Factoring is a financial transaction where a business sells its outstanding accounts receivable to a third party, known as a factor, at a discounted price rather than waiting to be paid based on the original terms. There are two primary types of factoring:

- Recourse factoring: Should the original customer (debtor) fail to settle the invoice, the responsibility remains with the seller. In such cases, the factor can seek ‘recourse’ from the seller to recover the unpaid amount.

- Non-recourse factoring: Here, the factor takes on the risk of non-payment. If the debtor doesn’t pay, the factor absorbs the loss.

Interestingly, though factoring of receivables is the predominant transaction among non-financial entities necessitating assessment per the IFRS 9 derecognition criteria, IFRS 9 doesn’t provide any examples that directly mention factoring.

Example: Factoring with partial recourse that qualifies for derecognition

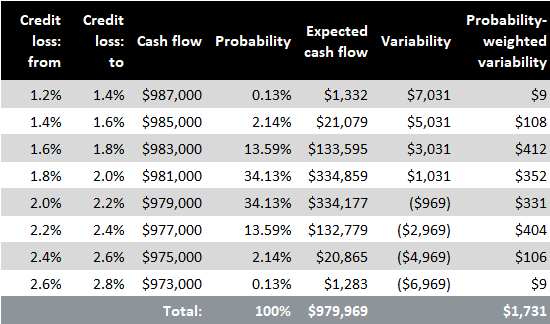

Entity A agrees to a factoring arrangement, selling its portfolio of trade receivables to the Factor. The face value and carrying amount of these receivables stand at $1 million, with the selling price at $0.9 million. After the transaction, Entity A absorbs the first 1.8% of credit losses across the portfolio, with the Factor covering the remainder. Historically, the average credit loss for similar receivables is 2%, with a standard deviation of 0.2%.

Initially, Entity A determines it has transferred its rights to receive cash flows as per IFRS 9.3.2.4(a). Subsequently, it evaluates whether it has transferred substantially all risks and rewards under IFRS 9.3.2.6(a). In this assessment, Entity A computes expected variability before and after the transfer. This is done by simulating different credit loss scenarios, assigning probabilities based on prior events, current conditions and economic forecasts. For simplicity, we’re excluding discounting in this example. All the computations from this example can be downloaded in an Excel file.

Variability before the transfer:

Too many IFRS updates? I know the feeling! That's why I created Reporting Period. It's a concise monthly summary of IFRS developments and Big 4 insights for accounting professionals. It's completely free, with zero spam, and you can unsubscribe anytime with one click. Interested? Leave your email below:

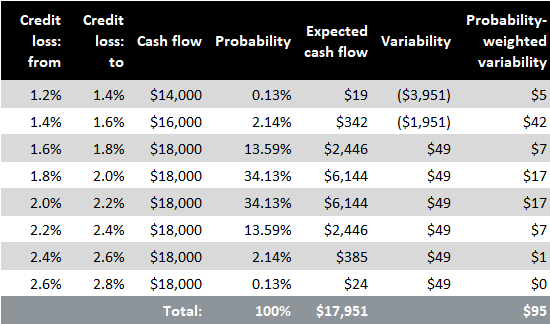

Variability after the transfer (credit loss absorbed up to 1.8%):

From the data, out of an original variability of $1,731, Entity A has transferred $1,636 (95%) and retained $95 (5%). Thus, Entity A determines that it has transferred substantially all of its exposure to the variability in the net cash flow amounts and timings (notably, IFRS 9 doesn’t set a specific percentage threshold). Therefore, substantially all risks and rewards have been transferred, leading to the derecognition of trade receivables.

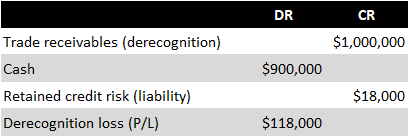

As a result, Entity A derecognises the trade receivables and recognises a one-time derecognition loss in profit or loss as per IFRS 9.3.2.12. Moreover, Entity A must account for the retained credit risk as a liability under IFRS 9.3.2.6(a). The accounting entries made by Entity A are:

IFRS 9 doesn’t specify where in the P/L the derecognition gain or loss should be presented.

See other pages relating to financial instruments:

Scope of IAS 32

Financial Instruments: Definitions

Derivatives and Embedded Derivatives: Definitions and Characteristics

Classification of Financial Assets and Financial Liabilities

Measurement of Financial Instruments

Amortised Cost and Effective Interest Rate

Impairment of Financial Assets

Derecognition of Financial Assets

Derecognition of Financial Liabilities

Factoring

Interest-Free Loans or Loans at Below-Market Interest Rate

Offsetting of Financial Instruments

Hedge Accounting

Financial Liabilities vs Equity

IFRS 7 Financial Instruments: Disclosures