Under IFRS 3, business combinations must be accounted for using the acquisition method, which comprises the following steps (IFRS 3.4-5):

- Identifying the acquirer.

- Determining the acquisition date.

- Recognising and measuring the identifiable assets acquired, the liabilities assumed and any non-controlling interest in the entity being acquired.

- Recognising and measuring goodwill or a gain from a bargain purchase.

Let’s dive in.

Recognising acquired assets and assumed liabilities

On the acquisition date, the acquirer is required to recognise, separately from goodwill, the identifiable assets acquired and the liabilities assumed in a business combination. Assets and liabilities satisfy the recognition criteria if they (IFRS 3.10-12):

- meet the definitions of assets and liabilities in the Conceptual Framework for Financial Reporting (‘Framework’) at the acquisition date (with limited exceptions), and

- are part of the business combination transaction between the acquirer and the entity being acquired (or its former owners), rather than resulting from separate transactions (see ‘Determining what is part of the business combination transaction‘ for further discussion).

The Framework (CF 4.3-4) defines an asset as a present economic resource controlled by the entity as a result of past events. An economic resource is a right with the potential to produce economic benefits.

Conversely, a liability is a present obligation of the entity to transfer an economic resource as a result of past events. For a liability to exist, three criteria (CF 4.26-4.27) must all be met:

- The entity has an obligation.

- The obligation is to transfer an economic resource.

- The obligation is a present obligation that exists as a result of past events.

As a result, entities cannot recognise liabilities for future expenses for which no present obligation exists on the acquisition date. Specifically, a restructuring plan that the acquirer intends to execute is not recognised on the acquisition date. Please refer to the sections on provisions and contingent liabilities for a more in-depth discussion.

Bear in mind that the criteria outlined above do not incorporate the ‘expected flow’. Hence, there’s no need for certainty, or even a likelihood, that economic benefits will be received, or expenses will be incurred, for an item to meet the Framework’s definition of an asset or a liability.

Application of the recognition principle and conditions by the acquirer may lead to the recognition of some assets and liabilities that the acquired entity did not previously recognise in its financial statements. For instance, the acquirer recognises the identifiable intangible assets, such as a brand name, a patent or a customer relationship, that the acquired entity did not recognise in its financial statements because it developed them internally and expensed the related costs (IFRS 3.13).

--Too many IFRS updates? I know the feeling! That's why I created Reporting Period. It's a concise monthly summary of IFRS developments and Big 4 insights for accounting professionals. It's completely free, with zero spam, and you can unsubscribe anytime with one click. Interested? Leave your email below:

Identifiable assets

Identifiable intangible assets

Typically, assets recognised in a business combination, but not previously recognised by the acquired entity, are internally generated intangible assets such as brands, patents, or customer relationships. For the acquirer to recognise an intangible asset, it must be identifiable, which means it fulfils one of the two following criteria (IAS 38.12, IFRS 3.B31):

- Separability criterion; or

- Contractual-legal criterion.

Separability criterion

An intangible asset satisfies the separability criterion if it can be separated or divided from the entity and sold, transferred, licensed, rented or exchanged, either individually or in conjunction with a related contract, identifiable asset or liability. This criterion should be assessed regardless of the acquirer’s intentions for the asset. Evidence of exchange transactions for the type of asset, or a similar type, is required, even if such transactions are infrequent (IFRS 3.B33-B34).

Examples of assets recognisable under the separability criterion include:

- Customer lists and non-contractual customer relationships, which encompass details such as name, age, geographical location, or order history. A customer list is recognised as an intangible asset under the separability criterion if confidentiality terms, agreements, or law do not prohibit its sale, lease, or exchange (IFRS 3.IE24, IE31).

- Technology-based intangible assets (IFRS 3.IE39-IE44).

Contractual-legal criterion

An intangible asset meets the contractual-legal criterion if it stems from contractual or other legal rights, irrespective of whether these rights are transferable or separable from the entity or from other rights and obligations (IFRS 3.B32). Examples of such assets include:

- Licences to operate in a particular sector or geographical area, even if not separable from the related assets or legal entity.

- Legally protected trademarks (IFRS 3.IE18-IE21).

- Internet domains (IFRS 3.IE 22).

- Customer contracts and orders, along with related customer relationships (IFRS 3.IE25-IE30). These contracts and placed orders (even if cancellable) arise from contractual rights and hence don’t need to meet the separability criterion to be recognised. They’re recognised even if confidentiality terms, agreements, or law prohibit their sale, lease, or exchange. Customer relationships satisfy the contractual-legal criterion if an entity has a practice of establishing contracts with its customers, irrespective of whether a contract exists at the acquisition date (IFRS 3.IE30c).

