IFRS 9 sets the guiding principles for financial reporting of financial assets and financial liabilities. All financial instruments and entities are in the scope of IFRS 9, with specific exceptions noted in paragraph IFRS 9.2.1. Generally, an entity recognises a financial asset or liability in its financial statements when it becomes party to the contractual provisions of the instrument (IFRS 9.3.1.1).

Let’s dive in.

Fees charged to customers by lenders

Entities engaged in the business of lending often generate revenue through various charges and fees. Examples of such fees include drawdown fees, establishment fees, and direct debit fees. A common question arises as to whether these fees fall within the scope of IFRS 9 or IFRS 15. This question also extends to fees paid by borrowers, particularly in determining which fees should be included in the calculation of the effective interest rate and which should be recognised as expenses. This publication by BDO offers valuable guidance on addressing these issues.

Financial guarantees vs other guarantees

IFRS 9 defines a financial guarantee as ‘a contract that requires the issuer to make specified payments to reimburse the holder for a loss it incurs because a specified debtor fails to make payment when due …’. Such financial guarantees fall within the scope of IFRS 9 and are accounted for as described here. It’s essential to note that not all contracts legally labelled as ‘guarantees’ qualify as financial guarantees under IFRS 9. The above definition is relatively narrow and only covers payments made when a debtor defaults on their payment. For a more comprehensive discussion, refer to IAS 32.AG8.

There are other types of ‘guarantees’, which despite being contractual financial instruments, do not fall under the category of financial guarantees. Depending on their nature, these can be treated as loan commitments or derivatives and accounted for under IFRS 9, or as insurance contracts under IFRS 17 (see below). For instance, PWC believes that performance guarantees not satisfying the definition of an insurance contract should be accounted for as loan commitments (see this discussion on our forums):

IFRS 17 defines an insurance contract as ‘a contract under which the issuer accepts significant insurance risk from the policyholder by agreeing to compensate the policyholder if a specified uncertain future event adversely affects the policyholder’. Insurance risk refers to any risk that is not financial risk (see IFRS 17 Appendix A). For further insights on this topic, refer to paragraphs IFRS 17.B7-B16 and this Deloitte’s publication on the applicability of IFRS 17 to non-insurers.

Note that it is incorrect to account for contractual guarantees under IAS 37 as this standard does not cover financial instruments.

--Too many IFRS updates? I know the feeling! That's why I created Reporting Period. It's a concise monthly summary of IFRS developments and Big 4 insights for accounting professionals. It's completely free, with zero spam, and you can unsubscribe anytime with one click. Interested? Leave your email below:

Receivables and payables

Entities recognise unconditional receivables and payables as assets or liabilities when the entity (IFRS 9.B3.1.2(a)):

- Becomes a party to the contract, and

- Has a legal right to receive cash or a legal obligation to pay cash.

Firm commitments (executory contracts)

Firm commitments to purchase or sell goods or services often result in potential assets and liabilities. However, these are generally not recognised until one party has fulfilled their part of the agreement. Such commitments are often referred to as ‘executory contracts’. For instance, a firm order does not lead to the recognition of an asset or a liability at the time of commitment. Instead, recognition is delayed until the ordered goods or services have been delivered or provided (IFRS 9.B3.1.2(b)).

If a firm commitment qualifies as a derivative instrument under the scope of IFRS 9, separate provisions apply (IFRS 9.B3.1.2(b)-(d)).

Regular way purchase or sale of financial assets (trade date and settlement date)

A ‘regular way purchase or sale’ refers to the purchase or sale of a financial asset where the terms of the contract necessitate delivery of the asset within the time frame typically established by regulations or convention in the relevant marketplace (IFRS 9 Appendix A). This method is commonplace in major stock exchanges, where transactions are settled a few days after their initiation. However, the policy choice discussed here also applies to privately issued financial instruments (IFRS 9.IG.B.28).

IFRS 9.3.1.2 offers a policy choice for such transactions: they can be recognised and derecognised using either trade date accounting or settlement date accounting.

The trade date is when an entity commits to buying or selling an asset. Trade date accounting involves the recognition of an asset to be received, and the liability to pay for it, on the trade date. It also includes the derecognition of an asset that is sold, the recognition of any gain or loss on disposal, and the recognition of a receivable from the buyer for payment on the trade date. Generally, interest doesn’t start accruing on the asset and corresponding liability until the settlement date when the title transfers (IFRS 9.B3.1.5).

The settlement date is the date when an asset is delivered. Settlement date accounting refers to the recognition of an asset on the day it is received by the entity, and the derecognition of an asset and recognition of any gain or loss on disposal on the day it is delivered by the selling entity. If settlement date accounting is used, any change in the fair value of the asset to be received between the trade date and the settlement date is accounted for in the same way as the acquired asset. Specifically, for assets measured at amortised cost, changes in fair value during this interval are not recognised. Conversely, for assets classified at FVTPL, these fair value changes are indeed recognised in P/L. (IFRS 9.B3.1.6).

Paragraphs IFRS 9.IG.D.2.1-3 provide examples illustrating the application of trade date and settlement date accounting. Both methods yield the same impact on P/L or OCI, with the only difference being the timing of recognition of the underlying financial asset.

The same method should be consistently applied for all purchases and sales of financial assets that are classified similarly under IFRS 9 (IFRS 9.B3.1.3). Regardless of the chosen approach, the trade date should be considered the date of initial recognition for applying the impairment requirements (IFRS 9.5.7.4).

Loan commitments

Loan commitments are firm commitments to provide credit under pre-specified terms and conditions. These are typically not recognised as they are outside the scope of IFRS 9, with the exception of certain loan commitments as specified in paragraph IFRS 9.2.3. See this forums topic and paragraphs IFRS 9.BCZ2.2-8 for a more comprehensive discussion.

However, the issuer must apply the impairment requirements of IFRS 9 to loan commitments (IFRS 9.2.1(g)).

Initial measurement

Generally, financial assets and liabilities are initially recognised at fair value, with an adjustment for directly attributable transaction costs. However, for items classified at fair value through profit or loss (FVTPL), transaction costs are expensed immediately (IFRS 9.5.1.1). The fair value of a financial instrument at initial recognition is typically, though not always, the transaction price (IFRS 9.B5.1.2A). IFRS 13 details conditions that might suggest a divergence between the fair value and the transaction price.

Day 1 gains/losses

When there is a difference between the transaction price and the fair value at initial recognition, IFRS 9 restricts immediate P/L recognition of these so-called ‘day 1 gains/losses’ to financial instruments with a quoted market price or a fair value derived from a valuation technique that uses solely data from observable markets (Level 1 input as per IFRS 13 terminology). For other instruments, the P/L recognition of the difference between the fair value and transaction price is deferred as an adjustment to the initial carrying amount of the financial asset or financial liability (IFRS 9.B5.1.2A(b)).

After initial recognition, the deferred difference is recognised as a gain or loss only to the extent it arises from changes in a factor (including time) that market participants would consider when pricing the asset or liability (IFRS 9.B5.1.2A).

It is not explicitly stated how the deferred difference should be recognised as a gain or loss. The Basis for Conclusions to IAS 39 suggested that straight-line amortisation may be suitable in some cases, but not all (IAS 39.BC222(v)(ii)). IFRS 9 does not elaborate on this, therefore, straight-line amortisation can be applied whenever reasonable.

Below-market interest rate loans

Please refer to a separate page for detailed guidance on interest-free loans or loans at below-market interest rate.

Trade receivables

As an exception to the general rule, trade receivables are initially recognised in line with IFRS 15 provisions, i.e., at their transaction price, potentially considering a significant financing component (IFRS 9.5.1.3).

Transaction costs

As previously stated, for financial assets not classified as fair value through profit or loss (FVTPL), transaction costs are added to the fair value at initial recognition. For financial liabilities, transaction costs are deducted from the fair value at initial recognition (IFRS 9.5.1.1).

For debt investments measured at amortised cost, transaction costs are, in effect, amortised through P/L over the life of the instrument. For equity investments measured at fair value through OCI, transaction costs are recognised in other comprehensive income as part of a change in fair value at the next remeasurement (IFRS 9.IG.E.1.1).

Transaction costs are defined as incremental costs directly attributable to the acquisition, issue or disposal of a financial asset or liability. An incremental cost is one that wouldn’t have been incurred if the financial instrument had not been acquired, issued or disposed of (IFRS 9 Appendix A). Transaction costs include fees and commissions paid to agents (including employees acting as selling agents), advisers, brokers, dealers, regulatory agencies and security exchanges, and any applicable transfer taxes and duties. However, transaction costs exclude debt premiums or discounts, financing costs or internal administrative or holding costs (IFRS 9.B5.4.8).

The determination of which costs qualify as incremental and directly attributable can involve significant judgement, particularly when such costs are incurred before the recognition of the financial instrument. For instance, a lender might incur professional fees to value a property intended to serve as collateral for a loan before providing a quote to the customer.

They are essentially two views on how to understand the term ‘incremental’ in this context:

- One view is that costs are incremental only if they’re directly triggered by executing the contract (that is, they wouldn’t have been incurred otherwise). This follows IFRS 9 definition of an incremental cost as one that “would not have been incurred if the entity had not acquired, issued or disposed of the financial instrument.”

- The alternative view is that preparatory costs should also qualify, provided the contract is likely to be executed.

This matter is currently on the agenda of the IFRS Interpretations Committee. For more details, see:

- The Committee’s tentative agenda decision.

- Staff paper prepared for the meeting.

It’s also worth noting that fees exchanged between parties to the contract (for example, between a lender and a borrower) that are an integral part of the effective interest rate are not considered transaction costs, and they are amortised as discussed here.

Cash collateral

Cash collateral is recognised by the receiving entity as cash along with a corresponding liability. The transferor, on the other hand, derecognises the cash and recognises a receivable (IFRS 9.D.1.1). Often, cash collaterals are non-interest-bearing, hence their fair value may be lower than the transaction price. This leads to the question of what should be done with the difference. The issue is similar to the one encountered with below-market interest rate loans. Specifically, under paragraph IFRS 9.B5.1.1, entities must establish what they have paid for, besides the non-interest-bearing financial instrument. Let’s look at the following example.

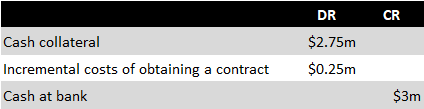

Example: Cash collateral paid by a contractor

On 1 January 20X1, Contractor X provides a security deposit of $3m to Client Y to secure a contract. This deposit will be repaid once the contract has concluded (after three years) but without any interest. The current market yield for corporate bonds issued by businesses with a similar credit standing to Client Y stands at 3%.

Contractor X recognises the deposit at $2.75m, which represents the present value of a $3m cash flow after three years (i.e. $3m/(1.03)^3). The difference between the amount paid ($3m) and the deposit recognised ($2.75m) is recognised as the incremental cost of obtaining a contract. The accounting entries at the time of initial recognition are as follows:

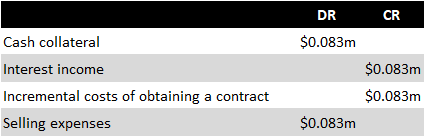

Each year, the incremental cost of obtaining a contract is amortised to P/L and interest is accrued on the cash collateral. For example, the entries after year one would be as follows:

After three years, the capitalised incremental costs of obtaining the contract will have been entirely amortised to P/L and the interest on the cash collateral will have been recognised as interest income.

More about financial instruments

See other pages relating to financial instruments:

Scope of IAS 32

Financial Instruments: Definitions

Derivatives and Embedded Derivatives: Definitions and Characteristics

Classification of Financial Assets and Financial Liabilities

Measurement of Financial Instruments

Amortised Cost and Effective Interest Rate

Impairment of Financial Assets

Derecognition of Financial Assets

Derecognition of Financial Liabilities

Factoring

Interest-Free Loans or Loans at Below-Market Interest Rate

Offsetting of Financial Instruments

Hedge Accounting

Financial Liabilities vs Equity

IFRS 7 Financial Instruments: Disclosures