The equity method, governed by IAS 28, is a simplified form of consolidation used for accounting for investments in associates and joint ventures. The key distinction is that the investee’s financials are not incorporated line-by-line into the investor’s financial statements. Instead, a single asset representing the equity-accounted investment is recognised in the statement of financial position. Similarly, single-line items are presented in the investor’s P/L and OCI statements. In applying the equity method, the investment is initially recognised at cost and subsequently adjusted for the post-acquisition changes in the investor’s share of the net assets.

In September 2024, the IASB published an exposure draft (along with a snapshot) proposing amendments to IAS 28 to address common application issues related to the equity method. Given the age of the standard, the IASB is also using this opportunity to reorganise its structure for improved consistency and clarity. The proposed changes are discussed in the relevant sections below.

Let’s begin with an introductory example on applying the equity method:

Example: Simple illustration of the equity method application

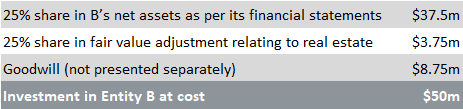

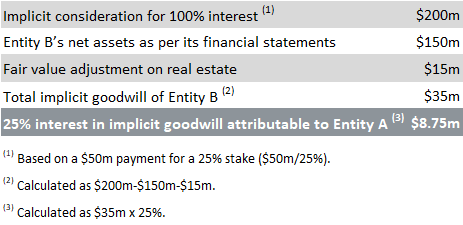

On 1 January 20X1, Entity A acquired a 25% interest in Entity B for a total consideration of $50m and applies the equity method in accounting for it. Entity B’s net assets as per its financial statements totalled $150m. These assets include real estate with a carrying amount of $20m and a fair value of $35m, with a remaining useful life of 15 years. For other assets and liabilities, the carrying amount is roughly equivalent to their fair value. In this example, deferred tax is not considered. A corresponding Excel file is available for download.

Entity A recognises the investment in Entity B at cost, i.e., $50m, on the date of acquisition. This amount can be broken down as follows:

Goodwill was calculated as shown below:

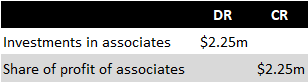

During the year ended 31 December 20X1, Entity B generated net income of $10m and paid dividends of $7m. In addition, Entity A must account for the $0.25m of additional depreciation charge on the fair value adjustment on real estate when applying the equity method. This is calculated as the fair value adjustment on real estate divided by 15 years of remaining useful life, multiplied by Entity A’s 25% share (i.e., $15m/15 years x 25%).

The entries made by Entity A at 31 December 20X1 are as follows:

1. Recognition of 25% share of B’s net income of $10m less 25% share in depreciation of fair value adjustment:

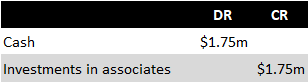

2. Recognition of 25% share of $7m of dividends paid by Entity B:

--

Too many IFRS updates? I know the feeling! That's why I created Reporting Period. It's a concise monthly summary of IFRS developments and Big 4 insights for accounting professionals. It's completely free, with zero spam, and you can unsubscribe anytime with one click. Interested? Leave your email below:

Initial recognition

An investment accounted for under the equity method is initially recognised at cost. While IAS 28 currently does not specify the measurement of cost, the 2024 exposure draft aims to address this gap. According to the IASB’s current views, the cost of an equity-accounted investment at initial recognition should include:

- The fair value of the consideration transferred.

- Contingent consideration measured at fair value.

- The fair value of any previously held interest.

- Deferred tax effects related to the investor’s share of the fair value of the associate’s or joint venture’s identifiable assets and liabilities.

Additionally, when an investment transitions from a consolidated subsidiary to an associate or joint venture, the cost for initial recognition is the fair value of the retained interest as of the date control is lost (as per IFRS 10.25(b)).

