Derecognition is the process of removing a previously recognised financial liability from an entity’s statement of financial position. This occurs when the obligation is discharged, cancelled, or expires. Moreover, a modification of a liability’s terms may yield a similar result.

Let’s dive in.

Derecognition resulting from modifications and restructurings

An exchange between a current borrower and lender involving debt instruments with substantially different terms should be treated as an extinguishment of the original financial liability and the recognition of a new financial liability. Similarly, a substantial modification of the terms of an existing financial liability, or part of it, should be treated as an extinguishment of the original financial liability and the recognition of a new financial liability (IFRS 9.3.3.2).

Any difference between the carrying amount of a financial liability (or part of a financial liability) derecognised and the consideration paid, or the new liability undertaken, should be recognised in P/L (IFRS 9.3.3.3).

Understanding substantially different terms

The terms of a financial liability are considered substantially different if the discounted present value of the cash flows under the new terms (discounted using the original effective interest rate) is at least 10% different from the discounted present value of the remaining cash flows of the original financial liability. This assessment includes any fees paid and received as part of the modification, but only those exchanged between the borrower and the lender (IFRS 9.B3.3.6).

--Too many IFRS updates? I know the feeling! That's why I created Reporting Period. It's a concise monthly summary of IFRS developments and Big 4 insights for accounting professionals. It's completely free, with zero spam, and you can unsubscribe anytime with one click. Interested? Leave your email below:

Example: Modification of a financial liability that does not result in a derecognition

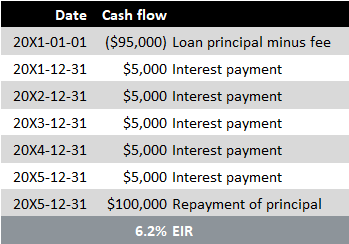

Suppose Entity A secures a bank loan on 1 January 20X1. The loan is for $100,000, and bank fees paid amount to $5,000. An annual interest of 5% is due every 31 December, and the principal should be paid back on 31 December 20X5. However, on 1 January 20X4, Entity A faces liquidity issues and requests the bank to restructure the loan. The bank consents to amend the loan terms, allowing Entity A to repay the loan on 31 December 20X7. The interest is increased to 6%, and Entity A also pays a one-time modification fee of $3,000. The following calculations and accounting schedules are available for download in an Excel file.

Initially, Entity A calculates the effective interest rate of the loan:

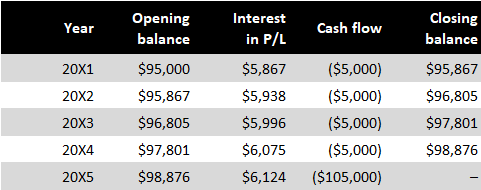

Here is the loan’s accounting schedule prior to the modification:

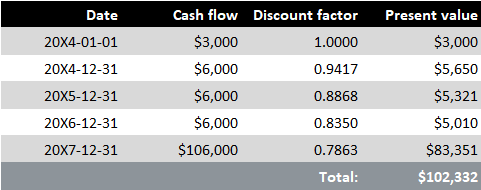

As seen in the table above, the amortised cost of the loan on the modification date (1 January 20X4) is $97,801. Entity A compares this amount to the present value of cash flows under the new terms, which includes the $3,000 of fees paid and is discounted using the original effective interest rate of 6.2%:

Since the present value after modification ($102,332) is 105% of the present value before modification ($97,801), Entity A concludes that the loan terms before and after modification are not substantially different. Thus, the liability is not derecognised. The additional fee of $3,000 is not recognised as a one-time expense but is instead amortised (IFRS 9.B3.3.6A). However, there is a one-time expense of $1,530 recognised due to the increased present value of the liability after modification. This is calculated by comparing the present value of the liability before modification ($97,801) to the present value after modification excluding the additional fee ($99,332).

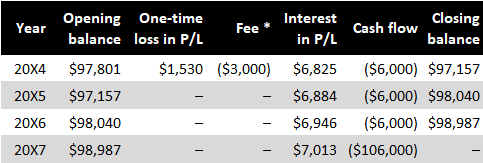

The accounting schedule for the loan post-modification is as follows:

* Reduction in the carrying amount of the liability.

Costs and fees

In the event of an extinguishment through an exchange of debt instruments or modification of terms, any ensuing costs or fees are recognised as part of the gain or loss on the extinguishment. On the other hand, if the exchange or modification isn’t an extinguishment, these costs or fees adjust the liability’s carrying amount and are amortised over the modified liability’s remaining term (IFRS 9.B3.3.6A). Such amortisation can be achieved by increasing the loan’s effective interest rate, as illustrated in the example above. While IFRS 9 is silent on what types of fees can modify the liability’s carrying amount, it’s commonly accepted that only fees payable to the lender qualify. Other fees, such as legal expenses, should be recognised immediately in profit or loss.

Modification gains and losses

When a financial liability measured at amortised cost undergoes a modification that does not lead to derecognition, the entity recalculates the financial liability’s amortised cost as the present value of the future contractual cash flows, discounted at the original effective interest rate. This recalculation triggers a one-time gain or loss recognition in profit or loss (IFRS 9.B5.4.6, BC4.252-3).

Extinguishing a financial liability

Derecognition resulting from extinguishment of a financial liability

An entity derecognises a financial liability, or a portion of it, when the liability is extinguished. This occurs when the obligation stipulated in the contract is discharged, cancelled or expires (IFRS 9.3.3.1). There are two main circumstances when a financial liability, or a part of it, is considered extinguished under IFRS 9.B3.3.1:

- The debtor discharges the liability by settling the debt with the creditor. This settlement can be made using cash, other financial assets, goods, or services.

- The debtor is legally released from the primary responsibility for the liability, either through a legal procedure or by the creditor’s action.

Gains and losses on extinguished or transferred liability

The difference between the carrying amount of a transferred or extinguished financial liability and the paid consideration, inclusive of any non-cash assets transferred or liabilities assumed, is recognised in profit or loss (IFRS 9.3.3.3).

Legal release

IFRS 9 adopts a stringent legalistic stance with regard to the legal release by a creditor. According to IFRS 9.B3.3.4, a debtor’s obligation is not derecognised simply by assigning the responsibility to a third party and informing the creditor about the change. The debtor must be legally released from the liability for the debt to be derecognised. Interestingly, even if the debtor issues a guarantee to the creditor, this doesn’t prevent the derecognition of the liability (IFRS 9.B3.3.1(b); B3.3.7).

Repurchasing a debt instrument

When an issuer of a debt instrument reacquires that instrument, the associated debt is considered extinguished. This holds true even if the issuer is a market maker of that instrument or plans to resell it in the near future (IFRS 9.B3.3.2).

Supplier finance arrangements

Supplier finance arrangements, also referred to as supply chain finance, payables finance or reverse factoring arrangements, have gained popularity, though their terms and structures can vary greatly. The derecognition criteria of IFRS 9 are notably relevant here, with the critical question being whether the original payables should be derecognised. Buyers typically prefer to maintain the original trade payable on their balance sheet, as it keeps their financial debt low.

The question that arises is whether the original obligation to the supplier has been extinguished. This would be the case if the financial intermediary settles the trade payable on the buyer’s behalf and legally releases the buyer from their obligation to the supplier. In such instances, the original trade payable is derecognised and a new liability recognised. Such a liability is fundamentally a financial liability (debt), yet it is not uncommon for entities to present them as trade payables, even though they represent liabilities to a financial institution.

In contrast, if the financial intermediary purchases the supplier’s receivable cash flow rights, without legally freeing the buyer from their obligation to pay the supplier, the trade payable is not derecognised unless there’s a significant modification of terms (the 10% threshold discussed above).

The IFRS Interpretations Committee issued an agenda decision on supplier finance arrangements, and the IASB introduced additional disclosure requirements by amending IAS 7 and IFRS 7. Further details can be found in PwC’s technical summary and an article by IASB Member Zach Gast.

More about financial instruments

See other pages relating to financial instruments:

Scope of IAS 32

Financial Instruments: Definitions

Derivatives and Embedded Derivatives: Definitions and Characteristics

Classification of Financial Assets and Financial Liabilities

Measurement of Financial Instruments

Amortised Cost and Effective Interest Rate

Impairment of Financial Assets

Derecognition of Financial Assets

Derecognition of Financial Liabilities

Factoring

Interest-Free Loans or Loans at Below-Market Interest Rate

Offsetting of Financial Instruments

Hedge Accounting

Financial Liabilities vs Equity

IFRS 7 Financial Instruments: Disclosures