Consolidated financial statements present assets, liabilities, equity, income, expenses, and cash flows of a parent entity and its subsidiaries as if they were a single economic entity. These statements are prepared in accordance with IFRS 10.

The terms ‘group’, ‘parent’, and ‘subsidiary’ are used in this context to refer to the entities involved. A parent is an entity that exercises control over one or more entities. An entity controlled by a parent is referred to as a subsidiary. A parent, together with all its subsidiaries, forms a group. The notion of ‘control’ is central to this arrangement.

Let’s dive in.

Control

According to IFRS 10.6-8, an investor controls an investee (another entity) if it has:

- Power over the investee,

- Exposure, or rights, to variable returns from its involvement with the investee, and

- The ability to use its power over the investee to affect the amount of the investor’s returns (principal vs agent consideration).

The presence of control should be reassessed whenever relevant facts or circumstances change (IFRS 10.8;B80-B85). IFRS 10 provides a comprehensive definition of control, ensuring that no entity controlled by the reporting entity is omitted from its consolidated financial statements. This is particularly crucial when an entity’s operations are not directed through voting rights.

The sections that follow elaborate on these criteria for determining control.

--Too many IFRS updates? I know the feeling! That's why I created Reporting Period. It's a concise monthly summary of IFRS developments and Big 4 insights for accounting professionals. It's completely free, with zero spam, and you can unsubscribe anytime with one click. Interested? Leave your email below:

Power

Power arises from rights that give the investor current ability to direct relevant activities of an investee. Power typically comes from voting rights attached to shares, but it can also originate from other sources, such as contractual arrangements (IFRS 10.10-13). This is particularly relevant for entities where key decision-making is predetermined at the formation of the investee, known as ‘structured entities’, ‘special purpose entities’, or ‘variable interest entities’.

Relevant activities

‘Relevant activities’ are operations that significantly impact the investee’s returns. IFRS 10.B11 provides examples of such activities, including:

- Sale and purchase of goods or services,

- Management of financial assets,

- Selection, acquisition, or disposal of assets,

- Research and development of new products or processes, and

- Decisions related to funding structure or obtaining financing.

Majority of voting rights

Holding the majority of the voting rights generally gives an investor power over the investee. This applies in situations where the investee’s relevant activities are directed by a vote of the majority shareholder, or when a majority of the members of the investee’s governing body that directs the relevant activities are appointed by a vote of the majority shareholder (IFRS 10.B35). In fact, for typical entities that are controlled through voting rights, possessing the majority of these rights is sufficient for a parent to ascertain that it controls the investee.

However, there may be situations where an investor with majority voting rights lacks the practical ability to exercise them. Such rights are considered non-substantive (see IFRS 10.B22-B25) and do not provide the investor with power over the investee (IFRS 10.B36-B37).

Minority of voting rights

An investor can exert power over an investee without possessing the majority of the voting rights, a situation often called ‘de facto control’. Such control can be exercised through (IFRS 10.B38-50):

- Investor’s voting rights (e.g., when other vote holders are dispersed and unable to collectively outvote the investor),

- A contractual arrangement between the investor and other vote holders,

- Rights derived from other contractual arrangements,

- Potential voting rights.

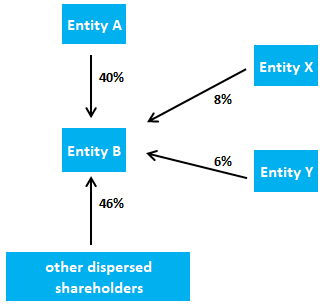

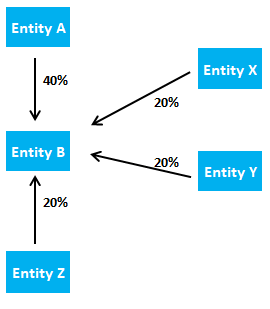

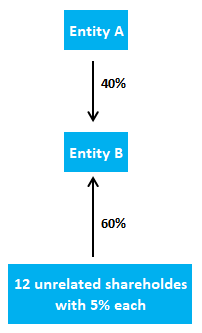

Consider an example where Entity A holds a 40% interest in Entity B:

Example: Minority of the voting rights vs power over the investee

Scenario #1

Entity B is listed on a stock exchange. Two large investors hold more than 5% of the voting rights each, with the remaining shares dispersed among unknown individual shareholders.

Scenario #2

Entity B is a privately-owned company with the following shareholding structure:

Scenario #3

Entity B is a privately-owned company with a different shareholding structure:

In Scenario 1, Entity A has power over Entity B (assuming the criteria of IFRS 10.B35 are met) since the other shareholders are too dispersed to collectively outvote Entity A. Conversely, in Scenario 2, Entity A does not have power over Entity B, as other shareholders could potentially unite and outvote Entity A. This conclusion remains valid even if Entities X, Y, and Z have been passive investors so far.

Determining whether Entity A has power over Entity B in Scenario 3 is more complex. Here, other factors need to be assessed as per IFRS 10.B42(b)-(d), such as the level of active participation of other shareholders at annual general meetings, regardless of whether they vote in line with Entity A.

If, after considering all available evidence, it is still unclear whether the investor has power over the investee, the investor should not consolidate the investee (IFRS 12.B46, BC110).

Potential voting rights

Potential voting rights, which could stem from convertible instruments, options, or other mechanisms, grant the holder the right to obtain voting rights of an investee. They are considered when assessing control only if they are substantive (IFRS 10.B22-B25). Potential voting rights are covered in IFRS 12.B47-50. It’s crucial to understand that potential voting rights can grant power to a minority shareholder as well as strip power from a majority shareholder.

Multiple parties with decision-making rights

In situations where two or more unrelated investors each have unilateral decision-making rights over different activities of an investee that significantly affect the investee’s returns, control belongs to the investor who has the ability to direct the most consequential activities of the investee. Thus, power is assigned to the party most closely resembling the controlling entity (IFRS 10.BC85-BC92).

In cases where multiple parties have unilateral decision-making rights over different activities, it may be possible that each party controls only certain assets or a ‘ring-fenced’ segment of a larger entity. That portion of an investee should be consolidated as if it were a separate entity or a ‘silo’. Guidelines for such situations can be found in IFRS 10.B76-B79.

Purpose and design of the investee

When assessing control, the purpose and design of the investee should be taken into account. An investee may be structured in such a way that voting rights are not the primary determinant of control (IFRS 10.B5-B8;B51-B54). This criterion is particularly applicable in assessing control over ‘special purpose entities’ or structured entities, i.e., entities designed so that voting or similar rights do not primarily dictate who controls the entity. For instance, voting rights might apply only to administrative tasks, while the relevant activities are directed by contractual agreements. Structured entities often engage in restricted activities, have a clear and specific objective, and require subordinate financial support (IFRS 12.B21-B22).

Protective rights

Protective rights are structured to safeguard the interests of an investor or another party such as a creditor. Importantly, these rights do not give power over the investee (IFRS 10.14). IFRS 10.B28 provides examples of protective rights:

- Lender’s right to restrict the borrower from undertaking activities that could significantly alter the borrower’s credit risk to the lender’s disadvantage,

- Lender’s right to seize the borrower’s assets if the borrower fails to meet specified loan repayment conditions,

- The right of a non-controlling interest holder in an investee to approve capital expenditure exceeding the routine business requirements, or to approve the issuance of equity or debt instruments.

The presence of protective rights held by external parties does not preclude an investor from having control over an investee. Veto rights are often protective in nature, but not always. For instance, if the veto applies to modifications in relevant activities that significantly affect investee returns for the investor’s benefit, it could be considered as a source of power over the investee (IFRS 10.B15(d)). This concept also applies to scenarios involving bankruptcy proceedings or covenant breaches.

Bankruptcy proceedings or breach of covenants

The Interpretations Committee deliberated the question of reassessing control when facts and circumstances change, changing the nature of previously protective rights (e.g., a covenant breach in a loan arrangement that results in borrower default). The necessity to reassess control whenever relevant facts and circumstances change is emphasized in IFRS 10.8;B80-B85. The Committee noted that IFRS 10 does not exempt any rights from this requirement. Thus, a covenant breach, resulting in rights becoming exercisable, denotes a change in facts and circumstances.

As a result, a protective right can transform into a right that grants power once it becomes exercisable. This situation commonly arises when evaluating control over entities encountering financial difficulties and entering bankruptcy proceedings. In such cases, creditors often acquire the right to direct the entity’s relevant activities for their benefit (i.e., debt repayment), which could lead to the conclusion that control over the investee has transferred to them.

Franchise agreements

Franchise agreements are detailed in IFRS 10.B29-B33. Generally, a franchisor does not have power over the franchisee, as the franchisor’s rights aim to protect the franchise brand rather than direct activities significantly impacting the franchisee’s returns.

Exposure, or rights, to variable returns

An investor is exposed, or possesses rights to, variable returns from their involvement with an investee when their returns have the potential to fluctuate based on the investee’s performance (IFRS 10.15). While only one investor can control an investee, it’s possible for other parties, such as non-controlling interest holders, to benefit from the investee’s returns (IFRS 10.16).

Variable returns may include (IFRS 10.B57):

- Dividends, interest, and other distributions of economic benefits,

- Changes in the value of the investor’s investment in an investee,

- Fees for servicing an investee’s assets or liabilities,

- Fees and potential losses from providing credit or liquidity support,

- Access to future liquidity an investor gains from their involvement with the investee,

- Residual interests in the investee’s assets and liabilities upon its liquidation,

- Tax benefits,

- Reputational risk (IFRS 10.BC37-BC39),

- Returns that aren’t accessible to other interest holders, such as benefits of synergy, procurement of scarce products, access to proprietary knowledge, or limitation of certain operations or assets to enhance the value of the investor’s other assets.

As we observe, credit risk is a factor when considering variable returns, which means fixed-interest financing also results in exposure to variable returns.

Link between power and returns (principal vs agent)

A parent company must be able to use its power to influence the returns from an investee. Entities acting as agents do not control an investee (IFRS 10.17-18). However, if another party delegates decision-making rights to an agent, it is the investor with these rights who maintains control. Essentially, decision-making rights given to an agent are considered as being held directly by the investor. These principal-agent relationships are frequent in industries such as asset management, real estate, and construction.

IFRS 10.B60 details factors determining whether a decision-maker is purely an agent:

- Extent and independence of the decision-making authority over the investee (IFRS 10.B62-B63),

- Removal (‘kick-out’) rights and restrictive rights held by other parties (IFRS 10.B64-B67),

- Remuneration entitled to the decision-maker, and its size and variability relative to the expected returns from the investee’s activities (IFRS 10.B68-B70),

- Decision-maker’s exposure to variability of returns from other interests held in the investee (IFRS 10.B71-B72).

Additionally, relationships between parties also require consideration (IFRS 10.B73-B75).

When an investor holds decision-making rights but perceives itself as an agent, it should evaluate whether it has significant influence over the investee.

Consolidated financial statements

Consolidated financial statements of a group should be prepared applying uniform accounting policies (IFRS 10.19,B86-B87). Each parent entity is required to prepare consolidated financial statements unless exemptions outlined in IFRS 10 are applicable.

Consolidation procedures are typically executed via specialised software wherein subsidiaries input their data for consolidation. As per IFRS 10.B93, the period between the financial statement dates of the subsidiary and the group should not exceed three months. Consequently, if a subsidiary’s reporting date differs from that of the parent company, it needs to provide additional information to ensure that this time gap does not influence the consolidated financial statements.

Consolidation of a subsidiary initiates when control is gained and concludes when control is lost (IFRS 10.20,B88).

Non-controlling interest

Non-controlling interest (NCI) represents the existing interest in a subsidiary that is not directly or indirectly attributable to a parent. For instance, if a parent owns 80% of the shares in a subsidiary, the residual 20% is the NCI. This was formerly referred to as ‘minority interest’, a term still occasionally used by accounting practitioners.

NCI should be presented within equity in the consolidated statement of the financial position, separate from the equity attributable to owners of the parent (IFRS 10.22). A parent entity, in presenting consolidated financial statements, should allocate the profit or loss and total comprehensive income between the owners of the parent and the non-controlling interests. Non-controlling interests can maintain a negative balance due to cumulative losses attributed to them (IFRS 10.B94), even in the absence of an obligation to invest further to cover these losses (IFRS 10.BCZ160-BCZ167). The allocation of profit or loss and total comprehensive income should solely rely on existing ownership interests, without considering the potential execution or conversion of potential voting rights and other derivatives (IFRS 10.B89-B90).

Changes in a parent’s ownership interest in a subsidiary that don’t result in loss of control are treated as equity transactions. These changes don’t impact the profit or loss, recognised assets (including goodwill), or liabilities (IFRS 10.23,B96,BCZ168–BCZ179). Prior to the introduction of IFRS 10, the acquisition of a non-controlling interest often led to the parent recognising additional goodwill (prohibited under IFRS 10).

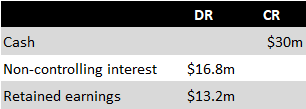

Example: Acquisition of non-controlling interest

Our starting point is an example provided in IFRS 3 for the calculation of goodwill. Following the acquisition of the Target Company (TC), Acquirer Company (AC) recognised $16.8m of non-controlling interest (NCI). Assuming that after a year, AC acquires the remaining 20% shareholding in TC for $30m (entirely paid in cash). For simplicity, we will also assume that the value of NCI remained constant after the acquisition date (usually, NCI changes due to dividend payments, profit generated by TC, etc.).

The entries made in the consolidated financial statements of TC are as follows:

As seen above, despite AC paying more than the previously reported amount of NCI in the consolidated statement of the financial position, there is no impact on profit or loss.

Loss of control

When a parent company loses control of a subsidiary, IFRS 10.25, B98-B99 stipulate the following accounting approach:

- Derecognise all assets (including goodwill) and liabilities of the former subsidiary at their carrying amount,

- Derecognise the non-controlling interest,

- Recognise the received consideration at fair value,

- Recognise any retained investment in the former subsidiary at fair value,

- Recognise any resulting difference as a gain or loss in profit or loss attributable to the parent.

Furthermore, when control of a subsidiary is lost, all amounts previously recognised in OCI concerning that subsidiary should be accounted for as if the parent had directly disposed of the related assets or liabilities. This means these amounts should be transferred to P/L as a reclassification adjustment (for instance, in the case of foreign currency translation) or directly to retained earnings (IFRS 10.B99).

Additionally, accounting for a former subsidiary becoming a joint operation is discussed in IFRS 11.

Scope of IFRS 10

IFRS 10 is applicable to all entities acting as a parent, except for those meeting the scope exemption criteria detailed in IFRS 10.4-4B. Consequently, a parent company controlling a subgroup, which is consolidated at a higher level under IFRS and not publicly listed, is not required to prepare consolidated financial statements if all the conditions in IFRS 10.4(a) are fulfilled. There are different perspectives regarding the applicability of this exemption by a subsidiary whose parent prepares consolidated financial statements under local GAAP that align closely with IFRS (e.g., ‘IFRS as adopted by the EU’). In my view, this exemption can be applied provided that any discrepancies with IFRS as issued by the IASB are negligible.

One of the conditions for exemption relates to the non-controlling interests being notified and not opposing the non-preparation of consolidated financial statements. IFRS 10 does not impose a time limit for non-controlling interests to raise objections so it’s prudent to actively obtain the approval of non-controlling interests when seeking an exemption from preparing consolidated financial statements.

Note that local laws might mandate the presentation of consolidated financial statements even if an IFRS 10 exemption applies.

In the past, under IFRS and certain local GAAPs, prominent exemptions from consolidation were related to subsidiaries when control was temporary, the subsidiary’s activities differed significantly from the parent, or there were long-term restrictions on the transfer of funds to the parent. IFRS 10 currently does not incorporate these exemptions from consolidation.

When control (or significant influence) is shared among two or more investors, the investee is not a subsidiary, and other relevant IFRS standards should be applied (i.e., IFRS 11, IAS 28, or IFRS 9). IFRS 3 covers the accounting for business combinations (i.e., gaining control of one or more businesses).

Exemption for investment entities

Investment entities are granted additional exemptions from consolidation (and business combination accounting). They are required to measure all of their subsidiaries at fair value through profit or loss according to IFRS 9 (IFRS 10.4B and IFRS 10.31-33). An investment entity (IFRS 10.27) is an entity that:

- Secures funds from one or more investors with the intention of offering those investors investment management services,

- Commits to its investor(s) that its business purpose is solely to invest funds for returns from capital appreciation, investment income, or both, and

- Measures and evaluates the performance of substantially all of its investments on a fair value basis.

Guidance on determining whether an entity is an investment entity can be found in IFRS 10.28, B85A-W, IE1-IE15. The accounting implications of an entity becoming or ceasing to be an investment entity are detailed in IFRS 10.B100-B101.

Exemption for employee benefit plans

IFRS 10.4A specifies that IFRS 10 does not apply to post-employment benefit plans or other long-term employee benefit plans to which IAS 19 is applicable. However, the phrasing isn’t entirely clear as to whether this exemption relates to financial statements prepared by employee benefit plans or to employers who need to consider whether such plans should be consolidated. It’s widely accepted in practice that this exemption applies to the latter case. In other words, employers are not required to assess whether employee benefit plans should be treated as subsidiaries and thus need to be consolidated.

Subsidiaries acquired exclusively with a view to resale

There is no consolidation exemption for subsidiaries acquired solely for resale. Nevertheless, these can be classified as held for sale and discontinued operations under IFRS 5, which can considerably simplify the determination of fair value and consolidation. Specifically, the acquirer would not need to measure individual assets and liabilities at fair value, as all assets and liabilities will be presented in one line (one line for assets and another for liabilities). Any breakdown of these assets and liabilities is not required (IFRS 5.39). P/L consolidation will also be presented in a single line, representing discontinued operations. Example 13 accompanying IFRS 5 illustrates this approach. More discussion on the classification of assets and disposal groups acquired solely for resale can be found under IFRS 5.

Disclosure

IFRS 12 is an exhaustive standard that encapsulates all disclosure requirements relating to interests in other entities. In addition, paragraphs IAS 7.39 and onwards encompass substantial disclosure requirements regarding cash flows from changes in ownership interests in subsidiaries and other businesses.