Consideration transferred

The consideration transferred should be measured at fair value. This is calculated as the sum of the acquisition-date fair values of assets transferred by the acquirer, liabilities incurred by the acquirer to the former owners of the acquiree, and any equity interests issued by the acquirer. Although the 2024 exposure draft does not explicitly define this formula, it is consistent with the IFRS 3 requirements.

The exposure draft does not provide specific guidance for cases where investments are acquired using non-monetary assets or a combination of cash and non-monetary assets. In such situations, entities may refer to IAS 16.24-26, which requires measuring the cost of the asset at fair value and recognising any difference between the fair value of the acquired asset and the carrying amount of assets surrendered in profit or loss. IAS 16 also offers guidance for transactions that lack commercial substance or where the fair value of neither the received nor the given-up asset is reliably measurable.

Contingent consideration

The 2024 exposure draft specifies that contingent consideration should be recognised at fair value on the date significant influence is obtained and included in the cost of the equity-accounted investment at initial recognition. Contingent consideration is then remeasured to fair value at each reporting date, with any changes recognised in profit or loss. However, contingent consideration classified as an equity instrument should not be remeasured, in line with the general requirements for the subsequent measurement of equity instruments.

Previously held interest

Significant influence may be acquired gradually over time through the incremental purchase of ownership interests. The 2024 exposure draft stipulates that the fair value of previously held interest must be included in the cost of the equity-accounted investment at initial recognition. Prior to obtaining significant influence, the previously held interest would have been accounted for under IFRS 9 and should be remeasured to fair value at the date significant influence is achieved. Any resulting fair value gains or losses should be recognised in P/L or OCI, depending on the previous classification of the investment under IFRS 9.

Transaction costs

The 2024 exposure draft does not specifically address the accounting treatment of transaction costs incurred during the acquisition of an investment. However, the IFRS Interpretations Committee has previously analysed this issue, noting that IFRS generally require assets not carried at fair value through profit or loss to be measured at cost at initial recognition. This cost includes expenditures directly attributable to the acquisition of the asset, such as legal fees, transfer taxes, and other transaction costs. As a result, such directly attributable costs are typically included in the cost of an asset in the investor’s financial statements. Any costs incurred prior to the actual acquisition of the asset can be recognised as prepayments and subsequently capitalised as part of the initial carrying amount of the investment at the acquisition date.

Changes in ownership interest

The current version of IAS 28 does not provide specific guidance on how to account for the purchase or disposal of ownership interest in an associate or joint venture while retaining significant influence or joint control. The 2024 exposure draft proposes that, when acquiring an additional ownership interest, an investor should:

- Recognise the additional ownership interest at the fair value of the consideration transferred.

- Include in the carrying amount of the investment the investor’s additional share of the fair value of the associate’s or joint venture’s identifiable assets and liabilities.

- Account for any difference between these two amounts as either goodwill (included in the carrying amount of the investment) or a gain from a bargain purchase recognised in P/L.

Conversely, when an investor disposes of part of its ownership interest, the investor should derecognise the proportionate share of the investment based on the carrying amount of the associate or joint venture and recognise any difference between the consideration received and the derecognised portion in P/L.

In cases where an investment in an associate is reclassified as a joint venture, or vice versa, the entity continues to apply the equity method without remeasuring the retained interest (IAS 28.24).

Goodwill and fair value adjustments

When acquiring an interest in an associate or joint venture, the investor must recognise its share of the associate’s or joint venture’s net assets at fair value, including any associated goodwill. This treatment is similar to full consolidation, except that under the equity method, the entire investment, including goodwill, is represented as a single line item (IAS 28.32). Additional adjustments, such as depreciation related to fair value adjustments for assets recognised at the time of acquisition (like an internally generated brand) must also be recognised.

Since goodwill is not separately recognised under the equity method, the mandatory annual impairment testing requirements of IAS 36 do not apply (IAS 28.42). Instead, any impairment is allocated to the overall investment.

According to the proposals in the 2024 exposure draft, if the investor’s share of the fair value of the identifiable assets and liabilities of the associate or joint venture exceeds the cost of the investment, the excess should be recognised as a gain from a bargain purchase in P/L.

Determining the fair value is typically more challenging for an associate since having significant influence can make it difficult to obtain all the necessary valuation inputs. Therefore, approximations and estimates are frequently used to a greater extent than usual. A simple example illustrating an investment in an associate or joint venture, accounted for under the equity method and broken down into the investor’s share in net assets, fair value adjustments and goodwill, is provided here.

Intercompany transactions with associates and joint ventures

Regular intercompany transactions

Associates and joint ventures do not form part of the group according to the IFRS 10 definition, as a group consists of a parent and its subsidiaries. Consequently, intercompany transactions with associates and joint ventures are not eliminated in consolidated financial statements. However, some accounting practitioners do eliminate regular intercompany transactions to the extent of the investor’s share in an associate or joint venture. These two methods are illustrated below.

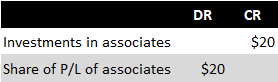

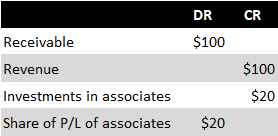

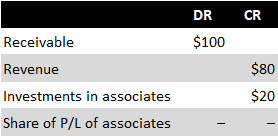

Example: Revenue earned from an associate

Company P, with a 20% interest in Company A (its associate), provides consulting services to A for $100 during the year. As services are provided, P recognises revenue in its books:

Associate A recognises the corresponding expense:

When applying the equity method in its consolidated financial statements, Company P does not eliminate the recognised revenue and receivable. However, it needs to recognise 20% of its share in A’s profit or loss:

Overall, this transaction has the following impact on P’s consolidated financial statements:

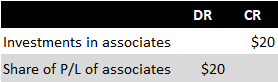

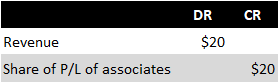

Alternative approach

As previously mentioned, a minority of practitioners eliminate even ‘regular’ intercompany transactions to the extent of the investor’s share in an associate or joint venture. Under this approach, when applying the equity method in its consolidated financial statements, Company P from our example eliminates 20% of the recognised revenue and correspondingly deducts this amount from its share in A’s profit or loss. The consolidation entries under this approach would be as follows:

Initially, Company P recognises 20% of its share in A’s profit or loss:

Subsequently, P eliminates its 20% share (the intercompany part) in the revenue and expenses recognised on consulting services:

In summary, the alternative approach has the following impact on P’s consolidated financial statements:

Upstream and downstream transactions involving assets

IAS 28.28 specifies that gains and losses from ‘upstream’ transactions (i.e., sales from an associate or joint venture to the investor) and ‘downstream’ transactions (i.e., sales from the investor to the associate or joint venture) must only be recognised to the extent of the interests held by unrelated investors. As a result, when applying the equity method, the investor’s share of the investee’s gains or losses from these transactions is eliminated.

However, the 2024 exposure draft proposes to remove this requirement. Under the proposed changes, an investor would recognise in full all gains and losses from upstream and downstream transactions with its associates or joint ventures. Until these amendments to IAS 28 are finalised, entities should continue to eliminate gains and losses in accordance with IAS 28.28. This is illustrated in the examples that follow.

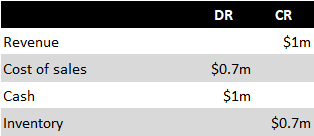

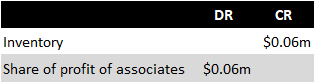

Entity A holds a 20% interest in Entity B and accounts for it using the equity method. In the year 20X0, Entity A sold an item of inventory to Entity B for $1m, which was carried at a cost of $0.7m in A’s books. During the year 20X1, Entity B sold this inventory to its client for $1.5 million. Deferred tax has been ignored in this example. Please note that an Excel file for this example can be downloaded.

Year 20X0

Entity A recognises the sale to Entity B in its books:

Simultaneously, Entity B recognises the purchase in its books:

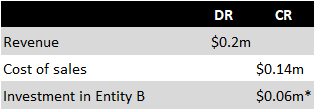

In the consolidated financial statements, Entity A recognises an adjustment to eliminate the gain on the sale of inventory with regard to its 20% interest in Entity B:

* Entity A adjusts the value of its investment in B, as the asset subject to elimination is held by B.

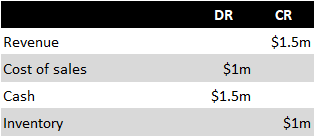

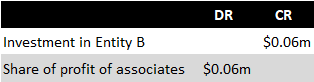

Year 20X1

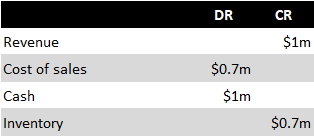

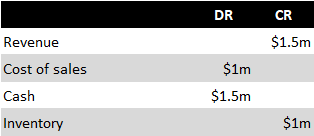

Entity B recognises the sale to a client:

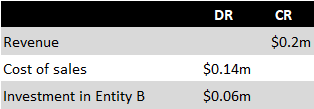

In the consolidated financial statements, Entity A reverses the previous entry and recognises a 20% portion of revenue and cost of sales:

In addition, Entity A recognises its share in the gain made by Entity B:

Example: Accounting for an upstream transaction

Entity A holds a 20% interest in Entity B and accounts for it using the equity method. In the year 20X0, Entity B sold an item of inventory to Entity A for $1m, which was carried at a cost of $0.7m in B’s books. During the year 20X1, Entity A sold this inventory to its client for $1.5 million. Deferred tax has been ignored in this example.

Year 20X0

Entity B recognises the sale to Entity A in its books:

Simultaneously, Entity A recognises the purchase in its books:

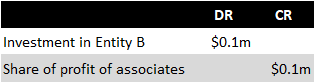

In the consolidated financial statements, Entity A recognises its share in the gain made by Entity B:

At the same time, Entity A eliminates the effect of the upstream transaction concerning its 20% interest in the consolidated financial statements. There are two acceptable approaches to this step, both commonly used in practice:

Approach 1:

Approach 2:

Year 20X1

Entity A recognises the sale to a client:

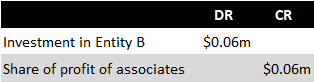

Additionally, Entity A reverses the consolidation entry made in year 20X0 and includes the profit that B made on the sale to A.

This approach should also be applied to the contribution of non-monetary assets to an associate or joint venture (IAS 28.30).

Associate or joint venture as a parent

The share of an investee’s profit or loss and OCI is determined based on its consolidated financial statements. This includes the investee’s consolidated subsidiaries and other investments accounted for using the equity method (IAS 28.10). While IAS 28 doesn’t provide specific guidance on how to treat non-controlling interest in the investee’s group, it is most logical for the investor to account only for the controlling interest’s share of P/L and OCI. This is because the net income attributable to non-controlling interest of the investee’s group will never accrue to the investor.

For further information, refer to the forums discussion on reciprocal equity interests (‘cross-holdings’) between parent and associate.

Dividends and other capital distributions

Dividends and other capital distributions received from an investee reduce the carrying amount of the investment (IAS 28.10).

Exchange differences on translation

Exchange differences that arise when translating an investee’s financial statements into the investor’s presentation currency are recognised in OCI (IAS 21.44).

Equity transactions of associate or joint venture

The current version of IAS 28 does not provide guidance on how to account for equity transactions conducted by an associate or joint venture, such as issuing or redeeming its own shares. The 2024 exposure draft addresses this gap by requiring that investors treat changes in ownership interest arising from these equity transactions as if they were acquiring or disposing of an ownership interest while retaining significant influence or joint control.

Loss making associate or joint venture

An investor recognises losses in an associate or joint venture up to the total amount of its investment. This means that when the value of an investment falls to zero, the investor stops recognition of further losses under the equity method, unless there is a legal or constructive obligation necessitating the recognition of a liability. Subsequent profits from such an investee are only recognised once the previously unrecognised losses have been recovered (IAS 28.38-39).

Importantly, an investment in an associate is not limited to ordinary shares held. It also encompasses all long-term interests (e.g., long-term financing) that substantively make up the entity’s net investment in an associate or joint venture. If such interests exist, cumulative losses exceeding the (equity-accounted) carrying amount of ordinary shares held by the investor are allocated to other components of the entity’s interest in reverse order of their seniority (i.e., priority in liquidation). Financial assets like preference shares and long-term receivables or loans without adequate collateral are examples of assets that form part of the net investment (IAS 28.38). See the example prepared by the IASB for further clarification.

Impairment

After applying IFRS 9 to long-term interests (as discussed below) and recognising its share of the associate’s or joint venture’s losses, the investor must assess whether there is objective evidence that its net investment in the associate or joint venture is impaired (IAS 28.40-41C). Impairment indicators listed in IAS 28 include significant financial or operational difficulties of the associate or joint venture, as well as a decline in the fair value of the net investment to below its carrying amount.

It is important to note that impairment losses recognised by an associate or joint venture may not always be reflected in the investor’s financial statements at the same amount. This is often due to fair value adjustments and goodwill recognised by the investor. Also, since goodwill is not separately recognised as an asset under the equity method, impairment losses on an investment in an associate or joint venture can be fully reversed in subsequent periods (IAS 28.42).

Net investment in an associate or joint venture

Impairment testing applies to the total net investment in an associate or joint venture. This includes all long-term interests (e.g., long-term financing) that, in substance, form part of the entity’s net investment. Refer to the section on loss-making associate or joint venture for more information.

The introduction of paragraph IAS 28.14A in 2017 with an accompanying illustrative example Long-term Interests in Associates and Joint Ventures clarified the interaction between IAS 28 and IFRS 9 regarding financial assets that form part of the entity’s net investment:

- An entity applies IFRS 9 to account for long-term interests, including the impairment requirements.

- When allocating any losses of the associate or joint venture in accordance with IAS 28.38, the entity includes the carrying amount of those long-term interests (determined applying IFRS 9) as part of the net investment to which the losses are allocated.

- The entity then assesses for impairment the net investment in the associate or joint venture, of which the long-term interests form a part, by applying the requirements in paragraphs 40 and 41A–43 of IAS 28.

- If an entity allocates losses or recognises impairment in steps 2 and 3 above, the entity omits those losses or that impairment when accounting for long-term interests under IFRS 9 in subsequent periods.

Financial assets that, in substance, form part of the entity’s net investment in an associate or joint venture are accounted for under IFRS 9 and are not included in the line presenting investments accounted for using the equity method (though there is no explicit guidance in IFRS).

The equity method requirement

The equity method is mandatory when accounting for investments in joint ventures and associates in all financial statements, with the exception of separate financial statements prepared under IAS 27 (IAS 28.16). Nevertheless, there are conditions set out in IAS 28.17-19 which, if met, allow an entity to be exempt from using the equity method.

When an investor doesn’t have any subsidiaries but holds interests in associates or joint ventures, it’s essential to determine whether the exemptions in IAS 28.17-19 are applicable. If not, the investor is obliged to prepare financial statements using the equity method. Interestingly, these wouldn’t be referred to as ‘consolidated financial statements’, since there aren’t any subsidiaries to consolidate. Such statements are often labelled as ‘economic interest’ financial statements.

Furthermore, entities have the choice to adopt the equity method voluntarily in separate financial statements as outlined in IAS 27.10(c).

Discontinuing the use of the equity method

IAS 28.22-24 provides guidance on the discontinuation of the equity method, typically occurring when an associate or joint venture is disposed of. However, such an investment is often classified as ‘held for sale‘ before disposal, thereby suspending equity accounting prior to actual disposal. IAS 28.20-21 provides specific requirements for classifying an investment in an associate or joint venture as an asset held for sale under IFRS 5.

IAS 28.21 additionally mandates that financial statements must be ‘amended accordingly’ if an equity-accounted investment, once classified as ‘held for sale’, no longer meets the ‘held for sale’ criteria. Yet, it remains unclear whether this stipulation applies solely to the investment’s measurement or its presentation too. The IFRS Interpretations Committee has considered this issue but, having declined to add it to their agenda, they did not provide a conclusive comment in their published agenda decision. In my opinion, the following approach would be the most suitable:

- If the investment no longer meets the ‘held for sale’ criteria during the reporting period, comparative amounts should be represented as if the equity method had been continuously applied.

- The opening balance of equity for the earliest comparative period should be restated to the extent that the retrospective application of the equity method impacts periods not included in the current financial statements.

- If the impact on the opening equity balance for the earliest comparative period is significant, a third statement of financial position should be provided under IAS 1:40A.

- Previously authorised financial statements should not be reissued.

When an associate or joint venture transitions into a subsidiary, full consolidation begins under IFRS 10. The previously held interest is remeasured to its fair value, with any gain or loss recognised in the profit or loss. IFRS 3 generally applies in such scenarios.

In contrast, when a change in ownership reduces interest to the point where the investment becomes a ‘regular’ financial asset, it is accounted for at fair value under IFRS 9. The difference between the fair value of retained interest, the disposal proceeds, and the investment’s carrying amount when the equity method was discontinued, is recognised in P/L. Any items previously accumulated in OCI are recycled to P/L in the same manner as if the investee had directly disposed of the associated assets or liabilities.

Presentation in financial statements

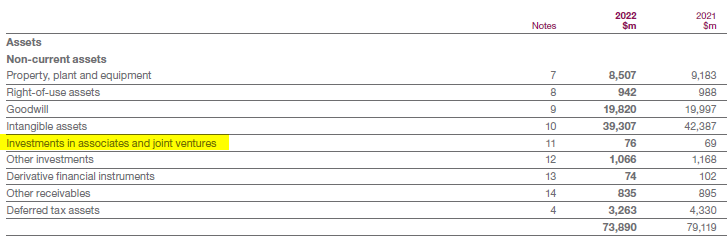

Investments accounted for using the equity method should be presented as non-current assets (IAS 28.15) in a separate line within the statement of financial position (IAS 1.54(e)). Similarly, the share of the profit or loss of associates and joint ventures accounted for using the equity method should be presented separately in P/L and OCI (IAS 1.82(c)).

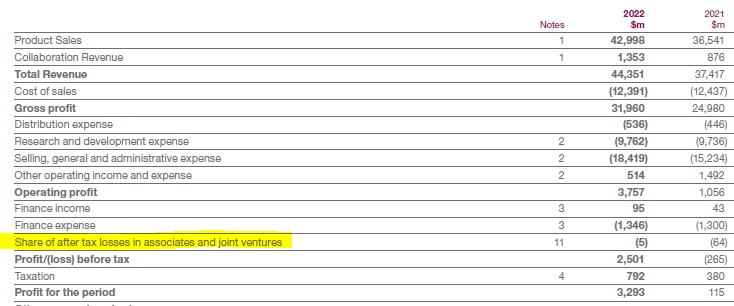

These excerpts from the financial statements of AstraZeneca may serve as an example of a common approach to the presentation of equity-accounted investees in primary financial statements:

Notably, there’s no explicit guidance regarding which section of the P/L should include the share of profit or loss from equity-accounted investments. Consequently, different entities have adopted varying methods (e.g., within operating income, just before the income tax charge, etc.). However, this line item will always be classified as investing income once IFRS 18 becomes effective.