- Copyrighted materials such as films, books, etc. (IFRS 3. IE32-IE33).

- Contract-based intangible assets, with numerous examples provided in IFRS 3.IE34-IE38.

- Technology-based intangible assets (IFRS 3.IE39-IE44).

Items that are not identifiable

Intangible assets that fail to meet either the separability criterion or the contractual-legal criterion can’t be recognised separately. Instead, they are incorporated into the value of goodwill (IFRS 3.B37-B40). Such assets may include:

- Assembled workforce.

- Potential contracts.

- Synergy benefits.

- Contingent assets.

- Expected renewals of reacquired rights.

In-process research and development projects

IAS 38.34 specifically mandates the separate recognition of an acquired in-process research and development project. Provisions for subsequent expenditure on such a project are covered in paragraphs IAS 38.42-43. If the project is never completed, it must be impaired.

Assets that the acquirer does not intend to use

Regardless of the acquirer’s intent to use or settle them, all acquired assets and liabilities should be recognised. Assets that the acquirer does not plan to use, or intends to use in a ‘suboptimal’ manner, must still be measured at their fair value, taking their highest and best use into consideration. Such as are sometimes referred to as ‘defensive assets’.

Immediate write-off of defensive assets after acquisition is not permitted as an impairment loss under IAS 36 can only be recognised when both the value in use and fair value fall below the asset’s carrying value (IFRS 3.B43). These assets will be removed from the accounts through amortisation over their useful life. Although determining the useful life of such an asset can be challenging, particularly if the acquirer does not plan to use it, an estimate must be made. Consider the following examples.

Example: Acquired brand that will not be used after the business combination

Acquiring Company (AC) acquired a competitor, Target Company (TC), which had a TC brand valued at $10 million. AC plans to withdraw the TC brand from the market within a year, intending to increase its original AC brand’s market share. Despite its intent to withdraw the brand, AC will maintain the legal rights to the TC brand indefinitely, preventing other companies from using it.

Despite this, AC recognises the TC brand at its fair value of $10 million. The economic benefits derived from the TC brand include preventing competitors from using it, thereby increasing AC’s profits. Therefore, the useful life of the brand extends beyond the year in which AC intends to withdraw it. This can be estimated as the period during which a significant competitor will fill the market void after TC’s withdrawal, influenced by factors such as entry barriers.

It is also important to note that, in most jurisdictions, a trademark registration will expire if the trademark has not been used to market products for a period of five years. Consequently, this five-year period can often serve as a reference point and may be considered the maximum amortisation period for the asset.

Example: Acquired software that will not be used after the business combination

AC acquired a competitor, TC, which had a customised client relationship management software (CRM) valued at $2 million. AC plans to migrate all TC customers to its CRM within 6 months, rendering the TC CRM obsolete. Given its customisation, AC will not be able to sell it to third parties.

Despite its short-term use, AC recognises the TC CRM at its fair value of $2 million. The software will be amortised over the 6-month period, corresponding with the duration AC will benefit from it.

Classification of acquired assets

At the acquisition date, the acquirer must classify or designate the acquired assets and assumed liabilities as per relevant IFRS guidelines (e.g., IFRS 9). This is done based on the terms and conditions existing at the business combination date (IFRS 3.15). However, an exception applies to lease contracts where the acquired entity is the lessor (IFRS 3.17).

Measurement of acquired assets and liabilities

The acquirer measures identifiable acquired assets and assumed liabilities at their acquisition-date fair values (IFRS 3.18-19), with a few exceptions. IFRS 3 does not specify how to measure fair value, as this is covered in IFRS 13.

Assets acquired in a business combination should be accounted for as a ‘fresh start’. This means that items such as allowance for credit losses or accumulated depreciation of fixed assets should not carry over in the acquirer’s financial statements (IFRS 3.B41).

Exceptions to recognition or measurement principles

Certain specified assets and liabilities are subject to exceptions to the recognition and measurement principles of IFRS 3. These exceptions are detailed in IFRS 3.21A-31A,54-57 and encompass the items discussed below.

Provisions and contingent liabilities

For a provision or a contingent liability that would fall under the scope of IAS 37 or IFRIC 21 if incurred separately, the acquirer applies IAS 37 or IFRIC 21 respectively to determine if a present obligation exists at the date of acquisition. Therefore, for this particular category of liabilities, the acquirer does not apply the Framework when evaluating recognition conditions (IFRS 3.21A-21C).

The acquirer must recognise assumed contingent liabilities for which a present obligation exists at fair value, even if the likelihood of outflow of resources is below 50% (IFRS 3.23). This approach differs from the ‘standard’ requirements of IAS 37, where a liability is recognised only when the probability of outflow of resources surpasses 50%. On the contrary, a contingent liability isn’t recognised if it’s a potential obligation only, whose existence is confirmed by the occurrence or non-occurrence of uncertain future events outside the control of the entity.

After the initial recognition, the contingent liability is measured at the higher of the following amounts:

- The amount that would be recognised in accordance with IAS 37.

- The amount initially recognised minus, if applicable, the cumulative amount of revenue recognised in accordance with IFRS 15.

This method of subsequent measurement prohibits the derecognition of a liability assumed in a business combination until it is settled or expires.

Contingent assets

The acquirer should not recognise contingent assets unless the acquiree has an unconditional right at the acquisition date (IFRS 3.23A). If an unconditional right exists, the asset is no longer considered contingent and should be recognised at fair value and subsequently measured in accordance with the appropriate IFRS, for instance, IFRS 9 (IFRS 3.BC276). Especially for non-contractual assets, assessing whether a right is unconditional can be challenging. In practice, if there’s any doubt, a separate asset is not recognised until all uncertainties are resolved.

Income tax

Deferred tax resulting from temporary differences and unused tax losses are accounted for as per IAS 12, i.e., not at fair value (IFRS 3.24-25). Deferred tax is recognised for assets and liabilities recognised at business combination as well as for fair value adjustments (IAS 12.19). Further discussion on business combinations and income tax accounting can be found in IAS 12.

Employee benefits

Employee benefits are recognised and measured in accordance with IAS 19, i.e., not at fair value (IFRS 3.26).

Indemnification assets

It’s common for the acquirer to shield themselves from uncertain outcomes of pending or potential issues related to the acquired entity. Prime examples are claims and litigation (C&L) where the seller pledges to reimburse the acquirer if the amounts to be paid as a result of C&L related to pre-acquisition events surpass a certain amount. In these cases, the acquirer has an indemnification asset, which should be measured (both at initial recognition and subsequently) on the same basis as the indemnified item (C&L liability in our example), taking credit risk into account (IFRS 3.27-28). Practically, such assets are valued at the same amount as the related liability, after accounting for any contractual indemnification limits.

Leases in which the acquiree is the lessee

Right-of-use assets and lease liabilities for leases where the acquiree is the lessee are recognised at the present value of the remaining lease payments, as if the acquired lease were a new lease at the acquisition date. The acquirer measures the right-of-use asset at the same amount as the lease liability, adjusted to reflect favourable or unfavourable lease terms compared with market terms (IFRS 3.28A). More information on leases can be found in IFRS 16.

Leases in which the acquiree is the lessor

Operating leases in which the acquiree is the lessor are not recognised separately if the terms of an operating lease are either favourable or unfavourable when compared with market terms. Instead, lease terms are considered when measuring the fair value of the asset subject to a lease (IFRS 3.B42).

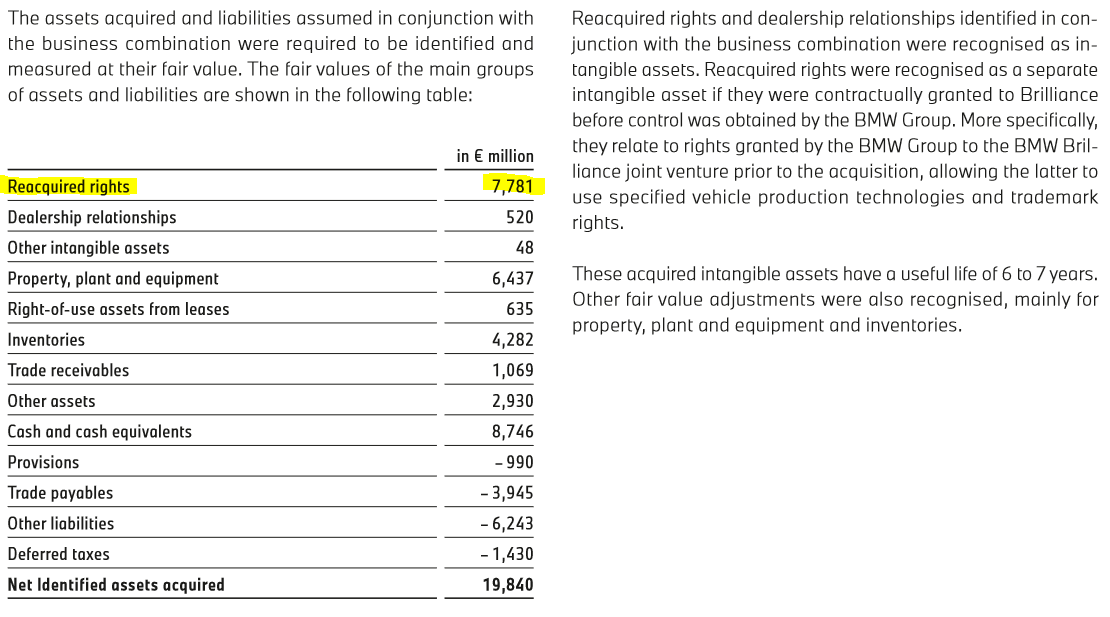

Reacquired rights

Occasionally, one of the assets acquired in a business combination is a right previously granted by the acquirer to the acquired entity. This often concerns the right to use an asset by the acquiree, such as a brand (which may not be recognised in the acquirer’s statement of financial position). This right is recognised as an asset in a business combination, but the fair value measurement should be based only on the remaining contractual term, disregarding possible contract renewals (IFRS 3.29, B35). A reacquired right should be amortised over the remaining contractual period.

The following extract illustrates the recognition of EUR 7.8 billion worth of reacquired rights by BMW as part of gaining control over its Chinese joint venture (BMW Brilliance) in 2022:

If the terms of the reacquired right were favourable or unfavourable in comparison to market terms, a settlement gain or loss on the pre-existing relationship should be recognised (IFRS 3.B36).

Share-based payments

Please refer to a separate section discussing share-based payment arrangements in the context of business combinations.

Assets held for sale

Acquired assets held for sale should be initially measured at fair value less costs to sell, in accordance with IFRS 5 (IFRS 3.31).

Insurance contracts

Groups of contracts within the scope of IFRS 17, and any assets for insurance acquisition cash flows as defined in IFRS 17, should be measured in accordance with IFRS 17.39 and IFRS 17.B93–B95F (IFRS 3.31A).

Recognising and measuring goodwill

Goodwill represents future economic benefits arising from assets acquired in a business combination that are not individually identified and separately recognised. The main components of goodwill are the going concern element of the acquiree’s existing business, including the assembled workforce, and the expected synergies and other benefits from combining the acquirer’s and acquiree’s net assets and businesses (refer to BC313+ for further discussion). IFRS 3.B64(e) requires a qualitative description of the factors that comprise the recognised goodwill.

Goodwill is measured as a residual as the difference between (IFRS 3.32):

- Consideration transferred,

- Non-controlling interest in the acquired entity,

- Fair value of the acquirer’s previously held equity interest in the acquired entity, and

- Net identifiable assets acquired and liabilities assumed.

Goodwill is not amortised but is subject to impairment testing at least annually, as per IAS 36 requirements (IFRS 3.B63(a)). If goodwill relates to an acquisition of a foreign subsidiary, it is expressed in the functional currency of this subsidiary and then subsequently translated as per IAS 21 requirements.

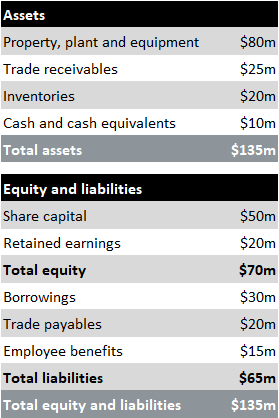

Example: Illustration of calculation of goodwill

Acquirer Company (AC) purchases an 80% shareholding of Target Company (TC) for $100m. TC holds the following assets and liabilities as of the acquisition date:

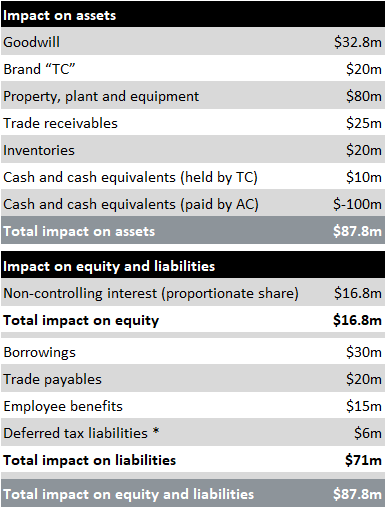

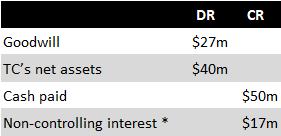

AC determines that the fair value of assets and liabilities of TC equals their net book value as presented in the statement of financial position of TC. Furthermore, AC recognises that the brand of TC is an identifiable asset to be recognised on acquisition. It is an internally generated brand, hence not previously recognised by TC. The fair value of the ‘TC’ brand is estimated at $20m. The impact of this acquisition on the consolidated financial statements of AC is as follows:

* Deferred tax liabilities relate to brand “TC” (tax rate assumed at 30%).

The formula for goodwill calculation may yield a negative number resulting in a gain on a bargain purchase.

Consideration transferred and contingent consideration

Transferred consideration is the aggregate of the fair values of the following (IFRS 3.37):

- Assets transferred by the acquirer.

- Liabilities to former owners incurred by the acquirer.

- Equity interests issued by the acquirer.

Typically, the consideration is paid in cash. If the acquirer transfers other assets, they must be remeasured to their fair value on the acquisition date. Any difference between the fair value and the net book value is immediately recognised in profit or loss. However, this rule doesn’t apply to assets transferred to the acquired entity, as they remain under the control of the acquirer after the acquisition (IFRS 3.38).

Occasionally, the amount of consideration depends on future events. This type of consideration is known as contingent consideration and should also be recognised at fair value as part of the business combination. The general criteria of IFRS 13 for determining the fair value of liabilities also apply to contingent consideration. It’s worth noting that contingent consideration dependent on the ongoing employment of the selling shareholder, also known as ‘earn-outs’, should be excluded from acquisition accounting and treated as an expense in future periods (see IFRS 3.B55(a) and this agenda decision).

If the total contingent consideration is paid, but the acquirer retains the right to a partial refund, this right is recognised as an asset at fair value, reducing the total consideration (IFRS 3.39-40).

Changes in the fair value of contingent consideration resulting from post-acquisition events (e.g. achieving performance targets) are recognised in profit or loss. Its classification in the income statement isn’t covered in IFRS, but it’s typically presented as part of operating income.

Contingent consideration classified as equity under IAS 32 isn’t subsequently remeasured, and its settlement is accounted for within equity (IFRS 3.58). Refer to IAS 32 for the equity vs liability distinction.

The acquirer sometimes reserves the right to defer part of the consideration for a specific period, typically in the event of a breach of the share purchase agreement by the seller (e.g. non-disclosure of a claim against the acquired entity). This is commonly known as deferred consideration. Changes or adjustments to deferred consideration generally arise from additional information about facts and circumstances existing at the acquisition date and are treated as measurement period adjustments.

Often, the consideration depends on the working capital of the acquired entity at the acquisition date, determined sometime post-acquisition. Any changes to consideration resulting from the target entity’s working capital balances at the acquisition date are treated as measurement period adjustments.

There may be instances where the acquirer obtains control without transferring consideration, such as when the target entity repurchases its own shares or when certain rights held by previous controlling interests expire. All IFRS 3 requirements also apply to these types of business combinations (IFRS 3.43-44).

Measuring non-controlling interest

IFRS 3 offers two measurement bases for non-controlling interest (NCI):

- Fair value, or

- The present ownership instruments’ proportionate share of acquiree’s identifiable net assets (IFRS 3.19).

It should be noted that the second option is only applicable to ‘ordinary’ NCI, that is, equity instruments that are present ownership instruments and entitle their holders to a proportionate share of the acquiree’s net assets in the event of liquidation. For example, preference shares that give their holders a disproportionately higher or lower share of the acquiree’s net assets in the event of liquidation must be measured at fair value. The same rule applies to share warrants or equity components of compound financial instruments.

The fair value of NCI should be determined using valuation techniques outlined in IFRS 13. If shares of the acquiree are quoted, their fair value is calculated as ‘price x quantity’. However, this is not often the case, and it’s vital to note that the fair value of NCI is typically lower than implied by simple reference to the controlling interest of the acquirer (e.g. a 30% NCI is worth less than half the value of a 60% controlling stake). This is due to the so-called control premium paid by the acquirer (IFRS 3.B44-B45).

The choice of measurement basis can be made on a case-by-case basis and is not a ‘fixed’ accounting policy. This decision has three major implications (IFRS 3.BC217-BC218):

- An NCI measured at fair value will generally be higher than when measured at the proportionate share of identifiable net assets – this consequently impacts goodwill, making it also higher (see illustrative example below).

- When an impairment loss is applied to goodwill, its amount will be higher when the NCI is measured at fair value. This ‘additional’ impairment loss is allocated to the NCI. Also, refer to the section on goodwill and non-controlling interests within IAS 36.

- When the NCI is later reduced due to the parent company purchasing additional shares, such a transaction is accounted for as an equity transaction under IFRS 10. The higher the NCI is valued before this transaction, the smaller the reduction in consolidated equity after the transaction.

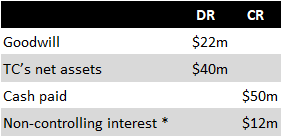

Example: Two methods of measuring non-controlling interest

The Acquirer Company (AC) purchases a 70% shareholding in the Target Company (TC) for $50m. The fair value of the TC’s net identifiable assets at the time of acquisition is $40m. The fair value of the remaining 30% stake in TC is $17m.

The impact of this acquisition on the consolidated financial statements of AC is as follows:

Method 1: Non-controlling interest measured at fair value:

* Measured at fair value under IFRS 13, not equivalent to 30% x $40m.

Method 2: Non-controlling interest measured at present ownership interest:

* Calculated as 30% x $40m.

Previously held equity interest in the acquiree

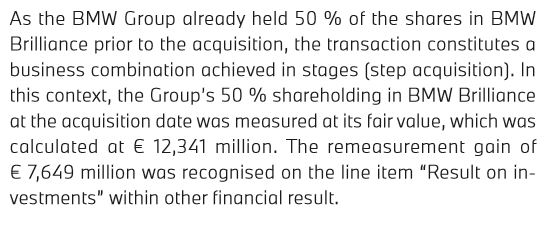

An acquirer might gain control of an acquiree in which it had an existing equity interest at the time of obtaining control. For instance, Acquirer Company (AC) holds a 30% stake in Target Company (TC). It then secures an additional 40%, aggregating to a 70% interest and thereby establishing control over TC. This type of transaction is commonly known as a ‘step acquisition’ or ‘piecemeal acquisition’. In such instances, the 30% stake should be remeasured to its fair value at the date of acquisition. Any difference between this fair value at the date of obtaining control and its carrying amount must be recognised as a gain or loss in P/L or OCI. This is treated as if the previously held interest was sold, including the recycling of accumulated OCI reserves to profit or loss, if applicable (IFRS 3.41-42).

The fair value of the previously held equity interest in the acquiree is then derecognised and factored into the goodwill calculation (as though it was part of the consideration transferred).

If the acquirer recognised changes in the value of its equity interest in the acquiree in OCI prior to the business combination (for example, as a share in the OCI of associates), those amounts should be recognised on the same basis as would have been required if the acquirer had directly disposed of the previously held equity interest. This indicates they may or may not need to be recycled to P/L.

The excerpt below illustrates the recognition of a EUR 7.6 billion gain by BMW from the remeasurement of its previously held 50% stake in its Chinese joint venture:

Gain on bargain purchase

The formula for calculating goodwill may result in a negative figure. In such scenarios, a one-off gain on a bargain purchase is recognised in profit or loss. However, before that, IFRS 3 requires a reassessment and re-evaluation of all the steps undertaken in the business acquisition accounting (IFRS 3.34-36). Moreover, IFRS 3.B64n(ii) mandates the disclosure of the reasons why the transaction resulted in a gain, for instance, the seller facing liquidity pressure.

In practice, gains on bargain purchases are rare. If the initial calculations show such a gain, the fair valuation of assets may need to be reduced, or alternatively, the fair valuation of liabilities increased. This re-evaluation may be more favourable to the management of the acquirer, as one-off gains are typically excluded from KPIs used by investors. Furthermore, a lower value of assets recognised in a business combination results in reduced depreciation and amortisation charges in post-acquisition P/L or increased gains on subsequent disposal of individual assets.

Overpayments

IFRS 3 does not address overpayments because the IASB considers such occurrences to be rare and virtually undetectable. In any case, an acquirer cannot recognise any loss on acquisition due to overpayment, meaning any overpayment will increase the value of goodwill. In theory, an overpayment will trigger an impairment loss during the next impairment test (IFRS 3.BC382).

Acquisition-related costs

Acquisition-related costs, like professional fees, should be expensed in the periods when the costs are incurred and the services are received. The costs to issue debt or equity securities should be recognised following IAS 32 and IFRS 9 (IFRS 3.53).

Acquirer’s acquisition-related costs borne by the acquiree or selling shareholders should also be accounted for as an expense by the acquirer (IFRS 3.52(c)).

Measurement period

The complexity of business combinations and the often limited access to the financial data of the acquiree before the acquisition can render the completion of acquisition accounting unfeasible before the reporting date. IFRS 3 acknowledges these limitations and introduces the concept of the measurement period. It is a time frame during which the acquirer can adjust acquisition accounting if it obtains new information about facts and circumstances that existed at the acquisition date. These adjustments should be applied retrospectively, along with changes in comparative data, such as adjustments to depreciation charges.

The measurement period ends when the acquirer obtains the information it was seeking about facts and circumstances that existed at the acquisition date or learns that further information is unobtainable. However, the measurement period must not exceed one year from the acquisition date (IFRS 3.45-50).

There is no relief regarding the timing of an impairment test for goodwill during the measurement period. As a result, CGUs to which newly recognised goodwill has been allocated should undergo an impairment test before the end of the first annual period during which the business combination occurred (IAS 36.96).

Determining what is part of the business combination transaction

IFRS 3.51-52; B50-B62 offer guidance on pre-existing relationships and transactions executed concurrently with business combinations, which are essentially separate transactions. Any transactions that are mainly to the benefit of the acquirer or the combined entity, rather than the acquiree (or its former owners) before the combination, are likely to be distinct transactions. These should be accounted for separately from the business combination. IFRS 3.52 provides examples of such transactions, which include:

- Settlements of pre-existing relationships between the acquirer and acquiree.

- Remuneration to employees or former owners of the acquiree for future services (also referred to in IFRS 3.B55(a) and this agenda decision).

To decide whether a transaction should be accounted separately from a business combination, consider factors outlined in IFRS 3.B50. These include the reasons for the transaction, who initiated it, and the timing of the transaction. IFRS 3.B54-B55 offer further guidance on contingent payments to employees or former owners of the acquiree to determine whether these payments are for future service or a contingent consideration for the acquiree.

If a business combination settles a pre-existing relationship, the acquirer recognises a gain or loss as follows (IFRS 3.B52):

- For a non-contractual pre-existing relationship (such as a lawsuit), it is measured at fair value.

- For a contractual pre-existing relationship, it is the lesser of:

- the amount by which the contract is favourable or unfavourable from the acquirer’s perspective compared with terms for current market transactions for similar items,

- the amount of any stated settlement terms in the contract available to the counterparty for whom the contract is unfavourable (see an example in IFRS 3.IE54-IE57).

If a business combination contract stipulates that the acquirer repay the acquiree’s debt at the acquisition date, or if the acquirer decides to do so voluntarily, this should be excluded from the business combination accounting if the debt wasn’t owed to the selling shareholders. Instead, the acquirer should recognise these liabilities as part of the net identifiable assets acquired at the acquisition date and consider the repayment a post-acquisition event.

Any cash flows linked to the business combination, but not part of the exchange for control over the acquiree, should be excluded from investing cash flows if they do not result in a recognised asset.

Example: Settlement of pre-existing lawsuit

Acquirer Company (AC) purchased Target Company (TC) for $100m. Before the acquisition, TC filed a lawsuit against AC for contract breaches, demanding $10m. AC did not recognise any provision as they believed the probability of cash outflow for this case was only 20%, with the fair value of this liability estimated at $2m. As this claim becomes an intragroup claim after the business combination, it should be effectively considered settled in AC’s consolidated financial statements. AC should account for this $2m separately as a settlement cost in P/L, and the remaining $98m paid should be accounted for as consideration for acquiring TC.

Example: Settlement of pre-existing contract

Acquirer Company (AC) purchased Target Company (TC) for $100m. Before the acquisition, TC was a supplier for AC. At the acquisition date, they had a valid supply contract for product Y at fixed prices, with the remaining contractual term being 3 years. As the prices of the product Y dropped in the market since the contract’s initiation, it was unfavourable to AC at the acquisition date. AC was contractually committed to order a minimum of 1,000 pieces of Y each year until the contract’s expiration. Terminating the contract would require AC to pay a $5m penalty to TC.

The fair value of the contract from TC’s perspective was $7m, with $3m attributable to above-market fixed pricing, and the remaining $4m to profits expected at-market prices. In other words, the contract was unfavourable to AC by $3m.

As part of the acquisition accounting, AC recognises the $3m of consideration paid as an expense related to the settlement of the pre-existing contract. The remaining $4m, corresponding to at-market prices, forms a part of goodwill (IFRS 3.IE56).

Acquisition of individual assets

In the event of acquiring assets that do not constitute a business, the acquirer recognises individual identifiable assets (and liabilities) by allocating the acquisition cost based on their relative fair values at the purchase date. Goodwill is not recognised in such cases (IFRS 3.2(b)).

Identifying the acquirer

Entities are required to identify the acquirer in every business combination (IFRS 3.6-7). The acquirer is the entity that obtains control over the acquiree. Here, control is understood as defined by IFRS 10. Generally, it is quite clear to establish which entity is the acquirer. It is usually the one that transfers cash and/or incurs liabilities and is significantly larger (in terms of assets, revenue etc.) than the other parties involved in the transaction. Further guidance on identifying the acquirer is provided in paragraphs IFRS 3.B14-B18.

Reverse acquisitions

Guidance on a specific type of business combination called reverse acquisitions, or reverse takeovers, or reverse IPO (initial public offering), is provided in paragraphs IFRS 3.B19-B27. A reverse acquisition happens when a private company, typically, takes over a publicly-traded company. First, the private company’s owners gain control over the public company by purchasing a sufficient number of shares on the market. Next, the public company ‘acquires’ the private company by issuing its shares to the private company’s owners. Finally, the two entities merge into one, or the private company’s operations are transferred to the public company. The primary benefit for the private company’s owners is that they can take their business public without undergoing a costly and lengthy IPO process.

While the public company is usually the legal acquirer as it issues shares to owners of the private company in exchange for the private company’s shares, if guidance in IFRS 3.B14-B18 suggests that the private company is the de facto acquirer, the business combination should be accounted for with the private company as the acquirer.

Determining the acquisition date

The acquisition date is the date when the acquirer obtains control over the acquiree. Generally, it’s easy to determine the acquisition date, which is typically the ‘closing date’, the date when the consideration is transferred to the seller. However, IFRS 3 acknowledges cases where control is obtained either before or after the closing date (IFRS 3.8-9).

Example: Determining the acquisition date

Acquirer Company (AC) acquired Target Company (TC). The following milestones are related to the transaction:

- The agreement was signed on 9 February, specifying that the effective date of the transaction was 31 March. Specifically:

– TC’s selling shareholders were not entitled to dividends or other equity distributions after 31 March,

– the price for TC’s shares was linked to TC’s working capital balances at 31 March, and

– TC’s management had to seek AC’s written consent for any strategic business decisions after 31 March. - The acquisition of TC was subject to shareholder approval at AC’s AGM on 17 May.

- After AGM’s approval was obtained, the price for TC’s shares was paid on 24 May and TC’s new board of directors was appointed by AC shortly thereafter.

- The change in ownership became legally binding on 27 June when the transaction was recorded in a public company register.

In this scenario, control was likely obtained on 24 May, i.e., when the payment was made. Despite the stated effective date of the transaction, AC did not obtain power over TC on 31 March. In particular, AC did not have existing rights that would give it the current ability to direct TC’s relevant activities at that date. The requirement of TC’s management to seek AC’s approval for strategic business decisions was a protective right only.

If there are any legal procedures to be fulfilled after the acquisition, they are usually virtually certain to be successfully processed and control over TC is usually passed by TC’s former owners to AC before that date. However, if the procedures to be fulfilled are substantive, e.g., consent of competition authorities, the acquisition date can only be determined after the consent is received.

In practice, the acquisition date for accounting purposes is often set at the month’s closing date, as it is easier to determine the value of assets and liabilities acquired. This approach is explicitly allowed by IFRS 3.BC110 provided that there are no material events between the month’s closing date and the actual acquisition date.

Other accounting methods

Acquisition method is the only method allowed under IFRS 3. Methods such as pooling of interest, fresh start, or others are not permissible under IFRS 3.

Certain GAAP allow the use of the acquirer’s basis of accounting in the acquiree’s separate financial statements. For instance, fair value adjustments recognised in consolidated financial statements are ‘pushed down’ to the separate financial statements of the acquiree. However, ‘pushdown accounting’ is not permitted under IFRS. More information about pushdown accounting can be found in Deloitte’s publications.

More about IFRS 3

See other pages relating to IFRS 3:

Scope of IFRS 3

Disclosure Requirements for Business Combinations