases (e.g., 99 years), the present value of the lease payments could represent substantially all of the fair value of the land.

If the value of the land component is immaterial to a lease of land and buildings, the lessor may consider the land and buildings as a single unit for lease classification purposes (IFRS 16.B57).

Subleases

A sublease represents a transaction in which a lessee, referred to as an ‘intermediate lessor’, leases out the original leased asset to a third party. During this transaction, the initial lease agreement, known as the ‘head lease’, between the original lessor and the lessee remains in effect (IFRS 16 Appendix A).

The intermediate lessor accounts for the head lease and the sub-lease as two different contracts, applying both the lessee and the lessor accounting requirements. The intermediate lessor is thus required to classify the sublease as either a finance lease or an operating lease based on the following criteria as stated in IFRS 16.B58:

- If the head lease is a short-term lease that the entity, acting as the lessee, has used the relevant practical expedient, then the sublease is classified as an operating lease,

- In any other case, the sublease is classified in relation to the right-of-use asset arising from the head lease, rather than the underlying asset itself.

It is important to note that if a lessee subleases an asset, or plans to do so, the head lease cannot be categorised as a lease of a low-value asset according to IFRS 16.B7.

For more information, refer to Examples 20-21 accompanying IFRS 16 and the discussion in paragraphs IFRS 16.BC232-BC236.

Reassessment of lease classification

The reclassification of a lease takes place only in the event of a lease modification. Changes in estimates or circumstances cannot lead to a new classification of a lease according to IFRS 16.66.

Finance leases: initial recognition and measurement

Summary of initial recognition and measurement

At the commencement of a finance lease, the lessor recognises a lease receivable that equates to the net investment in the lease (IFRS 16.67). The net investment in the lease comprises of the following components, discounted at the interest rate implicit in the lease:

- Lease payments receivable by a lessor, and

- Any unguaranteed residual value accruing to the lessor.

Initial direct costs are included in the net investment in the lease, with the exception of manufacturers or dealer lessors.

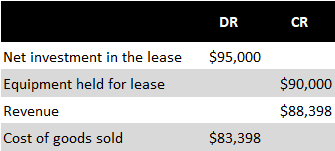

The underlying asset is derecognised and any resulting difference is immediately recognised in P/L as a gain or loss on the disposal of an asset. However, manufacturer and dealer lessors recognise revenue and costs of goods sold.

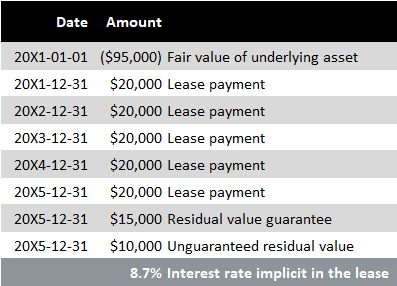

On 1 January 20X1, Entity A (a dealer-lessor) agrees to a five-year equipment lease contract with Entity X (a lessee). The relevant details of this lease are as follows:

- Annual lease payments of $20,000 are made at the end of each year,

- Entity A determines the equipment’s carrying amount at $90,000 and assesses its fair value at $95,000, and

- Entity A estimates the residual value of the equipment at $25,000, of which $15,000 is guaranteed by Entity X.

All calculations for this example are downloadable in an Excel file.

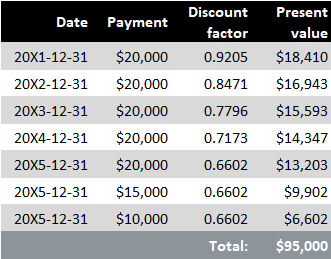

Initially, Entity A determines the implicit interest rate in the lease as follows:

Using the implicit interest rate, Entity A calculates the present values of lease payments and residual value:

At the commencement of the lease, Entity A makes the following accounting entries:

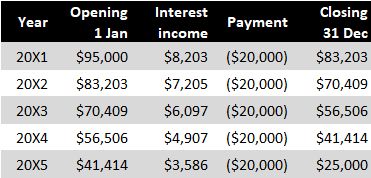

Each year, the net investment in the lease will increase due to the recognition of interest income in P\L and will decrease due to the lessee’s payments, as follows:

The remaining $25,000 on 31 December 20X5 is the equipment’s residual value.

Lease payments

The lease payments included in the measurement of the net investment in the lease are outlined in paragraph IFRS 16.70. They generally mirror those included in the lessee’s measurement of lease liability:

- Fixed payments (including in-substance fixed payments),

- Variable lease payments that depend on an index or a rate,

- Residual value guarantees provided to the lessor by the lessee,

- Exercise price of a purchase option, if the lessee is reasonably certain to exercise that option, and

- Payments of penalties for terminating the lease, if the lease term reflects the lessee exercising an option to terminate the lease.

Unguaranteed residual value accruing to the lessor

Unguaranteed residual value accruing to the lessor represents the sum that the lessor expects to recover from the value of the underlying asset at the lease’s conclusion. This value is not assured or guaranteed by any unrelated third parties. This amount is excluded from the lease payments but is factored into the net investment in the lease. Factors such as the leased asset’s nature, its susceptibility to technological obsolescence, and the market demand for used items influence the unguaranteed residual value. See the subsequent measurement of unguaranteed residual value for more information.

Interest rate implicit in the lease

Interest rate implicit in the lease is explained in the lessee accounting section. As noted below, initial direct costs are added to the initial net investment in the lease and the definition of implicit interest rate takes this into account (IFRS 16.69).

Initial direct costs

Initial direct costs are incremental costs of obtaining a lease that would not have been incurred had the lease not been obtained. The definition of initial direct costs for lessors mirrors that for lessees and is discussed in the lessee accounting section. Initial direct costs are factored into the initial net investment in the lease and thus reduce the amount of income recognised over the lease term as explained in IFRS 16.69. However, this does not apply to manufacturer or dealer lessors.

Separating components of a contract by a lessor

Lessors should allocate the consideration in a contract to all lease and non-lease components using criteria for allocating the transaction price to performance obligations outlined in IFRS 15.

Finance leases: manufacturer or dealer lessors

Accounting summary for manufacturer or dealer lessors

Manufacturers or dealers frequently provide customers with the option of either purchasing or leasing an asset. Essentially, a finance lease of an asset by a manufacturer or dealer lessor corresponds to the profit or loss arising from an outright sale of the underlying asset (IFRS 16.72). Hence, a manufacturer or dealer lessor recognises at the commencement date (IFRS 16.71):

- Revenue that is equivalent to the fair value of the underlying asset or, if lesser, the present value of the lease payments accruing to the lessor, discounted using a market rate of interest,

- Cost of sale that matches the cost, or carrying amount if different, of the underlying asset minus the present value of the unguaranteed residual value, and

- Selling profit or loss (the difference between revenue and the cost of sale), following its policy for outright sales, where IFRS 15 is applicable.

Market rate of interest

As previously highlighted, the present value of lease payments accruing to the lessor should be discounted at the market rate of interest, not the interest rate stated by the lessor in a lease contract.

Costs of obtaining a lease

At the commencement date, a manufacturer or dealer lessor recognises costs associated with obtaining a finance lease as an expense, as they are primarily associated with earning recognised selling profit. These costs are excluded from the net investment in the lease (IFRS 16.74). This approach differs from that of non-manufacturer/dealer lessors.

Finance leases: subsequent measurement

Finance income

The lessor recognises finance income over the lease term using the effective interest rate (IFRS 16.75). See this example.

Lease payments

The lessor decreases the net investment in the lease for received payments. Variable lease payments that aren’t included in the measurement of the net investment in the lease are recognised in P/L as they are earned. More discussion on variable lease payments can be found in lessee accounting.

Derecognition and impairment

The net investment in the lease is subject to derecognition and impairment requirements set out in IFRS 9 (IFRS 16.77).

Unguaranteed residual value

The estimated unguaranteed residual value should be reviewed ‘regularly’. Any reduction in this value reduces interest income recognised over the remaining lease term and is immediately recognised as an adjustment to the net investment value with a corresponding one-off impact in P/L (IFRS 16.77).

Revisions to lease term

The lessor only revises the lease term and remeasures the net investment in the lease when there’s a change in the non-cancellable period of a lease (IFRS 16.21). This can occur when an option previously not included in the lessor’s determination of the lease term is exercised, or when an option earlier included is not exercised. However, IFRS 16 does not specify the accounting treatment for the resulting remeasurement of the net investment in the lease. Hence, lessors must establish an accounting policy under IAS 8.10-12 and apply, for instance, IFRS 9 requirements for changes in expected cash flows.

Lease modifications

In the event of a lease modification, the lessor should determine whether such a modification should be accounted for as a separate lease. Criteria for such assessment are provided in paragraph IFRS 16.79 and are identical to those for lessees.

A modification not treated as a separate lease is accounted for as follows (IFRS 16.80):

(a) If the lease would have been classified as an operating lease had the modification been in effect at the inception date, the lessor:

(i) accounts for the lease modification as a new lease from the effective date of the modification, and

(ii) measures the carrying amount of the underlying asset as the net investment in the lease immediately before the effective date of the lease modification.

(b) Otherwise, the lessor applies the requirements of IFRS 9.

Operating leases

Presentation

When a lease is classified as an operating lease, the underlying asset remains in the lessor’s statement of financial position and is presented according to its nature (IFRS 16.88).

Lease income

As per IFRS 16.81, a lessor recognises payments from operating leases as income on a straight-line basis. However, a different systematic approach can be used if it is more representative of the manner in which the benefit from the use of the underlying asset diminishes.

Initial direct costs

IFRS 16.83 stipulates that initial direct costs incurred in obtaining an operating lease are to be added to the carrying amount of the underlying asset. These costs are then recognised in P/L over the lease term on the same basis as the lease income.

Depreciation

The underlying asset subject to an operating lease is depreciated according to the lessor’s standard depreciation policy for similar assets (IFRS 16.84). In other words, either IAS 16 or IAS 38 should be applied.

Manufacturer or dealer lessor

In contrast to finance leases, manufacturer or dealer lessors do not recognise any selling profit upon entering an operating lease, as it is not considered equivalent to a sale (IFRS 16.86).

Lease modifications

If a lease is modified, the lessor accounts for it as a new lease from the date the modification takes effect. Any prepaid or accrued lease payments relating to the original lease are considered part of the lease payments for the new lease (IFRS 16.87).

Disclosure

The disclosure requirements for lessors are detailed in paragraphs IFRS 16.89-97.

More about IFRS 16

See other pages relating to IFRS 16: