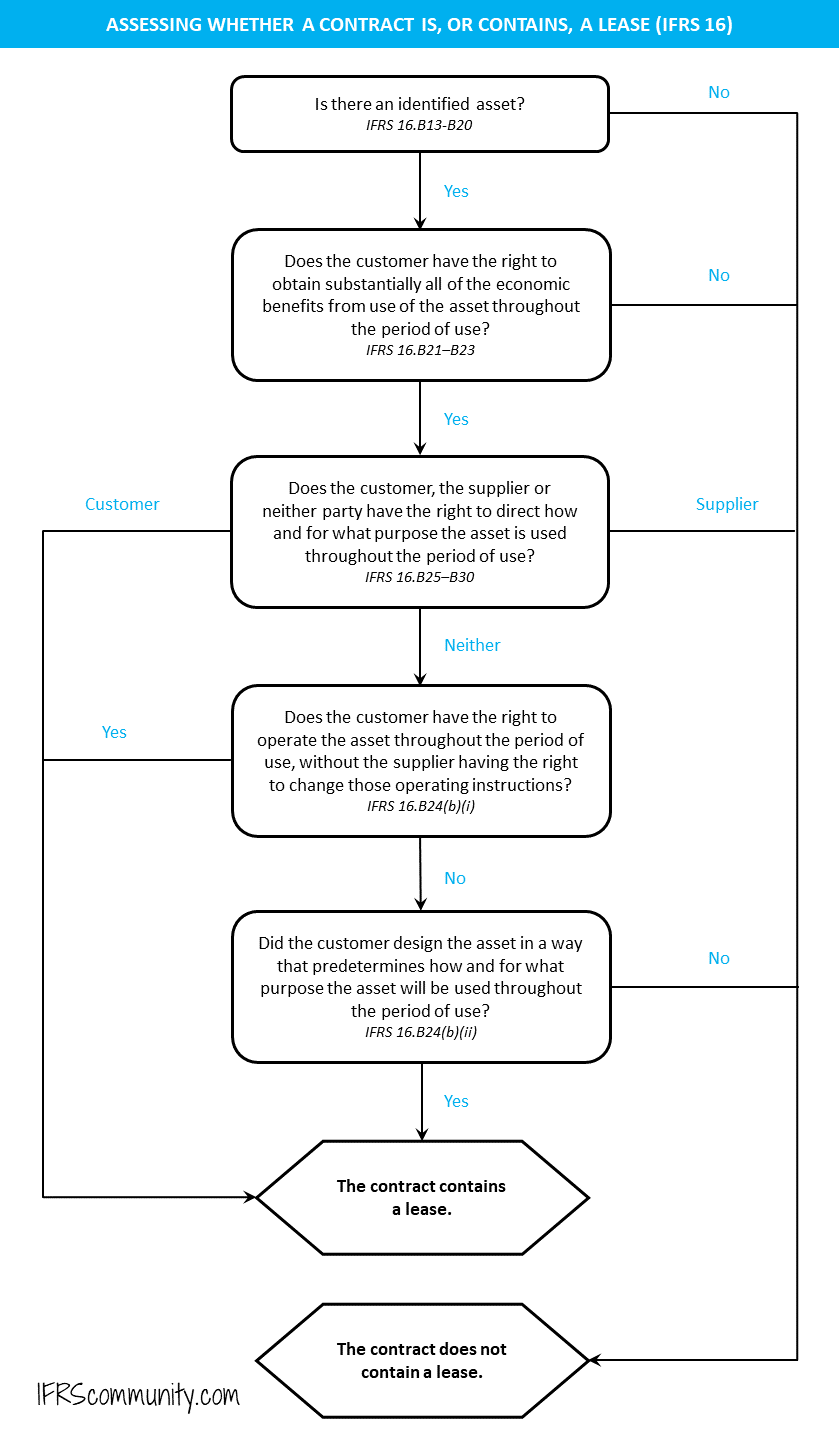

Determining if a contract is, or contains, a lease can usually be straightforward. However, in several instances, one may need to exercise judgement. As per IFRS 16.9, a contract qualifies as a lease if it grants the right to control the use of an identified asset (‘underlying asset’) for a period of time in exchange for consideration.

This right of control over an identified asset consists of:

- The right to obtain substantially all economic benefits from the asset’s use, and

- The right to direct its use.

The necessary steps for this assessment, to be conducted at the inception of the contract, are detailed in IFRS 16.B31. They are presented through a decision tree, as illustrated below. Examples 1-10 accompanying IFRS 16 illustrate the application of these criteria.

Let’s dive in.

--Too many IFRS updates? I know the feeling! That's why I created Reporting Period. It's a concise monthly summary of IFRS developments and Big 4 insights for accounting professionals. It's completely free, with zero spam, and you can unsubscribe anytime with one click. Interested? Leave your email below:

Identified asset

Definition

An asset is typically identified either by being expressly stated in a contract or implicitly when it becomes available for use. Thus, a lessee doesn’t need to know an asset’s exact serial number to consider it ‘identified’ (IFRS 16.B13; BC111).

Portions of assets

An identified asset can be a physically distinct part of a larger asset. For instance, IFRS 16 cites a building floor as a potential identified asset. Subsurface rights can also qualify. However, if a portion isn’t physically distinct (like 30% of a pipeline’s capacity), it’s only regarded as an identified asset if it covers almost the entire capacity of that asset (IFRS 16.B20). If not, the contract isn’t a lease. See also Example 2 in IFRS 16.

Substitution rights

If the lessor has substitution rights, then the lessee doesn’t control the asset’s use, since the asset can be replaced. Thus, contracts with substitution rights don’t qualify as leases. However, such rights must be substantive, meaning they’re practical and economically beneficial. Substitution rights that don’t change the substance or character of the contract, mainly if the supplier is unlikely to act on those rights, should not affect the lease assessment. Thus, the assessment if a supplier’s substitution rights are substantive should exclude unlikely future events. For an in-depth discussion on substitution rights, refer to IFRS 16.B14-B19, BC112-BC115, and Example 4 accompanying IFRS 16.

Right to obtain substantially all of the economic benefits

To control the use of an asset, a lessee must have the right to obtain substantially all of the economic benefits from use of the asset during the usage period. In making this evaluation, it is essential to consider the benefits within the confines of the customer’s usage rights as defined in the contract. For instance, if a contract restricts the usage of a motor vehicle to a specific territory, the entity must only account for the economic benefits derived within that particular territory. Similarly, if there’s a mileage limit set on the vehicle’s use, the assessment should be confined to the economic gains achievable within that mileage limit, disregarding any potential benefits beyond it. Furthermore, the presence of a payment obligation, such as a customer paying a percentage of sales to the supplier for the use of retail space, does not restrain the customer’s right to obtain most of the economic benefits from that space. (IFRS 16.B21-B23).

Lessees should centre their attention on the economic benefits derived from using the asset, like providing services to customers, rather than from its ownership, such as tax benefits (IFRS 16.BC118).

Right to direct the use

A customer has the right to direct the use of an identified asset throughout its usage period if, according to IFRS 16.B24:

- The customer has the right to direct how and for what purpose the asset is used; or

- The relevant decisions about how and for what purpose the asset is used are predetermined.

How and for what purpose the asset is used

To judge whether a lessee possesses the right to direct how and for what purpose the asset is used, the emphasis is on decision-making rights that affect the economic benefits derived from the asset’s use (IFRS 16.B25). IFRS 16.B26 offers examples of such rights:

- The choice to modify the asset’s output type (e.g., choosing a container’s purpose – either for transport or storage, or selecting the product variety in a retail space).

- The decision of when the output is generated (e.g., scheduling the operation time for machinery or a power plant).

- The choice of the output’s location (e.g., setting a vehicle or ship’s destination, or selecting an equipment’s location).

- Determining if the output is generated and its amount (e.g., deciding on energy production from a power plant and its quantity).

However, decision-making rights restricted to merely operating or maintaining the asset don’t grant control over its use (IFRS 16.B27).

Predetermined decisions

As mentioned, a customer can direct an identified asset’s use if decisions about its usage and purpose are predetermined and either (IFRS 16.B24(b)):

- The customer can operate the asset during its usage period, or

- The customer has influenced the asset’s design, thereby determining its use.

Protective rights

A lessor’s protective rights typically don’t hinder a lessee’s ability to direct an asset’s use. Designed primarily to safeguard the lessor’s interest in the asset or ensure compliance with laws, protective rights, as explained in IFRS 16.B30, might:

- Set a cap on the asset’s usage or restrict its operation times and places,

- Mandate specific operating protocols, or

- Require the customer to notify the supplier of any changes in the asset’s use.

Usage duration

The usage duration might also be defined by the extent to which an identified asset is used, like the mileage of a car or the production output of a machine (IFRS 16.10).

Distinguishing between lease and purchase

Occasionally, sellers maintain asset ownership until the buyer has paid all due amounts. If there’s a significant delay in payments, the gap between control transfer and legal title transfer might be lengthy. The IASB determined that transaction accounting should reflect its substance, not its legal form. Therefore, transactions that are essentially sales or purchases shouldn’t be accounted for under IFRS 16, even if there’s a delay in transferring the legal title (IFRS 16.BC138-140).

Separating components of a contract

Under IFRS 16.12, every lease and non-lease component within a contract should be accounted for independently.

Lease components

A right to use an underlying asset is a separate lease component when the following conditions are satisfied (IFRS 16.B32):

- The lessee can derive benefit from the asset either independently or in conjunction with readily available resources.

- The asset doesn’t depend heavily upon, nor is it closely connected with, other assets in the contract.

Application of these requirements is illustrated in Example 12 accompanying IFRS 16.

Non-lease components

A lease agreement might encompass non-lease charges, such as utilities in a building lease or maintenance for a car lease. These should be accounted for separately from the lease in line with relevant IFRSs. However, as per IFRS 16.15, a practical expedient is available for lessees (not lessors). They can choose, for a particular class of assets, not to separate non-lease components from lease components, treating them as a singular lease component.

Example 12 in IFRS 16 illustrates application of these requirements.

Costs without transfer of goods or services to lessee

Certain lease contracts might stipulate fees for activities and costs that don’t provide a good or service to the lessee. An example is an annual administrative fee that doesn’t transfer any tangible benefit to the lessee (i.e., isn’t distinct). These fees aren’t considered separate components but are part of the overall consideration, allocated to the separately identified contract components (IFRS 16.B33).

Allocating consideration to separate components

Contractual consideration should be allocated to each lease component based on the component’s relative stand-alone price and the combined price of non-lease components. This stand-alone price should mirror the amount the lessor or a comparable supplier would charge separately for the component. If there’s no observable stand-alone price, an estimation should be made (IFRS 16.13-14).

Refer to Example 12 accompanying IFRS 16 and the example below.

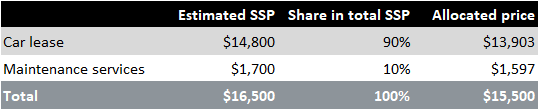

Example: Allocating consideration to separate components

A lessee agrees to a 4-year car lease. The lessor will also offer maintenance during this period. The collective fee for the car lease and services is $15,000 annually. Furthermore, the lessee incurs an annual $500 charge, reimbursing the lessor’s car tax. This fee isn’t seen as a separate component because it doesn’t provide any tangible asset or service to the lessee (IFRS 16.B33).

The annual $15,500 payment to the lessor is divided between lease and non-lease components based on estimated stand-alone selling prices (SSP):

The amount attributed to maintenance isn’t added to the lease liability but is expensed when incurred. However, there’s an exception if the lessee opts for the practical expedient as described in IFRS 16.15.

Leases in joint arrangements

For contracts initiated by or on behalf of a joint arrangement, the lease assessment should be from the perspective of the joint arrangement, not the joint operator or joint venturer. Hence, a joint operator cannot claim that a joint arrangement’s contract doesn’t contain a lease just because it only gains a fraction of economic benefits from the asset or cannot control the asset’s use (see IFRS 16.B11, BC126).

More about IFRS 16

See other pages relating to IFRS 16: