A sale and leaseback transaction occurs when a company sells an asset, often an item of PP&E, to a third party and then leases it back immediately. This arrangement allows the selling company to continue using the asset whilst freeing up capital and improving liquidity.

The accounting treatment for such transactions depends on whether a genuine sale has taken place. If the buyer-lessor has not gained control over the asset (indicating no sale has taken place), the supposed sale and leaseback is viewed as a financing arrangement, with the underlying asset acting as collateral. This assessment is based on the IFRS 15 criteria, with the ensuing accounting requirements outlined in the table below:

Let’s dive in.

Identifying a sale

According to IFRS 16.99, entities apply IFRS 15 to establish if the transfer to the buyer-lessor qualifies as a sale. This essentially depends on whether the buyer-lessor has obtained control over the asset. For instance, substantive repurchase options for the seller or certain buyer-held put options might mean the transaction isn’t a sale. Both parties should apply the same criteria and, ideally, should reach identical conclusions.

Additionally, as described in IFRS 16.B45-B47, if the lessee hasn’t gained control of the underlying asset before it’s transferred to the lessor, it’s a standard lease, not a sale and leaseback. Entities must refer to IFRS 15 to determine control, since IFRS 16 doesn’t offer a specific definition for leases. However, IFRS 16 highlights that just obtaining a legal title by the potential seller-lessee before transfer doesn’t necessarily mean they controlled the asset. This assessment becomes crucial in cases like:

- When an asset is acquired from a manufacturer or dealer by a would-be seller-lessee and then quickly sold to the lessor.

- Transactions that involve highly specialised or bespoke assets.

Too many IFRS updates? I know the feeling! That's why I created Reporting Period. It's a concise monthly summary of IFRS developments and Big 4 insights for accounting professionals. It's completely free, with zero spam, and you can unsubscribe anytime with one click. Interested? Leave your email below:

Transfers qualifying as a sale

IFRS 16.100 details the accounting approach for asset transfers qualifying as a sale:

Seller-lessees:

- Measure the RoU asset at the proportion of the previous carrying amount of the asset that relates to the retained right of use.

- Recognise a gain or loss related only to the rights transferred to the buyer-lessor (see IFRS 16.BC266-BC267).

Buyer-lessors:

- Account for the asset’s purchase as per relevant IFRSs (often IAS 16).

- Follow IFRS 16’s lessor accounting requirements.

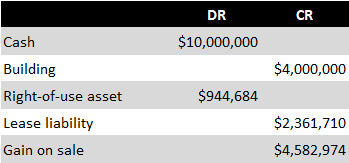

Entity D owns an office building with a carrying amount of $4,000,000. Seeking to boost liquidity, management sells the building to a Lessor for its fair value of $10,000,000. D then leases the building back for 10 years at an annual market rent of $280,000. D’s incremental borrowing rate stands at 4%.

Using calculations provided in this Excel file, D determines the present value of the lease payments to be $2,361,710 and measures the RoU asset at $944,684. This is based on the building’s previous carrying amount proportionate to the retained right of use. Only the gain arising on the rights transferred to the buyer-lessor is recognised in profit or loss. Thus, Entity D’s accounting entries at transaction date were:

The buyer-lessor recognises the building as an asset under IAS 16 (DR PP&E / CR Cash) and applies the IFRS 16 lessor accounting requirements.

Adjustments for off-market terms

Lease payments and the sale price in a sale and leaseback are often jointly negotiated, as highlighted in IFRS 16.BC267. Hence, the sale price might exceed the asset’s fair value, which is then offset by above-market leaseback rentals. Alternatively, a sale price below fair value could be paired with below-market leaseback rentals. As per IFRS 16.101, when the consideration for the sale of an asset differs from its fair value, or the lease payments aren’t at market rates, an entity should:

- Recognise the sale proceeds at fair value;

- Treat below-market terms as a prepayment of lease payments;

- Consider above-market terms as additional financing from the buyer-lessor.

IFRS 16.102 states that entities should measure these adjustments based on the more readily determinable difference between:

- The sale consideration’s fair value and the asset’s fair value; or

- The contractual lease payments’ present value and their market rates’ present value.

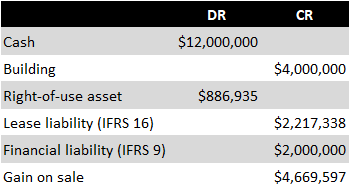

To illustrate, let’s modify the previous example. Assume Entity D sells the building for $12,000,000, which is $2,000,000 above its fair value. To balance this, the parties agree to a higher lease payment of $500,000 annually. A new Excel file provides calculations for this scenario.

The present value of future annual payments totals $4,217,338, determined by using D’s incremental borrowing rate. Out of this, the $2,000,000 difference between the sales proceeds and the building’s fair value is treated as additional financing from the buyer-lessor. This is recognised as a financial liability at amortised cost under IFRS 9. The remaining $2,217,338 is recognised as a lease liability. Apart from the non-lease part, the RoU asset and lease liability measurement methods remain consistent with the previous example.

Entity D’s accounting entries are:

The annual payment of $500,000 is allocated between the lease liability and the IFRS 9 financial liability. This allocation can be done using a goal seek function as shown in the Excel file.

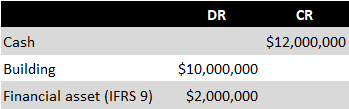

Like Entity D, the buyer-lessor recognises the additional financing it provided to D separately:

Variable lease payments

Recent amendments to IFRS 16, effective from 2024, aim to ensure the seller-lessee doesn’t recognise any gains relating to the retained right-of-use asset after a sale and leaseback transaction (refer to IFRS 16.BC267ZA-F). IASB has introduced a new example (no. 25) in IFRS 16 which demonstrates different methods to determine the proportion of the asset transferred to the buyer-lessor that relates to the retained right of use. This could be, for instance, comparing the retained space against the total area transferred. Additionally, this example shows how a seller-lessee might develop an accounting policy for variable lease payments not based on an index or rate, ensuring no gains related to retained right of use are recognised.

A new paragraph, IFRS 16.102A, underscores that subsequent lease liability measurements should not result in recognising gains or losses linked to the retained right of use.

Transfers not qualifying as a sale

If an asset transfer doesn’t qualify as a sale under IFRS 15, it’s considered solely a financing transaction. Both the seller-lessee and buyer-lessor recognise a financial liability and a financial asset under IFRS 9, respectively. The underlying asset remains in the seller-lessee’s statement of financial position as though no sale took place. IFRS 16.103 clarifies that the initial recognition amount matches the transfer proceeds, regardless of the asset and liability’s fair value. This is an exception to standard IFRS 9 initial recognition requirements.

For resulting financial assets or liabilities classified at amortised cost, IFRS 16 doesn’t set a specific approach for determining expected future cash flows. Hence, general amortised cost guidelines should be followed.

More about IFRS 16

See other pages relating to IFRS 16: