‘Value in use’ can be defined as the future cash inflows and outflows arising from the continued use of an asset and from its ultimate disposal. These cash flows are discounted to account for the time value of money and risk. Often, practitioners use a single cash flow estimate based on budgets, although IAS 36 also allows the use of the expected value approach.

Value in use represents one of the two measures for calculating an asset’s recoverable amount and is covered in IAS 36.30-57 and IAS 36.A1-A14. Let’s consider an example illustrating a simple impairment test of a cash-generating unit (CGU) based on value in use:

Example: Simple impairment test of a CGU based on value in use

The following illustrates a simple impairment test of a CGU prepared on 31 December 20X0. It is recommended that you download and review the accompanying Excel file.

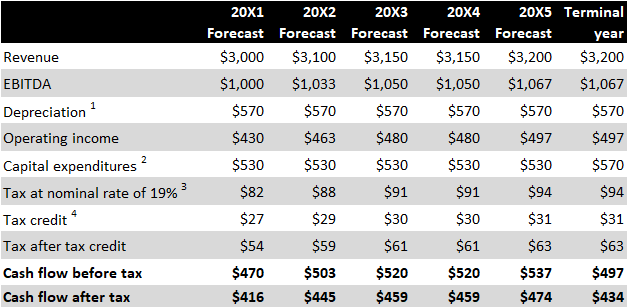

The calculation of value in use begins with cash flow projections:

- Depreciation refers to the notional tax depreciation required only for value in use calculations (to determine income tax charge). The term ‘notional’ is used under the assumption that the carrying value of the CGU and its tax base are equal on day 1.

- Strictly speaking, capital expenditure should only include the replacement of existing assets at the end of their useful life (refer to the section on improvements and restructuring). This may differ from the depreciation charge, for instance, due to technological changes.

- Tax is calculated as a percentage of operating income. Temporary differences should be disregarded as they are already included in deferred tax. Interest is excluded from cash flow projections in impairment tests as the cost of capital is accounted for in the discount rate.

- For this example, it’s assumed that the entity operates in a region with high unemployment rates and thus receives a one-third reduction in its tax charge.

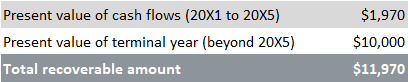

The value in use, based on the above cash flow projections, is calculated (see the Excel file) as follows:

In this calculation, the discount rate (WACC) used is 5.48% and the Perpetuity Growth Rate (PGR – estimated growth rate beyond the period covered by cash flow projections) is 2%.

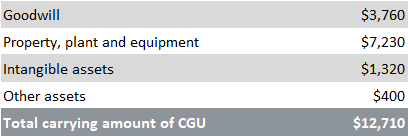

The recoverable amount is then compared to the carrying amount of the CGU, which is calculated as follows:

Since the carrying amount of the CGU exceeds its recoverable amount by $740, the CGU is impaired. Accordingly, an impairment loss of $740 is recognised in P/L.

--

Too many IFRS updates? I know the feeling! That's why I created Reporting Period. It's a concise monthly summary of IFRS developments and Big 4 insights for accounting professionals. It's completely free, with zero spam, and you can unsubscribe anytime with one click. Interested? Leave your email below:

Cash flow projections

The calculation of value in use is based on accurate cash flow projections. According to IAS 36.33, these projections should originate from the latest financial budgets or forecasts that have received management’s approval. Specifically, cash flow projections encompass the following, as outlined in IAS 36.39:

- Cash inflows from the ongoing use of assets within the CGU,

- Cash outflows that are essential for generating these inflows, and

- Net cash flows anticipated from disposing of assets at the end of their useful life.

Future cash flow estimates must include outflows necessary to sustain the economic benefits expected from the asset in its current condition (see Enhancements, improvements and restructuring). When a CGU comprises assets with varied estimated useful lives, replacing shorter-lived assets is considered part of regular maintenance in forecasting future cash flows related to the unit (IAS 36.49).

While cash flow projections should be grounded in management-approved forecasts, IAS 36 limits their span to a maximum of five years. This constraint arises because forecasts for more extended periods tend to lack detail and reliability. However, if management can demonstrate its ability to accurately predict cash flows over a longer period, based on past experience, extending beyond five years is permissible. In practice, most companies adhere to this five-year limit.

IAS 36 explicitly requires the extension of cash flow projections beyond the timeframe of the latest forecasts. This involves extrapolating them into future years, as exemplified earlier. A key factor in this extrapolation is the projected growth rate (PGR). IAS 36 stipulates that this rate must not surpass the long-term average growth rate for the relevant products, industries, countries, or markets where the entity operates or where the asset is used. This restriction is in place because market entry by competitors in favourable conditions is likely to limit growth. Consequently, entities generally struggle to exceed the historical average growth rate over the long term for their respective products, industries, countries, or markets (IAS 36.37).

Consistency between assets and liabilities tested for impairment and related cash flows

Ensuring consistency in determining the carrying amount of a CGU and its related cash flows is vital (IAS 36.75-79). Due to practical considerations, the value in use calculation frequently incorporates cash flows associated with provisions, working capital items or hedging instruments. In such instances, the CGU’s carrying amount should also reflect these assets and liabilities. For example, if a trade payable reduces a CGU’s carrying amount, its cash flows should also be reduced by the cash outflow needed to settle this payable. When incorporating changes in working capital into the terminal year (i.e., projecting them indefinitely), entities must ensure that this balance is reasonable and substantiated based on experience. This is especially applicable for entities maintaining negative working capital balances. As illustrated in this example, the terminal year forms a significant portion of the value in use.

Conversely, certain liabilities such as long-term post-employment benefits are recognised and paid continually, meaning that future payments partly relate to future events and should be included in projected cash flows. In simpler terms, entities can’t exclude payments of, for example, post-employment benefits from projected cash flows merely because an actuarial provision has already been recognised. In practice, distinguishing between payments related to an already recognised provision and payments relating to future years of service can be challenging. Therefore, it’s advisable to develop a simplified solution, potentially based on the current service cost included in a financial forecast.

Another crucial point to note is that entities should exercise caution when including provisions, particularly dismantling provisions, in the carrying amount of a CGU and its value in use. These provisions are discounted using a risk-free rate (as mandated by IAS 37) in the statement of financial position, and it is not appropriate to discount related cash outflows in impairment tests using WACC (or another discount rate) applied to assets. For some CGUs, the difference might be material.

Furthermore, cash flows associated with certain provisions are often omitted from business plans, which are subsequently used for impairment tests (e.g., if the timing of the cash flow is uncertain or expected after the period covered by the plan). In such cases, the present value of the cash outflow can be added separately to the value in use if the provision is included in the CGU’s carrying amount. Once again, remember to use the proper discount rate for the cash flows for which provisions are recognised (not WACC).

Example: Deferred tax liabilities and goodwill arising on fair value adjustments after a business combination

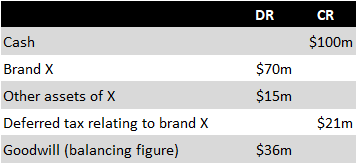

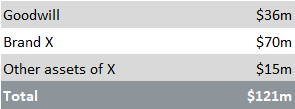

Entity A acquires Entity X for $100m. Subsequently, Entity A recognises the well-known brand of Entity X at its fair value of $70m. The brand has an indefinite useful life and is not tax-deductible. The applicable tax rate is 30%. The fair value of Entity X’s other identifiable assets, equal to their tax base, stands at $15m.

In Entity A’s consolidated financial statements, the following entries are made:

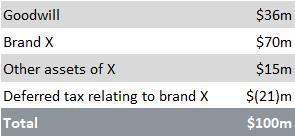

A deferred tax liability of $21m is recognised in relation to brand X ($70m x 30%), given that the tax base of brand X is $0. As the brand won’t be amortised, the deferred tax will be realised following either a disposal of, or impairment loss on, the brand.

Entity X operates as a separate CGU, and its assets should be tested for impairment in line with IAS 36. For the sake of clarity, let’s suppose the impairment test takes place one day after the acquisition and the carrying of assets remains unchanged.

As we can observe, the carrying amount of the assets to be tested totals $121m, which is somewhat surprising given Entity A only paid $100m for these assets. If we assume the recoverable amount of Entity X mirrors what Entity A paid (i.e., $100m), does this suggest a post-acquisition impairment loss of $21m needs immediate recognition?

The apparent excess of $21m of the carrying amount over the recoverable amount stems from the deferred tax liability associated with brand X. While IAS 36 doesn’t account for this type of discrepancy, it is generally acceptable in practice to include the deferred tax liability when calculating the carrying amount of the CGU.

Consequently, no impairment loss is recognised.

Internal transfer pricing

When calculating value in use, entities should adjust the internal pricing between CGUs to arrive at estimated market prices. The requirement to adjust internal transfer pricing applies to all CGUs, not just those with an active market for their output (IAS 36.71).

Q&A – Transfer pricing between subsidiaries and its on their separate financial statements

Entity A owns two subsidiaries, X and Y. X manufactures goods which are then sold to Y, which then uses them to produce final goods for sale to external customers. X sells its goods to Y below cost, rendering X unprofitable. However, X could sell its products to external customers at a price higher than Y pays. In the consolidated financial statements prepared by Entity A, X and Y are separate CGUs.

Question 1: For the purpose of impairment tests, should the prices paid by Y to X be adjusted to reflect estimated market prices?

Answer 1: Yes. This requirement is laid out in paragraph IAS 36.71.

Question 2: What prices should entities X and Y use for the purpose of impairment testing in their separate financial statements?

Answer 2: Although IAS 36 does not explicitly refer to separate financial statements, my suggestion is that prices should also be adjusted in X and Y’s separate financial statements. If this approach is adopted, it should be clearly disclosed.

Corporate assets and overheads

Corporate assets and related overheads should be allocated to the carrying amounts of CGUs and reflected in cash flow forecasts as prescribed in IAS 36.100-103. Refer to Illustrative Example 8 to IAS 36 for further discussion.

Enhancements, improvements and restructuring

As outlined in IAS 36.44-49 and illustrated in Examples 5 and 6 to IAS 36, projected cash flows should exclude any anticipated future cash inflows or outflows stemming from future restructurings (until the provision recognition criteria are met) or from enhancements that boost the asset’s performance. In reality, this often poses a challenge, as future improvements and restructurings are typically incorporated into management budgets. To prepare cash flow projections that exclude such items usually requires significant adjustment of an approved budget. A common workaround is to:

- Calculate the value in use derived from an approved budget, inclusive of future improvements and restructurings.

- Estimate the present value of cash flows resulting from major future improvements and restructurings (usually based on a business case for these projects).

- Compute value in use that excludes future significant improvements and restructurings by subtracting the value from step 2 from the value in step 1.

If the impact of future improvements or restructurings significantly alters the value in use calculation, it might be worth changing the base for the recoverable amount calculation to fair value less costs of disposal. When determining the fair value of a CGU, entities may consider future improvements and restructurings, as long as a market participant would also take them into account. However, in the fair value calculation, entities cannot include any conditions specific to the reporting entity that wouldn’t be available to a third party (see Differentiating ViU from FVLCD).

The IASB has tentatively decided to permit the inclusion of cash flows resulting from a future restructuring or enhancement in the value in use calculation in upcoming IAS 36 improvements, to align it with approved budgets and forecasts.

Foreign currency cash flows

As per IAS 36.54, future cash flows in foreign currency should be discounted using a discount rate appropriate for that specific currency and converted using the spot exchange rate at the date of the value in use calculation. Usually, this requires adjustments to management forecasts, as they are often prepared using expected exchange rates rather than the spot rate.

Interest payments

The cash flows incorporated into the value in use calculation should align with the applied discount rate. Given that the discount rate already reflects the time value of money and business risks, entities should exclude interest and dividend payments from cash flows used for the value in use calculation.

Discount rate

The discount rate used for the value in use calculation should reflect current market assessments of (IAS 36.55-57, IAS 36.A15-A21):

- Time value of money up until the asset’s useful life ends, and

- Asset-specific risks for which the future cash flow estimates have not been adjusted.

The discount rate for testing assets for impairment should not be tied to the entity’s capital structure (IAS 36.A19). As such, it is more appropriate to use a benchmark rate for companies within the same industry and region, rather than an entity-specific rate. This approach ensures that the assessed value in use of assets remains independent of any particular entity’s capital structure.

IAS 36 mandates the use of pre-tax cash flows with a pre-tax discount rate for discounting purposes. However, a different approach is often used in practice. The calculations presented below result in a post-tax discount rate. Note that different discount rates may apply to cash flows in different countries, currencies, or even for different products within the same CGU.

WACC as the discount rate

Weighted Average Cost of Capital (WACC) is frequently used as the discount rate for value in use calculations. While there are elaborate methods of calculating WACC (that could fill a 500-page book), a simplified approach is presented here. Each element of the calculation will be discussed in the subsequent sections. Please also review the accompanying Excel file for further details.

The calculation begins with the equation:

- Re = Cost of equity

- Rd = Cost of debt

- g = Gearing level

- t = Corporate tax rate

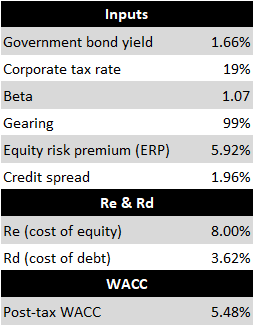

For instance, consider this WACC calculation for a UK grocery retail chain:

Cost of equity

Cost of equity equation

There are various methods for estimating the cost of equity. The following example uses the popular Capital Asset Pricing Model (CAPM). IAS 36.A17 acknowledges CAPM as a suitable starting point. The associated Excel file contains an example demonstrating the calculation of WACC for a retail chain operating in the UK.

CAPM equation:

Re = Rf + β x ERP

- Re = Cost of equity

- Rf = Risk free rate

- β = Beta

- ERP = Equity risk premium

Risk-free rate

The risk-free rate is typically based on the yield of government bonds (denominated in the same currency as the estimated cash flows) with a time horizon similar to the timing of cash flows. For CGUs with cash flows discounted into perpetuity, very long-term bonds (e.g., 20-year) should be used. If the government bond yield has a significant default risk integrated into the yield, entities should adjust the government bond yield for default risk using credit spreads.

Beta

Beta is a measure of volatility (risk) relative to the market. If a stock’s beta equals 1, it means that the stock, statistically speaking, moves in line with the market. The reference market is usually a broad index in a particular country (such as the S&P 500 in the US). For instance, if beta equals 1.2, the stock in question is more volatile than the market. If the market goes up by 10%, the stock with a beta of 1.2 goes up by 12% (10% x 1.2).

Beta is calculated using regression analysis. Betas for specific entities or industries can be sourced from providers like Bloomberg or Reuters (paid subscription), or from free sources such as Aswath Damodaran.

It’s crucial to understand the difference between unlevered and levered betas when using these metrics. Unlevered beta is the beta of a company without debt, that is, without the effects of financial leverage:

Unlevered beta = levered beta / [1 + (1 – tax rate) x gearing]

For the purpose of WACC used in impairment testing, entities need a levered beta. However, this should not stem from the gearing ratio or beta specific to the reporting entity. Instead, a benchmark gearing should be used, for example, the average gearing for the sector in the entity’s country or region.

Equity Risk Premium (ERP)

The Equity Risk Premium (ERP) represents the additional return that investors expect due to investing in riskier assets. It is expressed as a yield above a risk-free rate. For instance, if the risk-free rate is 2% and the ERP is 5%, investors, on average, would expect equities to yield 7%. The ERP is generally calculated based on historical premiums by comparing returns on equities and risk-free rates over a certain period.

For less mature markets, the ERP is calculated by adding a Country Risk Premium (CRP) to the ERP calculated for a mature market. For example, entities in Eastern European countries might adopt the ERP calculated for Germany and supplement it with a specific country’s CRP. The CRP is calculated based on sovereign rating and/or credit spreads.

As you might imagine, this process can become quite complex. Similar to obtaining betas, entities can access sources like Bloomberg, Reuters (paid subscription), or data from Mr Damodaran.

Cost of debt

Just like the cost of equity, the goal is to obtain a benchmark cost of debt, not a borrowing rate that is specific to the entity. Estimating a benchmark cost of debt typically involves adding a credit spread to the risk-free rate. Credit spreads can be estimated based on:

- Bond ratings for entities from the relevant sector and region, and

- Average credit spreads for bonds with the same ratings.

Another method, proposed by Mr Damodaran, is to estimate a global credit spread which is then increased by an additional risk premium based on the standard deviation of stock prices. Again, resources like Bloomberg, Reuters (paid subscription), or Damodaran’s data will be of assistance.

Impact of inflation

The approach to inflation (IAS 36.40) must be consistent:

- If future cash flows consider inflation, we should utilise nominal discount rates (i.e., advertised or ‘headline’ rates).

- If future cash flows are stated in real terms (not adjusted for future inflation), we should use real discount rates. These are adjusted advertised rates where the real interest rate equals the nominal interest rate minus the projected rate of inflation.

Similarly, when estimating the growth rate beyond the period covered by cash flow projections (PGR), we should distinguish between nominal (inflationary growth) and real growth. Nominal growth rate can be positive even for entities without real growth.

Pre-tax vs post-tax approach

IAS 36 requires the calculation of value in use using pre-tax cash flows and a pre-tax discount rate. This requirement arises due to the complexity that tax cash flows introduce to value in use calculation. However, rates observed in the market are typically post-tax, so in practice, value in use is often calculated with post-tax cash flows and a post-tax discount rate.

Under the post-tax approach to value in use calculation, the tax cash flows considered for calculation are not the same as the cash flows the entity anticipates paying to tax authorities. Entities should not account for temporary differences and unused tax losses, as these are recognised as deferred tax when necessary.

In an ideal scenario, entities would calculate tax payments as if the tax base of the assets equalled their recoverable amount. However, due to the complexity and iterative nature of this calculation, it’s often assumed in practice that the tax base of assets equates to their carrying value in the statement of financial position. In other words, accounting depreciation is used when arriving at the income tax charge for the value in use calculation.

If there are significant timing differences between tax and accounting depreciation, using tax depreciation is also acceptable, but the carrying amount of the CGU should then also include deferred tax assets or liabilities. Deferred tax is recognised on an undiscounted basis in the statement of financial position, but for impairment testing purposes, using a discounted amount is appropriate.

IAS 36 requires the disclosure of the pre-tax discount rate, and entities should observe this requirement even if the value in use was calculated on a post-tax basis. IAS 36.BCZ85 states, ‘In theory, discounting post-tax cash flows at a post-tax discount rate and discounting pre-tax cash flows at a pre-tax discount rate should give the same result, as long as the pre-tax discount rate is the post-tax discount rate adjusted to reflect the specific amount and timing of the future tax cash flows. The pre-tax discount rate is not always the post-tax discount rate grossed up by a standard rate of tax.’

Therefore, instead of grossing up the post-tax discount rate by the nominal income tax rate, entities can calculate the pre-tax rate iteratively, e.g., by using a spreadsheet function like goal seek. This ensures that the value in use, based on pre-tax cash flows and a pre-tax discount rate, equals the value in use based on post-tax cash flows and a post-tax discount rate.

When adopting the post-tax approach, it’s advisable to disclose both discount rates: pre-tax and post-tax.

Thankfully, the IASB plans to simplify the requirements by removing the requirement to use pre-tax inputs in the calculation.

Differentiating value in use from fair value less costs of disposal

Value in use and fair value less costs of disposal both provide means to estimate an asset’s recoverable amount. In essence, the fair value reflects the assumptions that market participants would use when pricing the asset, while value in use is based on entity-specific factors. IAS 36.53A clarifies that fair value does not account for:

- Synergies that may be present when combining the asset with the entity’s other assets.

- Unique legal rights or restrictions inherent to the asset’s owner.

- Tax implications that only apply to the current asset holder.

More about IAS 36

See other pages relating to IAS 36:

Impairment Framework for Non-Financial Assets

Cash-Generating Units (CGUs)

Impairment of Assets: Disclosure